Back

BackChapter 3: The Accounting Information System – Structured Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 3: The Accounting Information System

Overview of the Accounting Cycle

The accounting cycle is a systematic process used by companies to record and report financial transactions over a specific period, such as a month, quarter, or year. It ensures that all financial data is accurately captured and reported in the financial statements.

Accounting Period: The time frame for which financial statements are prepared (e.g., fiscal year).

Cycle Steps: Analyze transactions, record journal entries, post to the general ledger, prepare trial balances, adjust accounts, prepare financial statements, and close temporary accounts.

Start of New Period: The beginning balance of each account equals the ending balance from the previous period.

Types of Companies and Business Models

Companies may operate as merchandising or service entities, each with distinct accounting needs. Merchandising companies sell goods, while service companies provide intangible services.

Merchandising Companies: Record sales, cost of goods sold (COGS), and various expenses.

Service Companies: Focus on revenue from services and related expenses.

Accounts and Chart of Accounts

An account is a standardized record used to accumulate the dollar effects of transactions. The Chart of Accounts is a list of all accounts a company uses to record its transactions.

Common Accounts: Cash, Equipment, Accounts Payable, Notes Payable, Common Shares, Salary Expense, etc.

Purpose: Organize and classify financial information for reporting.

Identifying Transactions

Not all events are recorded in accounting books. Only measurable and realized transactions are recorded.

Examples of Transactions: Issuing shares for cash, borrowing from a bank, purchasing investments, receiving interest, paying salaries.

Non-Transactions: Forecasts, negotiations, or potential events not yet realized.

T-Accounts and Transaction Effects

The T-Account is a visual tool used to record increases and decreases in specific accounts. It helps track the effects of transactions on assets, liabilities, equity, revenues, and expenses.

Structure: Left side is debit (Dr.), right side is credit (Cr.).

Application: Used to analyze which accounts are affected and on which side (debit or credit).

Examples of Transaction Effects

Below are examples of how common transactions affect accounts:

Issuing Common Shares: Debit Cash, Credit Common Shares.

Borrowing from Bank: Debit Cash, Credit Bank Loan.

Buying Investments: Debit Short-term Investments, Credit Cash.

Receiving Interest: Debit Cash, Credit Interest Revenue.

Paying Employees: Debit Salary Expense, Credit Cash.

General Ledger

The General Ledger is a formal record that tracks increases and decreases in each account and shows their balances. It is essential for maintaining accurate financial records.

Journal Entries

A journal entry records the effects of a transaction using debits and credits. Each entry includes a reference number, date, account titles, and amounts.

Double-Entry Accounting: Every transaction affects at least two accounts; total debits must equal total credits.

Accounting Equation: Must always remain balanced.

Rules of Debit and Credit

Debits and credits are used to record increases and decreases in accounts according to the following rules:

Assets: Debit increases, Credit decreases

Liabilities: Debit decreases, Credit increases

Equity: Debit decreases, Credit increases

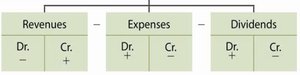

Revenues: Debit decreases, Credit increases

Expenses: Debit increases, Credit decreases

Dividends: Debit increases, Credit decreases

General Journal

The General Journal is the book of original entry, containing a chronological listing of all transactions and events.

Steps in the Accounting System

The accounting system tracks each transaction through three main steps:

Analyze the transaction

Record journal entries in the general journal

Post amounts to the general ledger

Exercises: Laundry Shop Example

Below are sample journal entries and postings for a new business, Laundry Shop, during its first month:

Owner invests $50,000 cash: Debit Cash, Credit Capital Stock

Purchase supplies for $100 cash: Debit Supplies, Credit Cash

Take out $100,000 loan: Debit Cash, Credit Short-term Bank Loan

Purchase $200 supplies on account: Debit Supplies, Credit Accounts Payable

Purchase equipment for $75,000 cash: Debit Equipment, Credit Cash

Perform service for $6,000 cash: Debit Cash, Credit Sales

Pay employee salaries $2,000: Debit Salary Expense, Credit Cash

Pay utilities $1,500: Debit Utility Expense, Credit Cash

The Trial Balance

The Trial Balance is a list of each account and its balance at a specific point in time. It is used to check for errors and ensure that total debits equal total credits.

Structure: Ending debit and credit balances are listed in two columns.

Error Detection: If total debits do not equal total credits, errors may have occurred in journal entries, posting, or balance calculations.

Summary Table: Rules of Debit and Credit

Account Type | Debit (Dr.) | Credit (Cr.) |

|---|---|---|

Assets | Increase | Decrease |

Liabilities | Decrease | Increase |

Common Shares | Decrease | Increase |

Retained Earnings | Decrease | Increase |

Revenues | Decrease | Increase |

Expenses | Increase | Decrease |

Dividends | Increase | Decrease |

Key Equations

The fundamental accounting equation must always be maintained:

Additional info:

All assigned textbook questions from Chapter 3 are recommended for practice.

Adjusting accounts and closing entries are covered in Chapter 4.