Back

BackChapter 5: Merchandising Operations – Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 5: Merchandising Operations

Introduction to Merchandising Operations

Merchandising operations involve businesses that purchase and sell goods, known as merchandise inventory. These businesses can be classified as wholesalers, who sell to retailers, or retailers, who sell directly to consumers. The accounting for merchandising operations differs from service businesses due to the presence of inventory and the need to account for its purchase and sale.

Merchandiser: A business that sells goods to customers.

Merchandise Inventory: Goods held for resale to customers.

Wholesaler vs. Retailer: Wholesalers sell to retailers; retailers sell to end consumers.

The Operating Cycle of a Merchandising Business

The operating cycle for a merchandiser begins with the purchase of inventory, followed by the sale of goods to customers, and concludes with the collection of cash from those sales. This cycle impacts the timing and recognition of revenues and expenses.

Sales Revenue: Income from selling merchandise (not services).

Cost of Goods Sold (COGS): The cost of inventory sold to customers.

Gross Profit: Net Sales Revenue minus COGS.

Operating Expenses: Expenses other than COGS.

Merchandise Inventory Systems

Businesses use inventory systems to track the value of inventory on hand and sold. There are two main systems:

Perpetual Inventory System: Continuously updates inventory records for each purchase and sale.

Periodic Inventory System: Updates inventory records at the end of the period based on a physical count.

Purchasing Merchandise Inventory (Perpetual System)

Recording Purchases

Purchases of inventory can be made with cash or on account. The following journal entries illustrate these transactions:

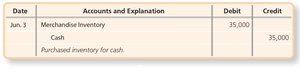

When inventory is purchased for cash:

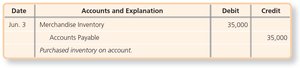

When inventory is purchased on account:

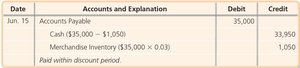

Purchase Discounts

Suppliers may offer discounts for early payment. The discount reduces the cost of inventory. For example, if payment is made within the discount period:

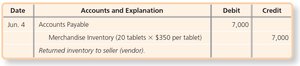

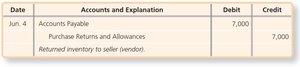

Purchase Returns and Allowances

Returns and allowances occur when goods are defective, damaged, or not as ordered. These reduce the cost of inventory:

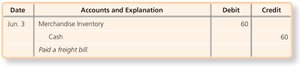

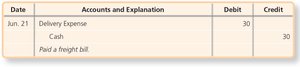

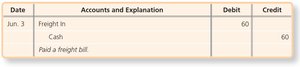

Transportation Costs (Freight In)

Freight costs are added to the cost of inventory if the buyer is responsible for shipping (FOB shipping point). If the seller pays, it is a selling expense (FOB destination).

Example: Buyer pays freight (added to inventory):

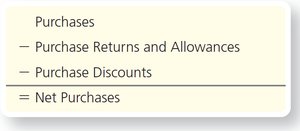

Net Cost of Inventory Purchased

The net cost of inventory purchased is calculated as:

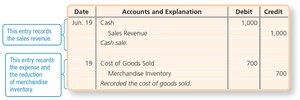

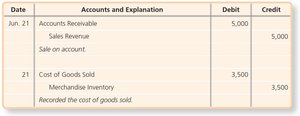

Sales of Merchandise Inventory (Perpetual System)

Recording Sales

Sales transactions require two entries: one for the sale and one for the cost of goods sold.

Example: Cash sale of inventory:

Example: Sale on account:

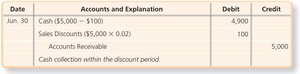

Sales Discounts

Sales discounts are offered to customers for early payment and are recorded as a contra account to Sales Revenue.

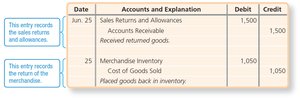

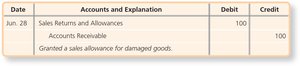

Sales Returns and Allowances

When customers return goods or receive allowances, these are recorded as contra accounts to Sales Revenue.

Example: Sales return and allowance:

Example: Sales allowance for damaged goods:

Transportation Costs (Freight Out)

Freight out is a selling expense when the seller pays for shipping goods to customers.

Net Sales Revenue and Gross Profit

Calculating Net Sales Revenue

Net Sales Revenue is calculated by subtracting sales returns, allowances, and discounts from Sales Revenue:

Example calculation:

Calculating Gross Profit

Gross profit is the difference between net sales revenue and cost of goods sold:

Adjusting and Closing Entries for Merchandisers

Inventory Shrinkage

Inventory shrinkage is the loss of inventory due to theft, damage, or errors. Adjustments are made based on physical counts.

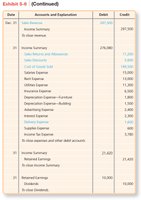

Closing Entries

Closing entries for a merchandiser involve closing revenues, expenses, and contra revenue accounts to Income Summary, then closing Income Summary and Dividends to Retained Earnings.

Financial Statements for Merchandisers

Income Statement Formats

There are two main formats for income statements:

Single-Step Income Statement: Lists all revenues and expenses with no subtotals.

Multi-Step Income Statement: Includes subtotals such as gross profit and operating income, and separates operating from non-operating items.

Operating expenses are divided into selling and administrative expenses. Gross profit minus operating expenses equals operating income.

Statement of Retained Earnings and Balance Sheet

The statement of retained earnings is similar for merchandisers and service businesses. The balance sheet for a merchandiser includes Merchandise Inventory as a current asset.

Gross Profit Percentage

Evaluating Business Performance

The gross profit percentage measures the profitability of each sales dollar above the cost of goods sold. A higher percentage indicates better profitability.

Periodic Inventory System (Appendix 5A)

Recording Purchases and Returns

In a periodic system, inventory is updated at the end of the period. Purchases, returns, and discounts are recorded in separate accounts. Net purchases are calculated as:

Example: Recording purchase returns and allowances:

Recording Transportation Costs

Freight in is recorded separately and added to net purchases.

Sales and Adjusting Entries

Sales, sales discounts, and sales returns and allowances are recorded similarly to the perpetual system. No adjustment is required for inventory shrinkage in the periodic system. Temporary accounts are closed via the Income Summary.

Preparing Financial Statements

Financial statements are prepared at the end of the period using the adjusted balances from the periodic system.

Additional info: These notes are based on Chapter 5 of a standard financial accounting textbook and are suitable for exam preparation in a college-level financial accounting course.