Back

BackChapter 1: The Financial Statements – Key Concepts and Foundations

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Types of Accounting

Financial vs. Managerial Accounting

Accounting is divided into two primary branches: Financial Accounting and Managerial Accounting. Each serves distinct purposes and audiences.

Financial Accounting: Provides information for external users such as investors, creditors, and regulatory agencies. It follows strict standards to ensure comparability and reliability.

Managerial Accounting: Generates information for internal users, including managers and employees, to aid in decision-making and operational control.

Standards: In the USA, financial accounting follows Generally Accepted Accounting Principles (GAAP), set by the Financial Accounting Standards Board (FASB). Internationally, International Financial Reporting Standards (IFRS) are used, set by the International Accounting Standards Board (IASB).

Business Organization Types

Forms of Business Entities

Businesses can be organized in several ways, each with unique characteristics regarding ownership, liability, and structure.

Sole Proprietorship: Owned by one individual. The owner's income is fully attributed to them, and they have unlimited liability for business debts.

Partnership: Similar to a sole proprietorship but with multiple owners. Partners generally have unlimited liability.

Corporation: A separate legal entity from its owners. Features include unlimited life, easy transferability of ownership, and limited liability for owners.

Hybrid Organizations (e.g., LLC, LLP): Offer special rules for owner liability. For example, in an LLP, partners are not liable for another partner's malpractice.

Table Purpose: The table compares ownership and liability characteristics across sole proprietorships, partnerships, LLCs, and corporations.

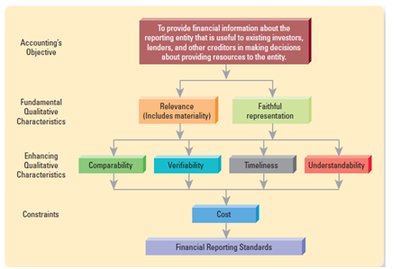

Useful Information in Accounting

Qualitative Characteristics of Financial Information

For accounting information to be useful, it must possess certain qualitative characteristics, as defined by standard-setting bodies.

Relevance: Information must influence decisions, with predictive and confirmatory value.

Faithful Representation: Information must be complete, neutral, and free from material error.

Enhancing Characteristics: Comparability, verifiability, timeliness, and understandability improve the usefulness of information.

Cost Constraint: The benefit of information must outweigh the cost of obtaining it.

Image Purpose: This diagram visually organizes the hierarchy of accounting objectives, qualitative characteristics, and constraints.

Underlying Assumptions and Principles

Accounting Assumptions

Financial accounting relies on several foundational assumptions:

Monetary Unit: The currency used in accounting is stable over time.

Economic Entity: The business is separate from its owners and other entities.

Periodicity: The economic life of a business is divided into regular reporting periods.

Going Concern: The business is expected to operate indefinitely.

Accounting Principles

Historical Cost Principle: Assets are recorded at their original cost.

Fair Value Principle: Assets are reported at their current market value.

Full Disclosure Principle: All information that could affect users' decisions must be disclosed.

Cost Constraint: Information should not be too costly to obtain relative to its benefit.

The Financial Statements

Overview of Financial Statements

There are four main financial statements required by GAAP:

Balance Sheet: Shows assets, liabilities, and equity at a specific point in time. Formula:

Income Statement: Reports revenues and expenses over a period. Formula:

Statement of Cash Flows: Details changes in cash over a period.

Statement of Stockholder's Equity: Shows changes in equity over a period. Small companies may use a Statement of Retained Earnings.

Account Classifications

Accounts are classified into five broad categories:

Assets: Resources owned by the company (e.g., cash, inventory, land).

Liabilities: Obligations owed to others (e.g., accounts payable, bonds payable).

Equity: Owner's residual interest (e.g., common stock, retained earnings).

Revenue: Income from sales or services.

Expenses: Costs incurred in earning revenue.

Fundamental Accounting Equation

Definition and Application

The fundamental accounting equation is the cornerstone of financial accounting:

Equation:

Assets: Tangible or intangible items owned by the company. Current Assets: Convertible to cash within one year. Long-term Assets: Used for more than one year.

Liabilities: Money owed to others. Current Liabilities: Payable within one year. Long-term Liabilities: Payable after one year.

Equity: Includes paid-in capital and retained earnings. Paid-in Capital: Money invested by stockholders. Retained Earnings: Accumulated income not distributed as dividends.

Dividends: Payments to shareholders from retained earnings. Note: Dividends are not an expense.

Income/Loss: Net result of revenue minus expenses.

Example: Equity in Home Purchase

If a home costs $150,000 and you make a $30,000 down payment, the remainder is financed by a mortgage. Paying back $20,000 of the principal increases your equity in the home.

Practice Problems

Applying the Accounting Equation

Problem 1: A company has assets totaling $50,000 and equity of $20,000. What are their liabilities? Solution:

Problem 2: A company has liabilities of $25,000 and assets of $35,000. What is the company’s equity? Solution:

Problem 3: If a company has liabilities of $65,000 and equity of $25,000, what are the company’s assets worth? Solution:

Additional info: Academic context and examples were added to clarify and expand on brief points from the original materials.