Back

BackChapter 2: Transaction Analysis – Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Transaction Analysis

Recognizing Business Transactions and Types of Accounts

Business transactions are events with a financial impact on a company that can be measured reliably. Each transaction involves an exchange: something is given and something is received. Accounting records both sides of every transaction, ensuring objective information about the financial impact.

Transaction: Any event affecting the financial position of a business.

Account: A record of all changes in a particular asset, liability, or stockholders’ equity during a period.

Types of Accounts:

Assets: Economic resources providing future benefit (e.g., cash, accounts receivable, inventory, prepaid expenses, investments, property, plant, and equipment).

Liabilities: Financial obligations to external parties (e.g., accounts payable, notes payable, accrued liabilities).

Stockholders’ Equity: Owners’ claims to assets (e.g., common stock, retained earnings, dividends, revenues, expenses).

The Accounting Equation

The accounting equation expresses the fundamental relationship in accounting:

Assets = Liabilities + Stockholders’ Equity

Assets: Resources owned by the business.

Liabilities: External claims on assets.

Stockholders’ Equity: Internal claims on assets.

Analyzing the Impact of Transactions on the Accounting Equation

Each transaction affects at least two accounts and must keep the accounting equation balanced. For example:

Investment by Owners: Increases assets (cash) and increases stockholders’ equity (common stock).

Purchase of Land: Decreases assets (cash) and increases assets (land).

Purchase on Account: Increases assets (supplies) and increases liabilities (accounts payable).

Revenue Earned: Increases assets (cash or accounts receivable) and increases stockholders’ equity (retained earnings).

Expenses Paid: Decreases assets (cash) and decreases stockholders’ equity (retained earnings).

Examples of Transaction Analysis

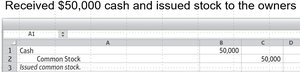

Transaction 1: Owners invest $50,000 cash and receive common stock. Asset (Cash) increases; Stockholders’ Equity (Common Stock) increases.

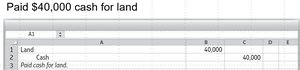

Transaction 2: Paid $40,000 cash for land. Asset (Land) increases; Asset (Cash) decreases.

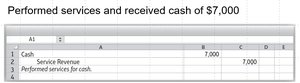

Transaction 4: Performed services and received $7,000 cash. Asset (Cash) increases; Stockholders’ Equity (Service Revenue) increases.

Double-Entry System and T-Accounts

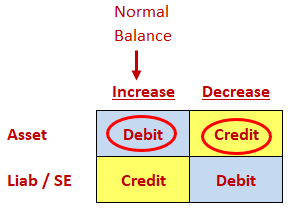

The double-entry system records the dual effects of each transaction. Every transaction affects at least two accounts, using debits and credits to indicate increases or decreases.

Debit: Left side of an account.

Credit: Right side of an account.

T-Account: Visual representation of an account, showing debits on the left and credits on the right.

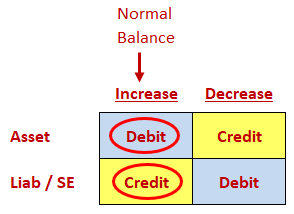

Rules for debits and credits:

Assets: Increase with debits, decrease with credits.

Liabilities and Stockholders’ Equity: Increase with credits, decrease with debits.

Journalizing Transactions and Posting to the Ledger

Journalizing is the process of recording transactions in the journal. Posting transfers the journal entries to the ledger, which houses account balances.

Specify each account affected and the amount.

Determine if each account is increased or decreased (debit or credit).

Record in the journal via a journal entry.

Constructing a Trial Balance

A trial balance lists all accounts with their balances, ensuring that total debits equal total credits. It is usually prepared at the end of the period and facilitates the preparation of financial statements.

Assets listed first, followed by liabilities and stockholders’ equity.

Purpose: To check the accuracy of the ledger and prepare financial statements.

Correcting Accounting Errors

To correct errors, compute the difference between debits and credits in the trial balance, search for missing accounts, and check for slide or transposition errors.

Slide Error: Misplacement of decimal point.

Transposition Error: Reversal of digits (e.g., 54 instead of 45).

Chart of Accounts and Normal Balances

A chart of accounts lists all accounts and their numbers. Normal balances indicate how to increase each account:

Assets: Debit

Liabilities: Credit

Stockholders’ Equity: Credit

Expenses: Debit

Revenues: Credit

Machine Learning in Accounting

Machine learning is a subset of artificial intelligence where machines learn from data without explicit programming. In accounting, machine learning can automate tasks such as identifying general ledger account names for transactions.

Supervised Learning: Task-driven, predicts values (e.g., spam filters).

Unsupervised Learning: Data-driven, identifies clusters (e.g., recommendation systems).

Programming Languages: Python (most popular), R, Julia, Java.

Key Formulas

Accounting Equation:

Expanded Accounting Equation:

Summary Table: Rules of Debit and Credit

Account Type | Increase | Decrease |

|---|---|---|

Asset | Debit | Credit |

Liability | Credit | Debit |

Stockholders' Equity | Credit | Debit |

Revenue | Credit | Debit |

Expense | Debit | Credit |

Dividend | Debit | Credit |