Back

BackChapter 2: Transaction Analysis – Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Transaction Analysis in Financial Accounting

Recognizing Business Transactions and Types of Accounts

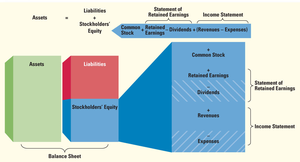

Business transactions are events that have a financial impact on a company and can be measured reliably. Each transaction involves an exchange where something is given and something is received, and both sides are recorded in the accounting system. The accounting equation forms the foundation for recording these events:

Assets: Economic resources providing future benefit (e.g., cash, accounts receivable, inventory, prepaid expenses, investments, property, plant & equipment).

Liabilities: Debts or payables (e.g., accounts payable, notes payable, accrued liabilities).

Stockholders’ Equity: Owners’ claims to assets (e.g., common stock, retained earnings, dividends, revenues, expenses).

Accounting Equation:

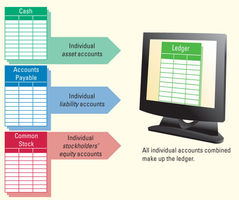

Account: A record of all changes in a particular asset, liability, or equity item during a period.

Examples of Account Types

Cash: Money, bank balances, currency, checks.

Accounts Receivable: Amounts owed by customers.

Inventory: Goods held for sale.

Accounts Payable: Amounts owed to suppliers.

Common Stock: Owner investment.

Retained Earnings: Cumulative net income minus dividends.

Revenues: Increases in equity from sales/services.

Expenses: Decreases in equity from business operations.

Analyzing the Impact of Transactions on the Accounting Equation

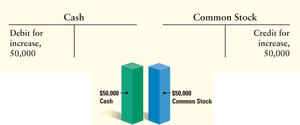

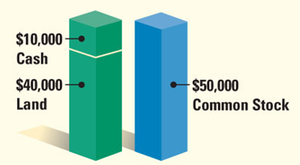

Each business transaction affects the accounting equation. For example, when owners invest cash and receive stock, both assets and equity increase. When land is purchased for cash, assets (land) increase while assets (cash) decrease.

Double-entry system: Every transaction affects at least two accounts.

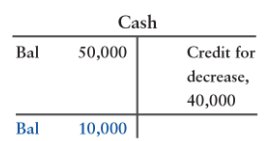

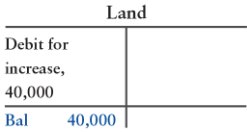

T-Account: Visual tool to record increases (debits) and decreases (credits) in accounts.

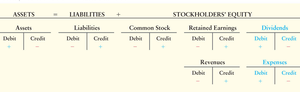

Rules of Debit and Credit:

Assets: Debit increases, Credit decreases

Liabilities: Debit decreases, Credit increases

Stockholders’ Equity: Debit decreases, Credit increases

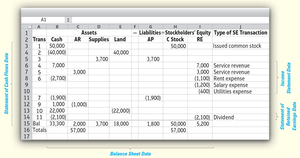

Transaction Examples

Owners invest $50,000 cash and receive common stock.

Purchase land for $40,000 cash.

Buy supplies on account ($3,700).

Earn service revenue ($7,000 cash, $3,000 on account).

Pay expenses (rent, salaries, utilities).

Pay accounts payable.

Declare and pay dividends.

Analyzing the Impact of Transactions on Accounts

Transactions are recorded using the double-entry system, affecting at least two accounts. The T-account helps visualize these changes. For example, receiving cash increases the cash account (debit), while issuing stock increases common stock (credit).

Expanded Accounting Equation

The expanded equation includes income statement accounts:

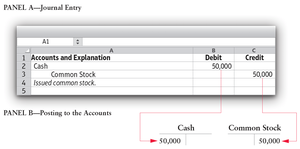

Journalizing Transactions and Posting to the Ledger

Journalizing involves recording transactions chronologically in a journal. Steps:

Specify each account affected and classify by type.

Determine if each account is increased or decreased (debit or credit).

Record in the journal.

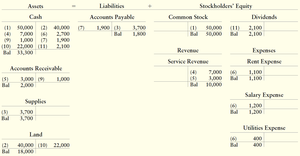

Ledger Accounts After Posting

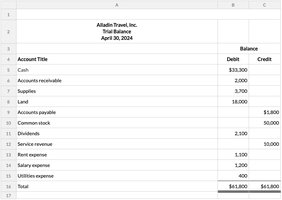

Constructing a Trial Balance

A trial balance lists all accounts and their balances at the end of a period. It ensures that total debits equal total credits and facilitates the preparation of financial statements.

Assets listed first, then liabilities, then equity.

Used to detect errors in recording.

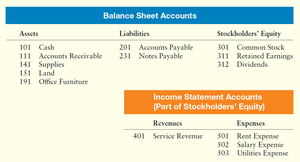

Chart of Accounts

A chart of accounts is a listing of all account titles and numbers used by a business. It organizes accounts for efficient record-keeping and reporting.

Machine Learning in Accounting and Business

Machine learning is a subset of artificial intelligence where computers learn from data without explicit programming. In accounting, machine learning can automate tasks such as identifying general ledger account names for transactions, fraud detection, and financial forecasting.

Supervised learning: Predicts outcomes based on labeled data (e.g., spam filters).

Unsupervised learning: Finds patterns or clusters in unlabeled data (e.g., recommendation systems).

Programming languages: Python (most popular), R, Julia, Java.

Summary Table: Types of Accounts

Type | Examples | Normal Balance |

|---|---|---|

Assets | Cash, Accounts Receivable, Inventory, Land | Debit |

Liabilities | Accounts Payable, Notes Payable | Credit |

Stockholders' Equity | Common Stock, Retained Earnings, Dividends | Credit (except Dividends: Debit) |

Revenues | Service Revenue, Sales | Credit |

Expenses | Rent Expense, Salary Expense, Utilities Expense | Debit |

Example: Alladin Travel, Inc. records transactions such as issuing stock, purchasing land, earning revenue, and paying expenses, each affecting the accounting equation and individual accounts.

Additional info: Academic context was added to clarify the expanded accounting equation, machine learning applications, and the structure of the chart of accounts.