Back

BackChapter 9: Long-Term Liabilities – Bonds, Amortization, and Financial Statement Impact

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Long-Term Liabilities

Introduction to Long-Term Liabilities

Long-term liabilities are obligations that a company expects to pay after one year. The most common types include bonds payable, long-term notes, leases, and deferred income taxes. These liabilities are crucial for financing large investments and operations.

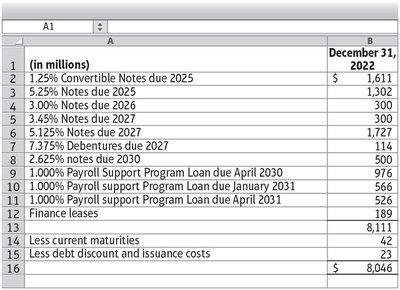

Bonds Payable: Debt securities issued to multiple investors, obligating the issuer to pay interest and repay principal at maturity.

Leases: Contracts allowing the use of assets without ownership.

Deferred Income Taxes: Timing differences between accounting and tax records create future tax obligations.

Bonds Payable: Concepts and Accounting

Bond Basics and Types

Bonds are formal debt instruments where the issuer borrows funds from investors for a defined period at a fixed interest rate. Key terminology includes:

Principal (Face Value): The amount to be repaid at maturity, typically in $1,000 increments.

Maturity Date: The date when the principal is due.

Stated (Coupon) Rate: The fixed interest rate paid to bondholders.

Interest Payment Dates: Usually semiannual.

Types of bonds:

Term Bonds: All mature at the same time.

Serial Bonds: Mature in installments.

Secured Bonds: Backed by specific assets.

Unsecured (Debentures): Backed only by issuer's credit.

Bond Pricing and Market Rates

The price of a bond depends on the relationship between the stated rate and the current market rate:

At Par: Stated rate equals market rate; bond sells at face value.

At Discount: Stated rate is less than market rate; bond sells below face value.

At Premium: Stated rate is greater than market rate; bond sells above face value.

Bonds are quoted as a percentage of face value (e.g., 101.5 means 101.5% of face value).

Case | Stated Rate | Market Rate | Issue Price |

|---|---|---|---|

Par | 9% | 9% | $1,000 |

Discount | 9% | 10% | <$1,000 |

Premium | 9% | 8% | >$1,000 |

Accounting for Bonds at Par

When bonds are issued at par, the cash received equals the face value. The issuer records:

Debit Cash

Credit Bonds Payable

Interest payments are calculated as:

\text{Interest Payment} = \text{Face Value} \times \text{Stated Rate} \times \frac{\text{Months}}{12}$ $

Example: semiannual interest.

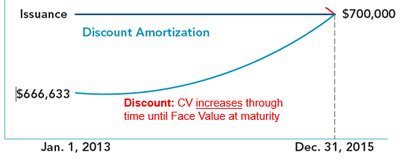

Accounting for Bonds at Discount

If the market rate exceeds the stated rate, bonds are issued below face value. The difference is recorded as a discount (contra-liability):

Debit Cash (proceeds)

Debit Discount on Bonds Payable

Credit Bonds Payable (face value)

The discount is amortized over the bond's life, increasing interest expense above the cash paid.

Accounting for Bonds at Premium

If the stated rate exceeds the market rate, bonds are issued above face value. The excess is recorded as a premium (adjunct-liability):

Debit Cash (proceeds)

Credit Premium on Bonds Payable

Credit Bonds Payable (face value)

The premium is amortized over the bond's life, reducing interest expense below the cash paid.

Amortization Methods

Two main methods are used to amortize bond discounts and premiums:

Straight-Line Method: Allocates equal amounts each period.

Effective-Interest Method: Allocates based on carrying value and market rate (required by IFRS, permitted by GAAP if not materially different).

International Perspective: IFRS requires the effective-interest method; GAAP allows straight-line if results are similar.

Other Features of Bonds Payable

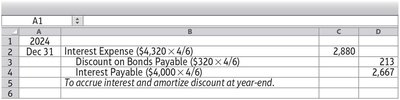

Partial-Period Interest and Amortization

When bonds are issued between interest dates, accrued interest and partial-period amortization must be recorded at year-end. Both interest expense and discount/premium amortization are prorated for the period.

Early Retirement of Bonds

Bonds may be retired before maturity, either by calling them at a set price or purchasing them on the open market. The difference between the carrying value and the retirement price results in a gain or loss.

Callable Bonds: Issuer can redeem before maturity at a specified price.

Gain on Retirement: Retirement price < carrying value.

Loss on Retirement: Retirement price > carrying value.

Convertible Bonds

Convertible bonds can be exchanged for a predetermined number of shares of the issuer's stock. This feature is attractive to investors and may allow the issuer to offer a lower interest rate.

Other Long-Term Liabilities

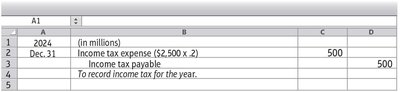

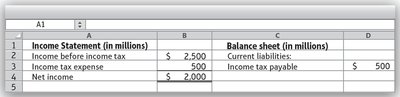

Deferred Income Taxes

Deferred income taxes arise from temporary differences between accounting income and taxable income, often due to different depreciation methods. These differences create future tax liabilities (or assets).

Income Tax Expense: Based on accounting income (GAAP).

Income Taxes Payable: Based on taxable income (tax law).

Deferred Tax Liability: The future tax owed due to timing differences.

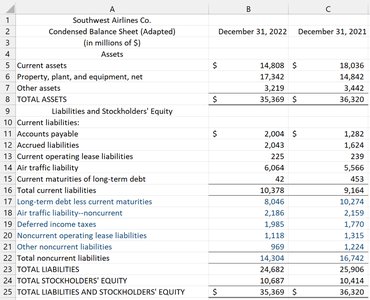

Air Traffic Liability

Airlines recognize liabilities for tickets sold and loyalty points earned but not yet redeemed. These are split into current and noncurrent portions based on expected redemption timing.

Leases

Leases allow companies to use assets without purchasing them. Under GAAP, both finance and operating leases are capitalized, meaning the asset and the related liability are recorded on the balance sheet.

Financial Statement Analysis: Leverage and Coverage

The Leverage Ratio

The leverage ratio (equity multiplier) measures the proportion of assets financed by equity:

\text{Leverage Ratio} = \frac{\text{Total Assets}}{\text{Stockholders' Equity}}$ $

A higher ratio indicates greater use of debt financing, which increases risk but can enhance returns.

The Times-Interest-Earned Ratio

This ratio measures a company's ability to cover interest expense with operating income:

\text{Times-Interest-Earned} = \frac{\text{Income from Operations}}{\text{Interest Expense}}$ $

A higher ratio indicates a stronger ability to meet interest obligations.

Reporting Long-Term Liabilities

Balance Sheet Presentation

Long-term liabilities are reported separately from current liabilities. Common categories include bonds payable, leases, deferred taxes, and other noncurrent obligations.

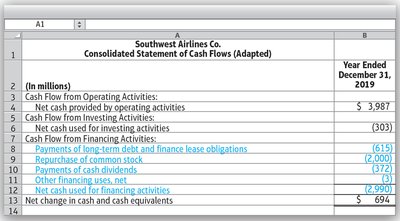

Statement of Cash Flows

Cash flows related to long-term liabilities are reported in the financing section, including proceeds from new debt and repayments of principal.

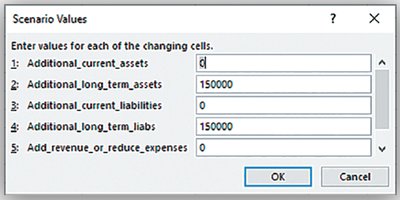

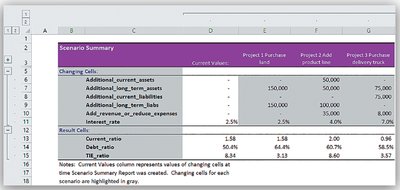

Scenario Analysis and Debt Covenants

Debt Covenants and Compliance

Lenders may impose covenants requiring the borrower to maintain certain financial ratios. Scenario analysis tools, such as Excel's Scenario Manager, help companies evaluate the impact of proposed actions on covenant compliance.

Summary Table: Key Journal Entries

Transaction | Debit | Credit |

|---|---|---|

Issue bond at par | Cash | Bonds Payable |

Issue bond at discount | Cash, Discount on Bonds Payable | Bonds Payable |

Issue bond at premium | Cash | Premium on Bonds Payable, Bonds Payable |

Interest payment (par) | Interest Expense | Cash |

Interest payment (discount) | Interest Expense | Discount on Bonds Payable, Cash |

Interest payment (premium) | Interest Expense, Premium on Bonds Payable | Cash |

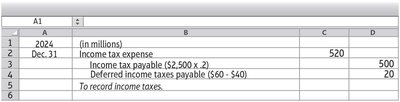

Income tax accrual | Income Tax Expense | Income Taxes Payable, Deferred Income Taxes |

Additional info: This summary covers the core concepts, calculations, and financial statement impacts of long-term liabilities, focusing on bonds, amortization, deferred taxes, and compliance with debt covenants, as outlined in a typical financial accounting curriculum.