Back

BackComprehensive Study Notes for Financial Accounting: ACCT 2301 Final Exam Review

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Accounting

The Accounting Equation

The foundation of financial accounting is the accounting equation, which represents the relationship between a company's resources and the claims on those resources. The equation is:

Assets = Liabilities + Stockholders’ Equity

Assets are resources owned by the company.

Liabilities are obligations to creditors.

Stockholders’ Equity represents the owners’ claims on the business.

Expanded equation:

Assets = Liabilities + Common Stock + Retained Earnings

Retained Earnings = Revenues – Expenses – Dividends

Net Income increases retained earnings, while dividends decrease it. Revenues are earned by providing goods/services, and expenses are sacrifices made to earn those revenues.

Transaction Analysis

Types of Business Transactions

Business events are called transactions and are classified as follows:

Asset Source Transaction: Increases both assets and claims (e.g., acquiring assets from owners, borrowing from creditors, earning from operations).

Asset Use Transaction: Decreases both assets and claims.

Asset Exchange Transaction: One asset increases, another decreases (no net change in total assets).

Claims Exchange Transaction: One claim increases, another decreases (no net change in total claims).

Financial Statements

The Four Financial Statements

Balance Sheet: Shows assets, liabilities, and stockholders’ equity at a point in time.

Income Statement: Reports revenues, expenses, and net income for a period.

Statement of Changes in Stockholders’ Equity: Details changes in common stock and retained earnings.

Statement of Cash Flows: Summarizes cash inflows and outflows from operating, investing, and financing activities.

These statements are interrelated, a concept known as articulation.

Accrual Accounting Concepts

Accrual vs. Cash Accounting

Accrual Accounting: Revenues are recognized when earned, expenses when incurred, regardless of cash flow. Required by GAAP.

Cash Accounting: Revenues and expenses are recognized only when cash is received or paid. Not allowed under GAAP.

Accrual accounting provides a better match of revenues and expenses and is a better predictor of future net income.

Accrued and Deferred Items

Accrued Revenue: Service performed before cash is received; record revenue and receivable, then cash collection.

Accrued Expense: Expense incurred before cash is paid; record expense and payable, then cash payment.

Deferred Expense (Prepaid): Cash paid before expense is recognized; record asset, then adjust for amount used.

Deferred Revenue (Unearned): Cash received before revenue is earned; record liability, then adjust as revenue is earned.

Merchandising Operations & Inventory

Inventory Transactions

Inventory: Asset representing goods held for sale.

Cost of Goods Sold (COGS): Expense recognized when inventory is sold.

Purchases can be for cash or on account; returns, allowances, and discounts affect inventory and accounts payable.

Inventory Cost Flow Methods

FIFO (First-In, First-Out): Oldest costs to COGS, newest remain in inventory.

LIFO (Last-In, First-Out): Newest costs to COGS, oldest remain in inventory.

Weighted-Average: Average cost per unit applied to both COGS and ending inventory.

Specific Identification: Actual cost tracked for each item.

Lower-of-Cost-or-Market (LCM) Rule

Inventory is reported at the lower of its historical cost or market value. If market value drops below cost, inventory is written down and an expense is recognized.

Receivables and Investments

Uncollectible Accounts

Allowance for Doubtful Accounts: Contra-asset reducing accounts receivable to net realizable value.

Uncollectible Accounts Expense: Estimated as a percentage of sales on account.

Write-offs do not affect net income or total assets.

Notes Receivable and Interest

Interest is calculated as

Interest revenue is recognized as it is earned, regardless of cash collection.

Long-Lived Assets

Property, Plant, and Equipment (PPE)

Recorded at historical cost, including all costs to get the asset ready for use.

Depreciation allocates the cost of PPE over its useful life (except land).

Straight-line depreciation:

Book Value = PPE – Accumulated Depreciation

Intangible Assets

Include trademarks, patents, copyrights, franchises, and goodwill.

Amortized over useful or legal life if identifiable; indefinite-life intangibles are tested for impairment.

Current Liabilities

Notes Payable and Interest

Interest expense is recognized over the life of the note.

At maturity, both principal and interest are paid.

Sales Tax Payable

Sales tax collected from customers is a liability, not revenue.

Remitted to the taxing authority when due.

Payroll Accounting

Employee deductions (withholdings) and employer payroll expenses are recorded separately.

Gross pay – deductions = net pay (paid to employees).

Employer payroll taxes and benefits are additional expenses.

Time Value of Money

Interest Calculations

Simple interest:

Used for notes receivable/payable and bonds.

Long-Term Liabilities

Bonds Payable

Companies may issue bonds to borrow from the public.

Interest is paid periodically; principal is repaid at maturity.

EBIT (Earnings Before Interest and Taxes) and Times Interest Earned Ratio measure solvency.

Stockholders' Equity

Dividends

Dividends are declared by the board and paid to shareholders.

Three key dates: Declaration Date (liability created), Date of Record (who receives dividend), Payment Date (cash paid).

Preferred stock may be cumulative or noncumulative, affecting dividend allocation.

Statement of Cash Flows

Classification of Cash Flows

Operating Activities: Cash flows from core business operations.

Investing Activities: Cash flows from buying/selling assets.

Financing Activities: Cash flows from transactions with owners and creditors.

Financial Statement Analysis

Liquidity and Solvency Ratios

Current Ratio:

Measures short-term liquidity; higher is better.

Solvency focuses on total assets vs. total liabilities for long-term financial health.

GAAP vs IFRS

Generally Accepted Accounting Principles (GAAP) are the accounting standards used in the United States, while International Financial Reporting Standards (IFRS) are used internationally. Key differences exist in areas such as inventory costing, asset valuation, and revenue recognition.

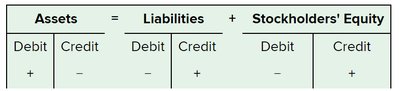

Appendix: Debits and Credits

Normal Balances and T-Accounts

Each account has a normal balance side, which is the side that increases the account. Assets have a normal debit balance, while liabilities and equity have a normal credit balance. Revenues increase equity (credit), while expenses and dividends decrease equity (debit).

Journal entries are used to record transactions, always listing debits first and credits second. At the end of the period, temporary accounts (revenues, expenses, dividends) are closed to retained earnings.

Additional info: These notes are structured to provide a comprehensive review for a college-level financial accounting course, covering all major topics relevant to introductory and intermediate accounting.