Back

BackChapter 2: Recording Business Transactions – Transaction Analysis and the Accounting Cycle

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Transaction Analysis and the Accounting Cycle

Introduction to Transaction Analysis

Transaction analysis is a foundational process in financial accounting, involving the identification, measurement, and recording of business transactions. This process ensures that all financial events are accurately reflected in the accounting records, maintaining the integrity of the financial statements.

Business Transaction: An event with a financial impact on the business, measurable in monetary terms (e.g., US dollars).

Non-transaction Event: An event that does not have a direct financial impact or cannot be measured in monetary terms (e.g., hiring a new CEO, employee satisfaction).

Double-entry Principle: Every transaction affects at least two accounts, ensuring the accounting equation remains balanced.

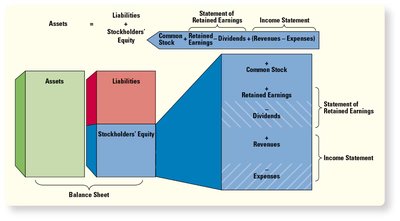

Accounting Equation: Assets = Liabilities + Equity

Types of Accounts and Their Classification

Accounts are records of all changes in a particular asset, liability, or equity item during a period. Each account must be classified as one of the ten elements of financial statements:

Assets: Cash, Accounts Receivable, Inventory, Prepaid Expenses, Property, Plant & Equipment (PP&E), Investments, Notes Receivable

Liabilities: Accounts Payable, Accrued Liabilities, Taxes Payable, Interest Payable, Rent Payable, Notes Payable, Bonds Payable

Equity: Common Stock, Retained Earnings (affected by Revenues/Gains, Expenses/Losses, Dividends Declared)

Examples of Account Usage

Cash: Records all cash received and paid.

Accounts Receivable: Records sales on account (credit sales) and collections of cash for those sales.

Inventory: Records purchases and sales of goods held for sale.

PP&E: Records purchases and disposals of long-term assets used in operations.

Accounts Payable: Records purchases made on account and payments made on those accounts.

Notes Payable: Records borrowings and repayments involving formal notes.

The Accounting Cycle: Steps and Activities

Overview of the 12-Step Accounting Cycle

The accounting cycle is a systematic process for recording and processing all financial transactions of a company. The main steps include:

Event/Transaction Identification

Journalize Events (Journal Entries)

Post to Ledger

Unadjusted Trial Balance

End of Period

Adjusting Journal Entries

Post to Ledger

Adjusted Trial Balance

Prepare Financial Statements

Closing Entries

Post to Ledger

Post-Closing Trial Balance

Analyzing Transactions with the Accounting Equation

Each transaction must be analyzed to determine its effect on the accounting equation. For example:

Issuing common stock for cash increases both assets and equity.

Purchasing land for cash increases one asset (land) and decreases another (cash).

Buying supplies on account increases assets (supplies) and liabilities (accounts payable).

Paying wages decreases assets (cash) and equity (expense).

Recording Transactions: Journal Entries and Posting

Journal Entries

Journal entries are the first formal record of a transaction. Each entry must include:

Date of the transaction

Accounts to be debited and credited

Amounts for each debit and credit

Total debits must equal total credits

Journal Entry Format:

Debit account(s) listed first with amounts in the debit column

Credit account(s) indented with amounts in the credit column

Posting to the General Ledger

After journalizing, amounts are posted to the general ledger, which groups all T-accounts and their balances. The ledger consists of:

Real (Permanent) Accounts: Balance sheet accounts that remain open at period end.

Nominal (Temporary) Accounts: Income statement accounts and dividends declared, closed at period end.

T-Accounts and the Rules of Debit and Credit

T-Accounts

A T-account is a visual tool used to represent the increases and decreases in an account. The left side is the debit side, and the right side is the credit side. The normal balance of an account determines which side increases the account.

Assets, Expenses, Dividends: Normal debit balance (increase with debits, decrease with credits)

Liabilities, Revenues, Stockholders’ Equity: Normal credit balance (increase with credits, decrease with debits)

Mnemonic: DEAD CURLS

Debits increase: Expenses, Assets, Dividends

Credits increase: Unearned Revenue, Revenue, Liabilities, Stockholders’ Equity

The Expanded Accounting Equation

The expanded accounting equation provides more detail on the components of equity:

Trial Balance Preparation

Unadjusted Trial Balance

A trial balance is a list of all open accounts in the general ledger and their balances at a specific point in time. Its main purpose is to check the equality of debits and credits. Accounts are listed in the following order:

Assets (in order of liquidity: Cash, Accounts Receivable, Inventory, Prepaids, Investments, PP&E, Intangibles)

Liabilities (current first, long-term last)

Equity (Common Stock, Retained Earnings)

Dividends Declared

Revenues/Gains

Expenses/Losses

Finding Missing Information Using T-Accounts and Trial Balance

Using T-Accounts

T-accounts can be used to reconstruct missing information, such as the amount of inventory purchased, equipment sold, new borrowings, or sales on account, by analyzing beginning and ending balances and additional transaction data.

Using the Trial Balance

The trial balance can help determine missing account balances (e.g., equipment) and total assets by ensuring that total debits equal total credits after all transactions have been posted.

Summary Table: Normal Balances and Effects of Debits/Credits

Account Type | Normal Balance | Debit Effect | Credit Effect |

|---|---|---|---|

Assets | Debit | Increase | Decrease |

Liabilities | Credit | Decrease | Increase |

Common Stock | Credit | Decrease | Increase |

Retained Earnings | Credit | Decrease | Increase |

Revenues/Gains | Credit | Decrease | Increase |

Expenses/Losses | Debit | Increase | Decrease |

Dividends Declared | Debit | Increase | Decrease |

Key Formulas

Basic Accounting Equation:

Expanded Equity:

Retained Earnings:

Net Income: