Back

BackComprehensive Study Notes for Managerial and Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 2: Building Blocks of Managerial Accounting

Types of Businesses

Businesses can be classified based on the nature of their operations and inventory requirements.

Service: Provides services, no inventory.

Merchandising: Sells objects they purchase; maintains inventory.

Manufacturing: Produces and sells objects; maintains three types of inventory: raw materials, work in process, and finished goods.

Value Chain

The value chain represents the sequence of activities that add value to a company's products or services.

Research & Development

Design

Production/Purchases (Product Costs)

Marketing

Distribution

Customer Service (Period Costs)

Direct vs. Indirect Costs

Costs are classified based on their traceability to a cost object.

Direct Costs: Easily traced to a cost object (e.g., direct materials, direct labor).

Indirect Costs: Cannot be traced directly; must be allocated (e.g., indirect materials, indirect labor, overhead such as supervision, insurance).

Product vs. Period Costs

Product Costs: All production costs (Direct Materials, Direct Labor, Manufacturing Overhead).

Period Costs: All non-production costs (sales, admin, R&D, marketing, customer service).

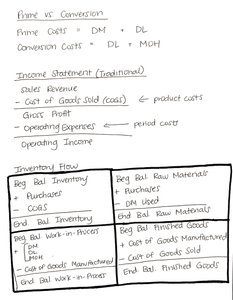

Prime vs. Conversion Costs

Prime Costs: Direct Materials + Direct Labor

Conversion Costs: Direct Labor + Manufacturing Overhead

Income Statement (Traditional)

Sales Revenue

Less: Cost of Goods Sold (COGS) → product costs

Gross Profit

Less: Operating Expenses → period costs

Operating Income

Inventory Flow

Tracks the movement of inventory through various stages in manufacturing.

Raw Materials | Work in Process | Finished Goods |

|---|---|---|

Beg Bal Raw Materials + Purchases - DM Used | Beg Bal WIP + DM Used + DL + MOH - Cost of Goods Manufactured | Beg Bal Finished Goods + Cost of Goods Manufactured - Cost of Goods Sold |

Chapter 3: Job Costing

Process vs. Job Costing

Different costing systems are used based on the nature of production.

Process Costing: Used for large batches of identical products.

Job Costing: Used for smaller batches or unique products; also used for services.

Job Cost Record

Direct Materials (DM): Trace amount directly to job.

Direct Labor (DL): Trace amount (DL hours × rate per hour).

Manufacturing Overhead (MOH): Allocated using a predetermined rate.

Total Job Cost / Manufacturing Cost = DM + DL + MOH

Chapter 4: Activity-Based Costing, Lean Operations, and the Costs of Quality

Cost Distortion & Activity-Based Costing (ABC)

Cost distortion occurs when products/jobs are over- or under-costed due to simplistic allocation methods. ABC provides a refined approach by allocating indirect costs based on activities.

Identify activities and estimate total indirect costs for each.

Select allocation base for each activity.

Calculate activity rates.

Allocate costs to jobs based on actual usage.

ABC is more accurate as it considers the specific resources each product/job uses and the extent of their usage.

Total Quality Management (TQM) & Costs of Quality

TQM is a management philosophy focused on consistently generating high-quality goods/services. Costs of quality are categorized as follows:

Prevention: Avoid producing poor quality.

Appraisal: Detect poor quality.

Internal Failure: Fix/rework/scrap poor quality before delivery to customer.

External Failure: Costs after poor quality reaches the customer.

Chapter 6: Cost Behavior

Variable, Fixed, and Mixed Costs

Understanding cost behavior is essential for planning and decision-making.

Variable Costs: Change in total with volume; per unit cost remains constant. Formula:

Fixed Costs: Total cost remains constant regardless of units produced; per unit fixed cost changes inversely with volume. Formula:

Mixed Costs: Contain both fixed and variable components. Formula:

High-Low Method & Regression Analysis

Used to separate mixed costs into variable and fixed components.

Identify high and low activity points.

Calculate slope (variable cost per unit):

Use one point to solve for fixed cost:

Regression analysis uses all data points to find the line of best fit.

Chapter 7: Cost-Volume-Profit Analysis

Contribution Margin

The contribution margin is the difference between sales revenue and variable expenses. It represents the amount available to cover fixed expenses and generate profit.

CM per unit = Sales Price per unit - Variable Expense per unit

CM Ratio =

Break-even Point (units) =

Break-even Point (sales) =

Income Statement Formats

Traditional Income Statement: Sales Revenue - COGS = Gross Profit - Operating Expenses = Operating Income

Contribution Margin Income Statement: Sales Revenue - Variable Expenses = Contribution Margin - Fixed Expenses = Operating Income

Chapter 8: Relevant Costs for Short-Term Decisions

Relevant Information

Relevant costs pertain to the future and differ among alternatives. Sunk costs are not relevant.

Keys to Decision Making

Focus on relevant costs/revenues only.

Separate variable and fixed costs (e.g., contribution margin).

Special Orders, Discontinue, Outsourcing, and Constraints

Special Orders: Consider incremental revenue and costs.

Discontinue?: Consider lost contribution margin and avoidable fixed expenses.

Outsourcing (Make or Buy): Compare variable and fixed costs to purchase price.

Product Mix with Constraints: Maximize products with highest contribution margin per unit of constraint.

Chapter 9: The Comprehensive Budget

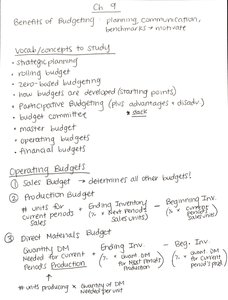

Benefits of Budgeting

Budgeting aids in planning, communication, benchmarking, and motivation.

Key Concepts

Strategic planning, rolling budget, zero-based budgeting, participative budgeting, master budget, budget committee, operating budgets, annual budgets.

Operating Budgets

Sales Budget: Determines all other budgets.

Production Budget: Units to produce = Sales + Ending Inventory - Beginning Inventory.

Direct Materials Budget: Quantity needed for production + Ending Inventory - Beginning Inventory.

Direct Labor Budget: Units to produce × DL hours per unit × DL rate per hour.

MOH and Other Expenses Budgets: Total fixed and variable costs per unit.

Financial Budgets

Capital Expenditures Budget: Plans for purchasing capital investments.

Cash Collections Budget: Forecasts cash inflows from sales.

Cash Payments Budget: Forecasts cash outflows for purchases and expenses.

Combined Cash Budget: Summarizes cash position before financing.

Chapter 10: Performance Evaluation

Decentralization

Dividing a company into segments with their own decision-making responsibilities.

Advantages: Faster response, expert knowledge, improved relations, motivation, retention.

Disadvantages: Duplication of costs, goal incongruence.

Responsibility Centers

Cost Center, Revenue Center, Profit Center, Investment Center

Performance Measures

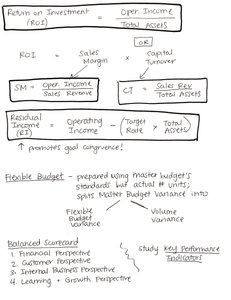

Return on Investment (ROI):

Sales Margin (SM):

Capital Turnover (CT):

Residual Income (RI):

Flexible Budget & Balanced Scorecard

Flexible Budget: Adjusts for actual activity levels.

Balanced Scorecard: Evaluates performance from financial, customer, internal business, and learning/growth perspectives.

Chapter 11: Standard Costs and Variances

Standard Cost

Budgeted cost for one unit, based on standard price and quantity.

DM Price Variance:

DM Quantity Variance:

DL Rate Variance:

DL Efficiency Variance:

Key Concepts

Ideal vs. practical standards, how standards are developed, advantages/disadvantages of using standards and variances.

Chapter 12: Capital Investment Decisions and the Time Value of Money

Capital Budgeting

Capital budgeting involves evaluating and selecting long-term investments.

Identify potential investments.

Estimate cash flows.

Analyze investments using Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR).

Engage in capital rationing and perform post-audits.

Payback Period

Measures how long it takes to recover the initial investment.

Formula:

Does not consider time value of money or profitability.

Accounting Rate of Return (ARR)

Formula:

Does not consider time value of money.

Time Value of Money

Money invested today earns income over time due to interest.

Principal (P), time (t), interest (i).

Present Value (PV) or Future Value (FV):

Net Present Value (NPV)

Formula:

Internal Rate of Return (IRR)

The discount rate that makes NPV = 0; considers the time value of money.