Back

BackChapter 1: The Financial Statements – Foundations of Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Types of Accounting

Financial vs. Managerial Accounting

Accounting is divided into two primary branches, each serving different users and purposes within and outside an organization.

Financial Accounting: Prepares information for external users such as investors, creditors, and regulators.

Managerial Accounting: Prepares information for internal users such as managers and employees for decision-making within the organization.

Financial Accounting Standards:

In the USA, standards are set by the Financial Accounting Standards Board (FASB) and are known as Generally Accepted Accounting Principles (GAAP).

Internationally, standards are set by the International Accounting Standards Board (IASB) and are known as International Financial Reporting Standards (IFRS).

Managerial Accounting is not governed by external standard-setting bodies but may follow internal guidelines.

Business Organization

Types of Business Entities

Businesses can be organized in several forms, each with unique characteristics regarding ownership, liability, and structure.

Sole Proprietorship: Owned by one individual. The owner has unlimited liability for business debts, and income is reported on the owner's personal tax return.

Partnership: Owned by two or more individuals. Partners generally have unlimited liability unless structured as a limited partnership.

Corporation: A separate legal entity from its owners (stockholders). Owners have limited liability, meaning they are not personally responsible for business debts. Corporations have unlimited life and easy transferability of ownership.

Hybrid Organizations (e.g., LLC, LLP): Combine features of partnerships and corporations, often providing limited liability to owners with flexible management structures.

Additional info: The table above compares ownership and liability characteristics across different business forms.

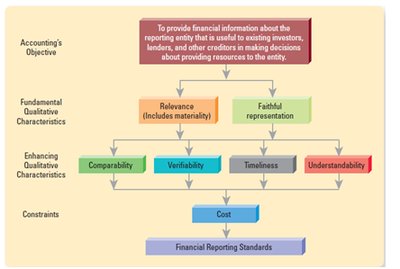

Qualitative Characteristics of Useful Information

Primary and Enhancing Qualitative Characteristics

For accounting information to be useful, it must possess certain qualitative characteristics as defined by the conceptual framework.

Relevance: Information must be capable of making a difference in users' decisions. It includes:

Predictive Value: Helps users predict future outcomes.

Confirmatory Value: Provides feedback about previous evaluations.

Faithful Representation: Information must be complete, neutral, and free from material error.

Completeness: All necessary information is provided.

Neutrality: Information is unbiased.

Freedom from Error: No material errors are present.

Enhancing Qualitative Characteristics:

Comparability: Enables users to identify similarities and differences across companies and periods.

Verifiability: Different knowledgeable and independent observers can reach consensus that information is faithfully represented.

Timeliness: Information is available to decision-makers in time to influence their decisions.

Understandability: Information is presented clearly and concisely.

Additional info: The diagram above illustrates the hierarchy and interaction of qualitative characteristics in financial reporting.

Underlying Assumptions and Principles

Basic Assumptions

Monetary Unit Assumption: Accounting records are maintained in a stable currency.

Economic Entity Assumption: The business is separate from its owners and other entities.

Periodicity Assumption: The life of a business can be divided into time periods for reporting purposes.

Going Concern Assumption: The business will continue operating indefinitely unless there is evidence to the contrary.

Key Principles

Historical Cost Principle: Assets are recorded at their original cost.

Fair Value Principle: Some assets and liabilities are reported at their current market value.

Full Disclosure Principle: All information that affects users' understanding must be disclosed in the financial statements.

Cost Constraint: The benefit of information should outweigh the cost of providing it.

The Financial Statements

Overview of the Four Main Financial Statements

Financial statements provide a structured representation of the financial position and performance of a business.

Balance Sheet: Shows assets, liabilities, and equity at a specific point in time.

Income Statement: Reports revenues and expenses over a period, resulting in net income or loss.

Statement of Cash Flows: Details cash inflows and outflows over a period.

Statement of Stockholders' Equity: Explains changes in equity accounts over a period. Small companies may use a Statement of Retained Earnings instead.

Classification of Accounts:

Assets: Resources owned by the company (e.g., cash, inventory, land).

Liabilities: Obligations owed to outsiders (e.g., accounts payable, bonds payable).

Equity: Owners' claims on the business (e.g., common stock, retained earnings).

Revenue: Inflows from delivering goods or services.

Expenses: Outflows from receiving goods or services.

Fundamental Accounting Equation

The Core Equation

The foundation of financial accounting is the accounting equation, which must always remain in balance:

Assets: Anything tangible or intangible owned by the company.

Current Assets: Expected to be converted to cash within one year.

Long-term Assets: Used for more than one year (e.g., land, machinery).

Liabilities: Amounts owed to others.

Current Liabilities: Due within one year.

Long-term Liabilities: Due after one year.

Equity: Consists of paid-in capital and retained earnings.

Paid-in Capital: Amount invested by stockholders.

Retained Earnings: Cumulative net income not distributed as dividends.

Dividends: Distributions to shareholders from retained earnings (not an expense).

Income/Loss: Net result of revenues minus expenses.

Example: If a company has assets of $50,000 and equity of $20,000, liabilities are $30,000 ($50,000 - $20,000).

Practice Problems:

If liabilities are $25,000 and assets are $35,000, equity is $10,000 ($35,000 - $25,000).

If liabilities are $65,000 and equity is $25,000, assets are $90,000 ($65,000 + $25,000).