Back

BackCompleting the Accounting Cycle: Financial Statements, Closing Entries, and the Accounting Cycle

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 4: Completing the Accounting Cycle

Overview

This chapter covers the final steps in the accounting cycle, including the preparation of financial statements, the use of worksheets, the closing process, post-closing trial balances, and the evaluation of business performance using the current ratio. It also introduces reversing entries as an optional step for simplifying future accounting periods.

Preparing Financial Statements

Types of Financial Statements

Financial statements are formal records that summarize the financial activities and position of a business. The main types include:

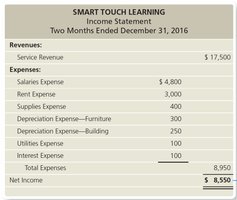

Income Statement: Reports revenues and expenses, calculating net income or net loss for the period.

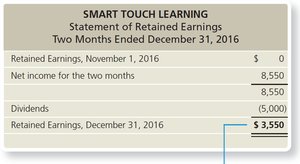

Statement of Retained Earnings: Shows changes in retained earnings over the period, including net income and dividends.

Balance Sheet: Reports assets, liabilities, and stockholders’ equity as of the end of the period.

These statements are prepared from the adjusted trial balance.

Relationships Among Financial Statements

Net income or net loss from the income statement flows to the statement of retained earnings.

Ending retained earnings from the statement of retained earnings flows to the balance sheet.

Classified Balance Sheet

A classified balance sheet organizes assets and liabilities into specific categories:

Assets: Listed in order of liquidity (how quickly they can be converted to cash).

Liabilities: Classified as current (due within one year or operating cycle) or long-term (due after one year).

Stockholders’ Equity: Represents owners’ claims after liabilities are paid, including common stock and retained earnings.

The operating cycle is the time span during which cash is paid for goods and services, which are then sold and collected from customers.

Using the Worksheet to Prepare Financial Statements

Purpose and Structure of the Worksheet

A worksheet is a tool used to organize accounting data and facilitate the preparation of financial statements. Key sections include:

Income Statement Section: Contains only revenue and expense accounts.

Balance Sheet Section: Contains asset, liability, and equity accounts (excluding revenues and expenses).

Net Income/Net Loss Section: The balancing amount for the income statement and balance sheet sections.

The Closing Process

Purpose of Closing Entries

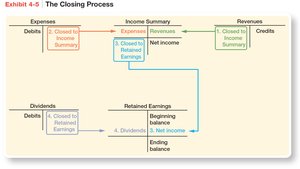

The closing process zeros out all revenue and expense accounts to measure each period’s net income separately. It involves transferring temporary account balances to permanent accounts.

Closing Entries: Transfer revenues, expenses, and dividends to retained earnings, often via an Income Summary account.

Income Summary: Temporarily holds the net income or net loss for the period before transferring to retained earnings.

Steps in the Closing Process

Close revenue accounts to Income Summary.

Close expense accounts to Income Summary.

Close Income Summary to Retained Earnings (net income or loss).

Close Dividends to Retained Earnings.

After closing, only permanent accounts (assets, liabilities, and equity) have balances.

Post-Closing Trial Balance

Purpose and Preparation

The post-closing trial balance is prepared at the end of the accounting cycle. It lists all permanent accounts and their balances after closing entries have been posted, ensuring debits equal credits and that temporary accounts have zero balances.

The Accounting Cycle

Definition and Steps

The accounting cycle is the recurring process of recording, processing, and summarizing financial transactions. The main steps include:

Analyzing transactions

Journalizing transactions

Posting to the ledger

Preparing a trial balance

Making adjusting entries

Preparing an adjusted trial balance

Preparing financial statements

Making closing entries

Preparing a post-closing trial balance

Evaluating Business Performance: The Current Ratio

Definition and Formula

The current ratio measures a company’s ability to pay its current liabilities with its current assets. It is a key indicator of short-term financial health.

Formula:

A higher current ratio indicates greater liquidity and a stronger ability to meet short-term obligations.

Reversing Entries (Appendix 4A)

Purpose and Use

Reversing entries are optional journal entries made at the beginning of a new accounting period to simplify the recording of certain transactions. They are the exact opposite of specific adjusting entries made in the previous period.

Not required by GAAP, but used for convenience.

Commonly used for accrued expenses and revenues.

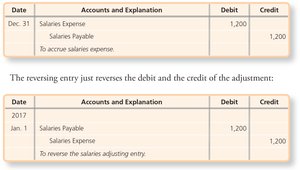

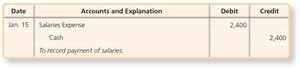

Example: Accrued Salaries

Suppose $1,200 in salaries was accrued at year-end. The adjusting entry and its reversing entry would be:

When the actual salary is paid in the next period, the reversing entry ensures that only the current period’s expense is recorded.

Summary Table: Key Steps in Completing the Accounting Cycle

Step | Description |

|---|---|

Prepare Adjusted Trial Balance | Summarizes all accounts after adjustments |

Prepare Financial Statements | Income statement, statement of retained earnings, balance sheet |

Journalize and Post Closing Entries | Close temporary accounts to retained earnings |

Prepare Post-Closing Trial Balance | Ensures only permanent accounts remain open |

Optional: Journalize and Post Reversing Entries | Simplifies recording of certain transactions in the new period |