Back

BackChapter 7: Internal Control and Cash – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Internal Control and Cash

Introduction

This chapter explores the principles and procedures of internal control, focusing on safeguarding assets, ensuring reliable accounting, and promoting operational efficiency. Special emphasis is placed on cash management, including receipts, payments, petty cash, card sales, bank reconciliations, and performance evaluation using the cash ratio.

What Is Internal Control?

Definition and Objectives

Internal control is the organizational plan and all related measures adopted by an entity to safeguard assets, encourage adherence to company policies, promote operational efficiency, and ensure accurate and reliable accounting records.

Key objectives include:

Safeguarding assets

Encouraging employees to follow company policies

Promoting operational efficiency

Ensuring accurate, reliable accounting records

The Sarbanes-Oxley Act (SOX) and Internal Control

The Sarbanes-Oxley Act (SOX) was enacted to address accounting scandals and requires public companies to maintain and report on internal controls.

SOX provisions include:

Management must issue an internal control report.

Auditors must evaluate internal controls.

The Public Company Accounting Oversight Board (PCAOB) oversees auditors.

Prohibits auditors from providing certain consulting services to audit clients.

Imposes severe penalties for violations.

Components of Internal Control

Five key components:

Control procedures

Risk assessment

Information system

Monitoring of controls

Control environment

Internal controls are monitored by both internal and external auditors.

Internal Control Procedures

Competent, reliable, and ethical personnel

Assignment of responsibilities

Separation of duties (e.g., separating operations from accounting, and custody of assets from accounting)

Audits (internal and external)

Use of documents and electronic devices (e.g., inventory sensors)

E-commerce controls (encryption, firewalls, passwords, PINs)

Other controls (vaults, alarms, fidelity bonds, mandatory vacations, job rotation)

Data Analytics and Cryptocurrencies

Cryptocurrencies (e.g., Bitcoin, Ethereum) are digital mediums of exchange, not legal tender, and operate on blockchain technology.

They offer resistance to counterfeiting and secure, fast transactions.

Limitations of Internal Control

Internal controls cannot eliminate all fraud, especially collusion (when two or more people work together to circumvent controls).

Controls must balance cost and benefit.

Internal Controls for Cash Receipts

Overview

Cash receipts are primarily from sales of merchandise or services. Each source requires specific security measures to prevent theft and errors.

Cash Receipts by Mail

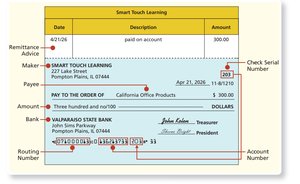

Mailroom employee opens all incoming mail, sending checks to the treasurer and remittance advices to accounting.

Treasurer deposits checks; cashier receives deposit receipt.

Accounting uses remittance advices to record journal entries.

Controller compares bank deposit, accounting records, and deposit receipts for accuracy.

Lock-box systems allow customers to send checks directly to a bank-controlled PO box for added security.

Internal Controls for Cash Payments

Overview

Most payments are made by check, which provides a record, requires authorization, and is supported by documentation.

Controls Over Payment by Check

Controller or treasurer examines the payment packet to ensure:

Goods ordered were received

Payment is for authorized goods only

Correct amount is paid

Streamlined Procedures

Evaluated Receipts Settlement (ERS): Payment approval is compressed into a single step by comparing the receiving report to the purchase order.

Electronic Data Interchange (EDI): Automates routine transactions by allowing direct computer-to-computer communication between customers and suppliers.

Petty Cash: Controls and Accounting

Petty Cash Controls

Petty cash is a small fund for minor expenditures, controlled by:

Designated custodian

Specific fund amount

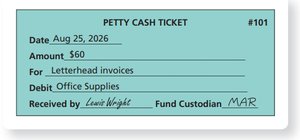

Sequentially numbered petty cash tickets for all payments

Setting Up and Replenishing Petty Cash

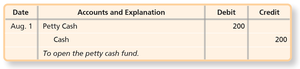

To establish the fund, debit Petty Cash and credit Cash.

Custodian prepares a petty cash ticket for each payment.

Imprest system: Cash plus tickets always equals the fund balance.

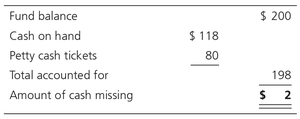

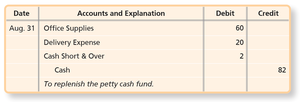

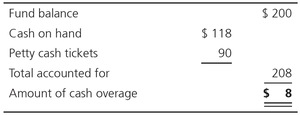

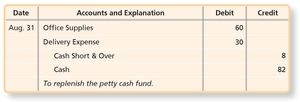

Replenishing the Fund

When cash is low, write a check to replenish the fund.

If cash is missing, record the difference in the Cash Short and Over account.

If there is a cash overage, also record in Cash Short and Over.

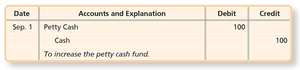

Changing the Petty Cash Fund Amount

To increase the fund, debit Petty Cash and credit Cash for the additional amount.

Internal Controls for Debit and Credit Card Sales

Controls and Recording

Use secure POS terminals and comply with PCI DSS standards.

Never print full card numbers on receipts.

Segregate duties for refunds and reconciliation.

Minimize storage of cardholder data; use encryption and firewalls.

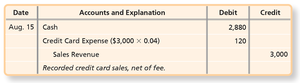

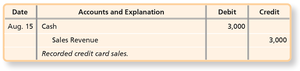

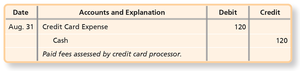

Accounting for Card Sales

Two methods for handling proceeds and fees:

Net method: Deposit is net of processing fee.

Gross method: Deposit is gross; fees are deducted later.

Bank Accounts as Control Devices

Bank Account Controls

Signature cards, deposit tickets, and checks provide documentation and authorization.

Checks specify maker, payee, routing number, and account number.

Bank Statement

Shows beginning and ending balances, transactions, and canceled checks.

Electronic Funds Transfers (EFT)

EFTs transfer cash electronically, reducing costs and increasing speed.

Includes debit card transactions and direct deposits.

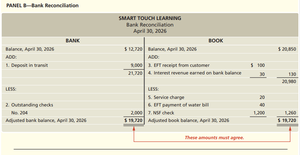

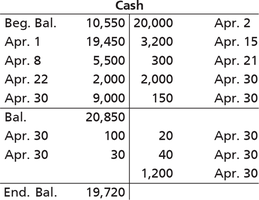

Bank Reconciliation

Purpose and Process

Compares the company’s Cash account with the bank statement to explain differences (timing, errors, etc.).

Bank side: Adjust for deposits in transit, outstanding checks, and bank errors.

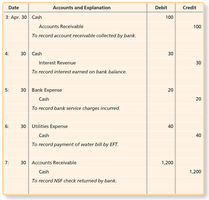

Book side: Adjust for credit memorandums, EFTs, service charges, interest, NSF checks, and book errors.

Journalizing Bank Reconciliation Adjustments

Record all book-side adjustments in the general ledger.

Evaluating Performance: The Cash Ratio

Definition and Application

The cash ratio measures a company’s ability to pay short-term obligations using cash and cash equivalents.

Formula:

Cash equivalents are highly liquid investments convertible to cash within three months.

Summary Table: Key Internal Control Procedures

Area | Key Controls |

|---|---|

Cash Receipts | Segregation of duties, lock-box system, daily deposits, remittance advices |

Cash Payments | Payment packets, authorized signatures, supporting documentation |

Petty Cash | Imprest system, petty cash tickets, periodic replenishment |

Card Sales | Secure POS, PCI DSS compliance, segregation of duties |

Bank Accounts | Bank reconciliation, EFTs, signature cards |