Back

BackChapter 14: The Statement of Cash Flows – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 14: The Statement of Cash Flows

Introduction

The statement of cash flows is a fundamental financial statement that provides information about a company’s cash receipts and cash payments during a specific period. It helps users understand how a business generates and uses cash, and why net income does not always equal the change in cash balance.

Purposes and Structure of the Statement of Cash Flows

Purpose of the Statement

Explains cash changes: Reports why cash increased or decreased during the period.

Predicts future cash flows: Assists in forecasting a company’s ability to generate cash in the future.

Evaluates management: Provides insight into how management uses cash.

Assesses liquidity: Helps predict the ability to pay debts and dividends.

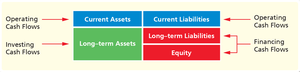

Classification of Cash Flows

Cash flows are classified into three main categories:

Operating Activities: Cash flows from the primary revenue-generating activities of the business.

Investing Activities: Cash flows from the acquisition and disposal of long-term assets and investments.

Financing Activities: Cash flows from transactions with the company’s owners and creditors.

Non-Cash Investing and Financing Activities

Transactions that do not involve cash but affect long-term assets, liabilities, or equity (e.g., acquiring equipment by issuing stock).

Reported in a separate schedule or in the notes to the financial statements.

Sections of the Statement of Cash Flows

Operating Activities

Cash Inflows: From customers, interest revenue, and dividend income.

Cash Outflows: For inventory, operating expenses, interest expense, and income tax expense.

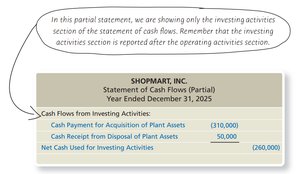

Investing Activities

Cash Inflows: From the sale of property, plant, equipment, and investments; collection of long-term notes receivable.

Cash Outflows: To purchase property, plant, equipment, and investments; loans made to borrowers.

Financing Activities

Cash Inflows: From issuance of stock, selling treasury stock, and borrowing money.

Cash Outflows: For payment of dividends, buying treasury stock, and repayment of loans.

Methods for Reporting Operating Activities

Indirect Method

Starts with accrual net income and adjusts for non-cash items and changes in current assets and liabilities.

Most commonly used method in practice.

Direct Method

Reports actual cash receipts and payments from operating activities.

Preferred by the Financial Accounting Standards Board (FASB) for clarity.

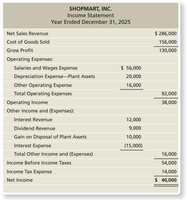

Preparing the Statement of Cash Flows (Indirect Method)

Required Information

Current year income statement

Current and prior year balance sheets

Additional transaction details

Preparation Steps

Calculate cash flows from operating activities.

Calculate cash flows from investing activities.

Calculate cash flows from financing activities.

Compute the change in cash.

Prepare a schedule for non-cash activities.

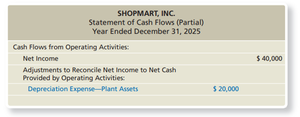

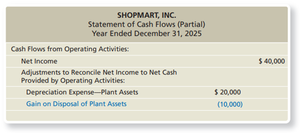

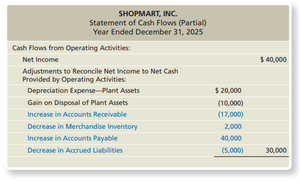

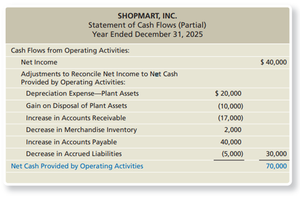

Adjustments in the Operating Activities Section

Depreciation, Depletion, and Amortization: Non-cash expenses added back to net income.

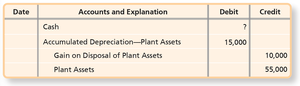

Gains and Losses on Disposal of Long-Term Assets: Subtracted (gains) or added (losses) to net income to avoid double-counting.

Changes in Current Assets and Liabilities: Adjustments reflect the cash effects of changes in accounts such as receivables, inventory, payables, and accrued liabilities.

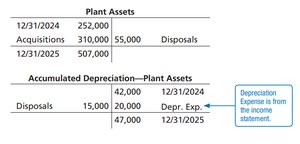

Investing Activities

Cash Flows from Investing Activities

Include cash paid for acquisitions and cash received from disposals of long-term assets.

Analysis of T-accounts helps identify cash transactions related to investments.

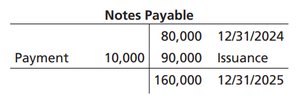

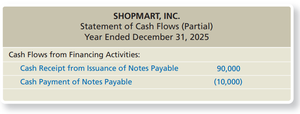

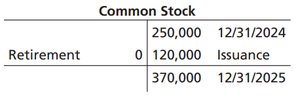

Financing Activities

Cash Flows from Financing Activities

Include cash received from issuing notes payable or stock, and cash paid for retiring debt, repurchasing stock, or paying dividends.

Non-Cash Investing and Financing Activities

Reported separately from the main statement of cash flows.

Examples: Acquiring assets by issuing stock, converting debt to equity.

Free Cash Flow

Definition and Importance

Free Cash Flow (FCF): The cash available from operating activities after paying for planned investments in long-term assets and after paying dividends.

Formula:

FCF is a key measure for evaluating a company’s financial flexibility and ability to pursue new opportunities.

Direct Method for Operating Activities (Appendix 14A)

Overview

Reports actual cash receipts and payments from operating activities.

Provides more transparent information about cash flows than the indirect method.

Key Components

Cash Collections from Customers: Calculated by adjusting net sales revenue for changes in accounts receivable.

Cash Receipts of Interest and Dividend Revenue: Reported if received in cash during the period.

Payments to Suppliers: Includes payments for inventory and operating expenses (excluding employee compensation, interest, and income taxes).

Payments to Employees: Salaries, wages, and other compensation paid in cash.

Payments for Interest and Income Taxes: Cash paid for these expenses during the period.

Summary Table: Classification of Cash Flows

Activity | Examples of Cash Inflows | Examples of Cash Outflows |

|---|---|---|

Operating | Receipts from customers, interest, dividends | Payments to suppliers, employees, interest, taxes |

Investing | Sale of property, plant, equipment, investments | Purchase of property, plant, equipment, investments |

Financing | Issuance of stock, borrowing | Dividends paid, repayment of debt, treasury stock purchases |

Additional info: Data analytics tools are increasingly used to monitor and analyze cash flows in real time, supporting better financial decision-making.