Back

BackChapter 1: The Financial Statements – Foundations of Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 1: The Financial Statements

Introduction to Accounting

Accounting is an information system that measures, processes, and communicates financial data about business activities. It is often referred to as the "language of business" because it provides essential information for decision-making by various stakeholders.

Individuals use accounting for personal finance management.

Investors & Creditors use accounting to assess returns and repayment ability.

Regulatory Bodies (e.g., IRS, SEC) rely on accounting for oversight.

Nonprofits use accounting for resource allocation and compliance.

Types of Accounting

Financial Accounting: Provides information to external users (investors, creditors, government agencies, public).

Managerial Accounting: Provides information to internal users (managers).

The Accounting Cycle

The accounting cycle is the process by which a company prepares its financial statements:

People make decisions

Business transactions occur

Companies report their results

The Accounting Equation

The foundation of all accounting is the accounting equation:

Can be rearranged as: or

Definitions of Key Terms

Assets: Economic resources expected to provide future benefits (e.g., cash, accounts receivable, inventory, equipment).

Liabilities: Debts owed to outsiders (e.g., accounts payable, notes payable).

Equity: Owners' claims on the business assets (includes paid-in capital and retained earnings).

Revenue: Inflows from delivering goods/services; increases equity.

Expenses: Outflows due to operations; decreases equity.

Dividends: Distributions to stockholders; decreases equity.

Financial Statements Overview

There are four primary financial statements, each answering a key question about the business:

Income Statement: Reports revenues, expenses, and net income/loss for a period.

Statement of Retained Earnings: Explains changes in retained earnings.

Balance Sheet: Shows assets, liabilities, and equity at a point in time.

Statement of Cash Flows: Reports cash inflows and outflows from operating, investing, and financing activities.

Business Organization Forms

Businesses can be organized in several ways, each with different implications for liability and taxation:

Proprietorship: One owner, personally liable.

Partnership: Two or more owners, personally liable. Income flows through to partners.

Limited Liability Partnership (LLP): Limits liability for partners except the general partner.

Limited Liability Company (LLC): Two or more members, not personally liable; income flows through to members.

Corporation: Owned by stockholders, not personally liable; subject to double taxation.

Accounting Standards and Principles

GAAP (Generally Accepted Accounting Principles): U.S. standards for financial reporting.

FASB (Financial Accounting Standards Board): Sets U.S. GAAP.

IASB (International Accounting Standards Board): Sets IFRS (International Financial Reporting Standards).

Qualitative Characteristics of Accounting Information

Relevance: Useful for decision-making.

Faithful Representation: Complete, neutral, free from error.

Comparability: Consistent across companies and periods.

Verifiability: Can be checked for accuracy.

Timeliness: Available in time for decisions.

Understandability: Clear to informed users.

Key Accounting Assumptions and Principles

Entity Assumption: Each business is a separate economic unit.

Continuity (Going-Concern) Assumption: The business will continue operating.

Historical Cost Principle: Assets recorded at their original cost.

Fair Value: Current value for settling liabilities.

Stable-Monetary-Unit Assumption: Ignores inflation; assumes stable currency value.

Transactions Affecting Owner’s Equity

Investments: Owner contributes resources; increases assets and equity.

Withdrawals: Owner takes out resources; decreases assets and equity.

Revenue: Increases assets and equity.

Expenses: Decreases assets and equity.

Financing, Investing, and Operating Activities

Business activities are classified as financing, investing, or operating, each impacting the accounting equation differently.

Financing: Borrowing or owner investments (e.g., loans, issuing stock).

Investing: Acquiring long-term assets (e.g., equipment, buildings).

Operating: Day-to-day activities (e.g., sales, paying expenses).

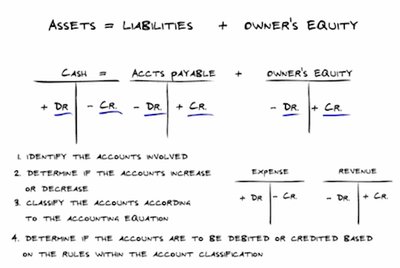

Debits and Credits in the Accounting Equation

Debits and credits are used to record increases and decreases in accounts according to the accounting equation:

Assets: Increase with debits, decrease with credits.

Liabilities: Increase with credits, decrease with debits.

Owner’s Equity: Increase with credits, decrease with debits.

Expenses: Increase with debits.

Revenue: Increase with credits.

Identify the accounts involved.

Determine if the accounts increase or decrease.

Classify the accounts according to the accounting equation.

Determine if the accounts are debited or credited based on classification rules.

Examples of Journal Entries and T-Accounts

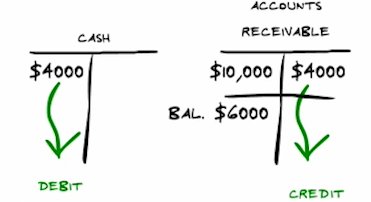

Partial Payment on Accounts Receivable

When a customer makes a partial payment on an account, both cash and accounts receivable are affected:

Cash is debited (increased) by the amount received.

Accounts Receivable is credited (decreased) by the same amount.

The remaining balance in Accounts Receivable reflects what is still owed.

Paying Expenses

When a business pays for expenses such as rent or salaries, cash decreases and the respective expense accounts increase:

Cash is credited (decreased) by the total amount paid.

Rent Expense and Salary Expense are debited (increased) by their respective amounts.

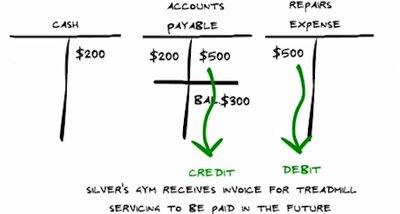

Receiving an Invoice for Future Payment

When a business receives an invoice for services to be paid in the future, an expense and a liability are recorded:

Repairs Expense is debited (increased).

Accounts Payable is credited (increased), representing the obligation to pay in the future.

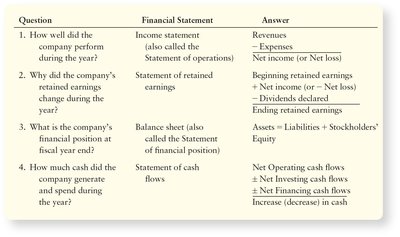

Summary Table: Financial Statements and Their Purposes

Question | Financial Statement | Answer |

|---|---|---|

1. How well did the company perform during the year? | Income statement (Statement of operations) | Revenues – Expenses = Net income (or Net loss) |

2. Why did the company’s retained earnings change during the year? | Statement of retained earnings | Beginning retained earnings ± Net income (or Net loss) – Dividends declared = Ending retained earnings |

3. What is the company’s financial position at fiscal year end? | Balance sheet (Statement of financial position) | Assets = Liabilities + Stockholders’ Equity |

4. How much cash did the company generate and spend during the year? | Statement of cash flows | Net Operating cash flows ± Net Investing cash flows ± Net Financing cash flows = Increase (decrease) in cash |

Additional info: This summary provides a foundational overview of financial accounting, focusing on the structure, principles, and practical application of the accounting equation and financial statements. The included images reinforce key concepts such as T-accounts, debits and credits, and the flow of transactions through the accounting system.