Back

BackChapter 3: The Adjusting Process – Financial & Managerial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 3: The Adjusting Process

Learning Objectives

Differentiate between cash basis and accrual basis accounting

Define and apply the time period concept, revenue recognition, and matching principles

Explain the purpose of and journalize and post adjusting entries for deferrals and accruals

Prepare an adjusted trial balance and identify the impact of adjusting entries on financial statements

Describe the accounting cycle and the purpose of a worksheet

Cash Basis vs. Accrual Basis Accounting

Definitions and Key Differences

Accounting methods determine when revenues and expenses are recognized in the financial records. The two primary methods are cash basis accounting and accrual basis accounting.

Cash Basis Accounting: Revenues are recorded when cash is received; expenses are recorded when cash is paid. This method is not allowed under GAAP and is simpler but less accurate for business performance.

Accrual Basis Accounting: Revenues are recorded when earned; expenses are recorded when incurred. This method is used by most businesses and provides a more accurate picture of financial performance.

Example: If a company pays $1,200 for six months of insurance, cash basis records the expense when paid, while accrual basis spreads the expense over six months.

Example: If a company receives $600 for services to be performed over six months, cash basis records revenue when received, while accrual basis spreads revenue over the service period.

The Time Period Concept, Revenue Recognition, and Matching Principles

Time Period Concept

The time period concept assumes business activities can be divided into specific periods (month, quarter, year) for reporting purposes. A fiscal year is any 12 consecutive months, not necessarily matching the calendar year.

Revenue Recognition Principle

The revenue recognition principle guides when to record revenue, requiring a five-step process:

Identify the contract with the customer

Identify performance obligations

Determine the transaction price

Allocate the transaction price to performance obligations

Recognize revenue when each obligation is satisfied

Matching Principle

The matching principle ensures expenses are recorded in the same period as the revenues they help generate, aiming for accurate net income or loss.

Adjusting Entries: Deferrals and Accruals

Purpose and Types

Adjusting entries are made at the end of the accounting period to update accounts for revenues earned and expenses incurred. They are essential for accurate financial statements and fall into two categories:

Deferrals: Recognition of revenue or expense is postponed to a later date. Includes deferred expenses (prepaid expenses) and deferred revenues (unearned revenue).

Accruals: Revenue or expense is recognized before cash is received or paid. Includes accrued expenses and accrued revenues.

Deferrals

Deferred Expenses

Advance payments for future expenses are treated as assets until used. Examples include prepaid rent, office supplies, and depreciation.

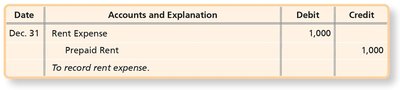

Prepaid Rent: When rent is paid in advance, it is recorded as an asset and expensed as time passes.

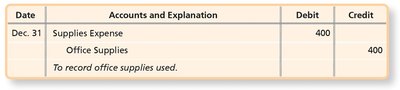

Office Supplies: Supplies purchased are recorded as assets; as they are used, an adjusting entry transfers the used amount to expense.

Depreciation

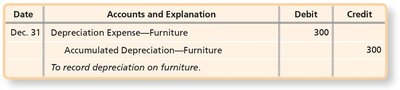

Depreciation allocates the cost of long-lived assets over their useful life. The straight-line method is commonly used:

Example: Furniture costing $18,000, useful life 5 years, no residual value:

per year, or $300$ per month.

Accumulated Depreciation: Contra asset account, paired with the asset and has a credit balance.

Book Value: Asset cost minus accumulated depreciation.

Deferred Revenues

Cash received before services are performed is recorded as a liability (unearned revenue). As services are performed, revenue is recognized.

Accruals

Accrued Expenses

Expenses incurred but not yet paid, such as salaries, interest, and utilities, are recorded with an adjusting entry.

Interest Expense Formula:

Example:

Accrued Revenues

Revenues earned but not yet received are recorded as accounts receivable and service revenue.

Adjusted Trial Balance

Purpose and Preparation

An adjusted trial balance lists all accounts with their adjusted balances after posting adjusting entries. It ensures total debits equal total credits and is used to prepare financial statements.

Impact of Adjusting Entries on Financial Statements

Effects of Not Making Adjusting Entries

Failure to record adjusting entries results in misstated financial statements. For example:

Type of Adjusting Entry | Impact if Not Made |

|---|---|

Deferred Expenses | Expenses understated, assets overstated, net income overstated |

Deferred Revenues | Revenues understated, liabilities overstated, net income understated |

Accrued Expenses | Expenses understated, liabilities understated, net income overstated |

Accrued Revenues | Revenues understated, assets understated, net income understated |

The Accounting Cycle

Steps in the Accounting Cycle

The accounting cycle is a series of steps performed during each accounting period:

Analyze and record transactions

Post to ledger accounts

Prepare unadjusted trial balance

Journalize and post adjusting entries

Prepare adjusted trial balance

Prepare financial statements

Worksheets in Accounting

Purpose and Structure

A worksheet is an internal tool used to organize and summarize data for preparing financial statements. It typically includes:

Account names

Unadjusted trial balance

Adjustments

Adjusted trial balance

Worksheets help ensure accuracy and completeness in the adjusting process.