Back

BackChapter 11: Statement of Cash Flows – Comprehensive Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Statement of Cash Flows

Introduction to the Statement of Cash Flows

The Statement of Cash Flows (SCF) is a fundamental financial statement that explains the change in a company’s cash balance over a period. It provides insight into the sources and uses of cash, helping users assess liquidity and predict future cash flows. Unlike the income statement, which is accrual-based, the SCF focuses on actual cash movements.

Liquidity: Measures how quickly assets can be converted to cash to pay obligations.

Cash Flow Statement: Explains how cash changed from one balance sheet to the next.

Importance: Cash is so vital that it has its own statement, covering the same period as the income statement but from a cash perspective.

Purpose and Users of the Statement of Cash Flows

The SCF helps answer key questions about a company’s financial health:

Is there enough cash to pay short-term debt?

How much cash is generated from operations?

Did the company finance purchases internally or rely on external financing?

Is the company changing its external financing sources?

Is the company providing a cash return to shareholders?

Internal users (management, board of directors) and external users (equity holders, creditors) rely on the SCF for decision-making.

Structure of the Statement of Cash Flows

Three Major Sections

The SCF is divided into three main sections, each reflecting a different type of activity:

Operating Activities: Cash flows from day-to-day business operations.

Investing Activities: Cash flows from buying and selling long-term assets and investments.

Financing Activities: Cash flows from transactions with equity holders and creditors.

Additionally, the effect of currency exchange rate changes may be reported, but is not a major category.

Cash Flow Equation

The change in cash is calculated as:

Change in Cash = Operating Cash Flow + Investing Cash Flow + Financing Cash Flow + Effect of Exchange Rate Changes

Ending Cash Balance = Beginning Cash Balance + Change in Cash

For class purposes, assume no currency exchange rate impact unless stated otherwise.

Operating, Investing, and Financing Activities

Operating Activities

Operating activities are the most desirable and sustainable source of cash. They include cash flows related to generating revenues and incurring expenses.

Examples: Cash received from customers, cash paid to suppliers, wages, rent, and other day-to-day expenses.

Operating cash flows are mostly related to income statement activities.

Investing Activities

Investing activities reflect how a company spends cash on investments expected to generate returns.

Examples: Purchase and sale of property, plant, and equipment (PP&E), investments in securities.

Financing Activities

Financing activities involve cash transactions with equity holders and creditors.

Examples: Issuing stock, borrowing and repaying debt, paying dividends, repurchasing shares.

Methods of Preparing the Statement of Cash Flows

Direct Method

The direct method records each cash transaction in the appropriate section. It is straightforward but cumbersome for companies with many transactions.

Cash inflows from customers

Cash outflows to suppliers

Other operating inflows/outflows

Indirect Method

The indirect method starts with net income and adjusts for non-cash and non-operating items to arrive at cash flow from operations. It is required under US GAAP and explains why net income and cash flows from operations differ.

Adjusts net income for depreciation, amortization, gains/losses, and changes in operating assets and liabilities.

Comparison Table: Direct vs. Indirect Method

Aspect | Direct Method | Indirect Method |

|---|---|---|

Operating Section | Records actual cash transactions | Adjusts net income for non-cash items |

Investing & Financing Sections | Identical to indirect | Identical to direct |

US GAAP Requirement | Optional (rarely used) | Required |

Example: XYZ Company Statement of Cash Flows

XYZ Balance Sheet and Income Statement

XYZ Company’s transactions illustrate the preparation of the SCF. The balance sheet and income statement provide the necessary data for both methods.

Assets | 2020 | 2019 | Liabilities | 2020 | 2019 |

|---|---|---|---|---|---|

Cash | 1,280 | 500 | Interest Payable | 200 | 0 |

A/R | 4,500 | 0 | Bonds Payable | 2,000 | 0 |

Inventory | 800 | 1,000 | Note Payable | 0 | 0 |

PP&E, net | 0 | 0 | |||

Common Stock | 2,500 | 1,500 | Retained Earnings | 2,380 | 0 |

Treasury Stock | (500) | 0 | |||

Total Assets | 6,580 | 1,500 | Total Liab & SE | 6,580 | 1,500 |

XYZ Statement of Cash Flows – Direct Method

Cash from Operations: $(20)

Cash from Investing: $1,800

Cash from Financing: $(1,000)

Total Change in Cash: $780

XYZ Statement of Cash Flows – Indirect Method

Start with Net Income: $4,380

Add Depreciation Expense: $500

Subtract Gain on Sale of PP&E: $(800)

Subtract Increase in A/R: $(4,500)

Add Decrease in Inventory: $200

Add Increase in Interest Payable: $200

Total Cash from Operations: $(20)

Cash from Investing: $1,800

Cash from Financing: $(1,000)

Total Change in Cash: $780

Steps for Constructing the Indirect Method SCF

Step-by-Step Process

Start with Net Income

Add back non-cash expenses (depreciation, amortization, depletion)

Adjust for non-operating gains and losses

Recognize net cash inflows/outflows from changes in operating assets and liabilities

Sum to yield net cash flows from operating activities

Formula:

Practice Questions and Journal Entries

Depreciation

Journal Entry: Dr. Depreciation Expense; Cr. Accumulated Depreciation

Effect on Net Income: Decreases by depreciation amount

Effect on Cash from Operations: No effect; add back depreciation to net income

Gain/Loss on Sale of PP&E

Journal Entry: Dr. Cash; Dr. Accumulated Depreciation; Cr. PP&E Cr. Gain on Sale

Effect on Net Income: Increase by gain

Effect on Cash from Operations: Subtract gain from net income

Changes in Non-cash Assets and Liabilities

Increase in Accounts Receivable: Subtract from net income

Decrease in Inventory: Add to net income

Increase in Operating Liabilities: Add to net income

Decrease in Operating Liabilities: Subtract from net income

Free Cash Flow (FCF)

Definition and Calculation

Free Cash Flow is the cash available from operations after paying for capital investments (capex). It is a key measure of financial flexibility and is used in firm valuation models.

Formula:

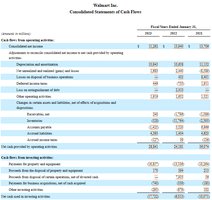

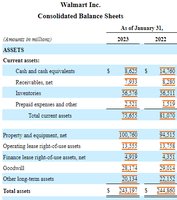

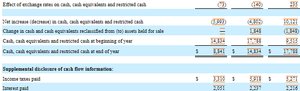

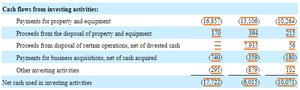

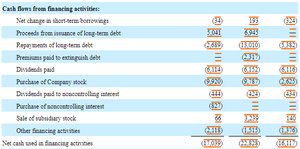

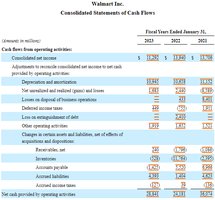

Real-World Example: Walmart Statement of Cash Flows

Walmart 2023 10-K Balance Sheet

Walmart 2023 10-K Statement of Cash Flows

Cash from Operations

Cash from Investing

Cash from Financing

Effect of Currency Exchange Rate Changes

Summary Table: Key Concepts in Statement of Cash Flows

Concept | Definition | Example |

|---|---|---|

Operating Activities | Cash flows from core business operations | Cash received from customers |

Investing Activities | Cash flows from buying/selling assets | Purchase of equipment |

Financing Activities | Cash flows from equity/debt transactions | Issuing stock, paying dividends |

Direct Method | Records actual cash transactions | Cash paid to suppliers |

Indirect Method | Adjusts net income for non-cash items | Add back depreciation |

Free Cash Flow | Cash available after capex | Net cash from ops minus capital investments |

Conclusion

The Statement of Cash Flows is essential for understanding a company’s liquidity, financial flexibility, and ability to meet obligations. Mastery of both the direct and indirect methods, as well as the classification of cash flows, is crucial for financial accounting students.