Back

BackChapter 4: Internal Control and Cash – Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Internal Control and Cash

Learning Objectives

Describe fraud and its impact

Explain the objectives and components of internal control

Evaluate internal controls over cash receipts and cash payments

Prepare a bank reconciliation

Report cash on the balance sheet

Describe unsupervised machine learning and its application to expense reimbursement fraud detection

Fraud and Its Impact

Definition and Types of Fraud

Fraud is the intentional misrepresentation of facts for the purpose of persuading another party to act in a certain way, causing injury or damage. It is a growing problem, especially with the expansion of e-commerce. Common examples include insurance fraud, check forgery, Medicare fraud, credit card fraud, and identity theft.

Misappropriation of assets: Theft of money or inventory, bribery, kickback schemes, and overstated expense reimbursements. Usually committed by employees.

Fraudulent financial reporting: False and misleading journal entries to deceive investors and creditors. Usually committed by managers under pressure to meet results.

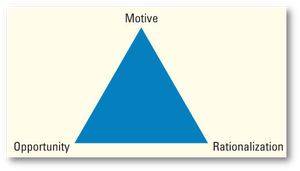

The Fraud Triangle

The fraud triangle explains the three elements that must be present for fraud to occur: motive, opportunity, and rationalization. Weak internal controls often create the opportunity for fraud.

Fraud and Ethics

Fraud has economic, legal, and ethical implications. Perpetrators gain short-term benefits, but others suffer losses. Fraud is illegal and unethical, violating the rights of many for the benefit of a few. Penalties include imprisonment, fines, and damages.

Objectives and Components of Internal Control

Objectives of Internal Control

Internal control is a plan of organization and procedures implemented to accomplish five objectives:

Safeguard assets

Encourage employees to follow company policy

Ensure accurate, reliable accounting records

Comply with legal requirements

Promote operational efficiency

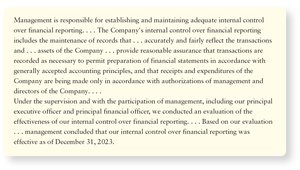

Management Report on Internal Controls

Public companies are required to report on the effectiveness of their internal controls over financial reporting. This includes maintaining accurate records, providing reasonable assurance of proper transactions, and compliance with accounting principles.

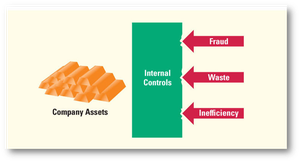

Function of an Internal Control System

Internal controls act as a barrier to protect company assets from fraud, waste, and inefficiency.

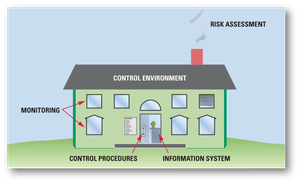

Components of Internal Control

The internal control system consists of five components:

Control Environment: The overall tone at the top, including code of ethics.

Risk Assessment: Identifying and managing business risks.

Information System: Tracking assets, profits, and losses accurately.

Control Procedures: Methods to achieve internal control objectives.

Monitoring of Controls: Ongoing review, often by auditors.

Internal Control Procedures

Preventative and Monitoring Controls

Preventative Controls: Stop fraud or errors before they occur (e.g., smart hiring, separation of duties, limited access, proper approvals).

Monitoring Controls: Detect fraud or errors after they occur (e.g., compliance monitoring, audits, reconciliations).

Examples:

Smart hiring practices: background checks, training, supervision, competitive salaries, clear responsibilities.

Separation of duties: no one person should handle asset handling, record keeping, and transaction approval.

Comparison and compliance monitoring: budgets, exception reporting, audits, reconciliations.

Adequate records: detailed documentation, prenumbered documents, electronic records.

Limited access: physical and electronic controls, passwords, encryption.

Proper approvals: management or delegated department approval, competitive bids.

Safeguard Controls and E-Commerce

Additional controls include fireproof vaults, security cameras, loss prevention specialists, fidelity bonds, mandatory vacations, and job rotation. E-commerce risks require encryption and firewalls to protect data from theft and malware.

Internal Controls Over Cash Receipts and Payments

Cash Receipts Over the Counter and by Mail

Cash is highly susceptible to theft, requiring specific controls. Point-of-sale terminals record sales and inventory changes, and cash drawers are reconciled at the end of shifts. Cash receipts by mail involve multiple steps to ensure proper recording and deposit.

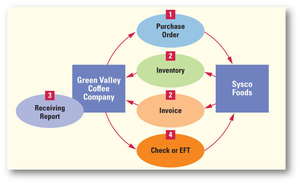

Controls Over Payment by Check or EFT

Payments by check or electronic funds transfer (EFT) provide a record, require authorized signatures, and must be supported by evidence. Duties are split among purchasing, receiving, preparing payment, and approving payment.

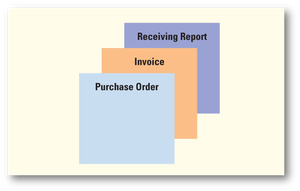

Payment Packet

A payment packet typically includes a purchase order, invoice, and receiving report, which are matched before payment is made.

Petty Cash

Petty cash is used for minor expenses and is managed using the imprest system, where the sum of cash and vouchers equals the specified balance. Debit cards have reduced the need for petty cash funds.

Limitations of Internal Control

Internal controls can be circumvented by collusion, management override, or human error. The cost of controls should not exceed the expected benefits.

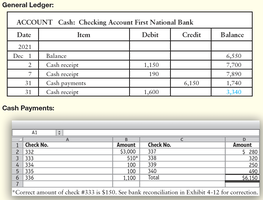

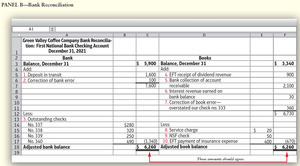

Bank Reconciliation

Documents Used in Bank Control

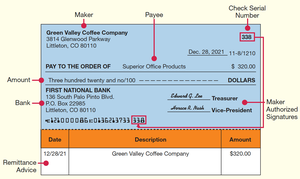

Signature card: Protects against forgery.

Deposit ticket: Records deposits and provides receipts.

Check: Involves a maker, payee, and bank.

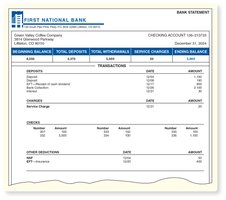

Bank Statement

The bank statement reports cash activity, including beginning and ending balances, receipts, and payments.

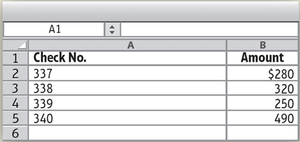

Bank Reconciliation Process

Bank reconciliation explains differences between the company's cash records and the bank balance, often due to timing or errors. The goal is to ensure both balances match after adjustments.

Bank Side Adjustments: Deposits in transit, outstanding checks, bank errors.

Book Side Adjustments: Bank collections, EFTs, service charges, interest revenue, NSF checks, cost of printed checks, book errors.

Bank Reconciliation Table

The following table summarizes the reconciliation process:

Bank Side | Book Side |

|---|---|

Add deposits in transit | Add bank collections, interest revenue, EFT receipts |

Subtract outstanding checks | Subtract service charges, NSF checks, EFT payments |

Add/subtract bank errors | Add/subtract book errors |

Journalizing Transactions from Bank Reconciliation

All reconciling items on the book side require journal entries, as these transactions have not yet been recorded by the company.

Reporting Cash on the Balance Sheet

Cash and Cash Equivalents

Cash includes currency, checking and savings accounts, and money market accounts. Cash equivalents are low-risk, highly liquid investments with maturities of three months or less, such as time deposits, certificates of deposit, and high-grade government securities. Stocks like Apple are not cash equivalents due to risk and lack of maturity date.

Unsupervised Machine Learning in Expense Reimbursement Fraud Detection

Application of Machine Learning

Unsupervised machine learning models can detect fraud in employee expense reimbursements by flagging unusual receipts for human investigation. The Association of Certified Fraud Examiners (ACFE) classifies expense reimbursement fraud into four categories: mischaracterized, fictitious, overstated, and multiple reimbursements.

Machine learning can examine every transaction and combine structured and unstructured data.

Helps overcome human error and bias, and keeps up with sophisticated fraudsters.

Practice Problems and Solutions

Bank Reconciliation Practice

Students are encouraged to practice preparing bank reconciliations using provided scenarios, identifying bank or book side, impact on balances, and recording journal entries.

Copyright Notice

This work is protected by copyright laws and is intended solely for instructional use.