Back

BackComprehensive Study Notes: Introduction to Financial Accounting, VAT, and Subsidiary Journals

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Accounting

Users and Uses of Accounting Information

Accounting information is essential for a variety of stakeholders who rely on financial statements to make informed decisions. The main users and their interests include:

The general public: Interested in the overall health and sustainability of businesses in their community.

Employees and Labour Unions: Assess job security, wage negotiations, and benefits.

Customers: Evaluate the reliability and longevity of suppliers.

Investors: Make decisions about buying, holding, or selling equity.

Lenders: Assess creditworthiness and risk of default.

Suppliers and other trade creditors: Determine the ability of the business to pay for goods and services supplied on credit.

Management: Use information for planning, controlling, and decision-making within the organization.

Government and their agencies: Use information for taxation, regulation, and economic planning.

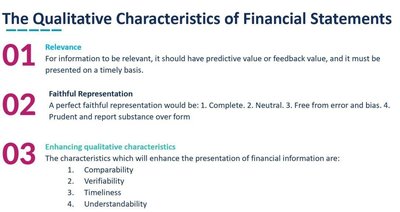

The Qualitative Characteristics of Financial Statements

Financial statements must possess certain qualitative characteristics to be useful for decision-making:

Relevance: Information should have predictive or feedback value and be presented on a timely basis.

Faithful Representation: Information must be complete, neutral, free from error and bias, prudent, and report substance over form.

Enhancing Qualitative Characteristics: These include comparability, verifiability, timeliness, and understandability.

Transaction Analysis

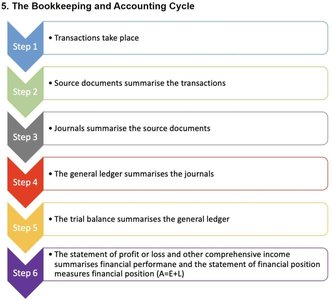

The Bookkeeping and Accounting Cycle

The accounting cycle is a systematic process that ensures all financial transactions are accurately recorded and reported:

Transactions take place: Economic events occur that affect the financial position of the business.

Source documents summarise the transactions: Invoices, receipts, and other documents provide evidence of transactions.

Journals summarise the source documents: Transactions are recorded in the appropriate journals (e.g., sales, purchases, cash receipts, cash payments).

The general ledger summarises the journals: Journal entries are posted to the general ledger accounts.

The trial balance summarises the general ledger: Ensures that total debits equal total credits.

Financial statements: The statement of profit or loss and other comprehensive income measures performance, while the statement of financial position measures financial position ().

Accrual Accounting Concepts

VAT (Value Added Tax) in Financial Accounting

VAT is an indirect tax based on transactions, not assessed directly by the tax authority but collected by vendors on behalf of the government. Key concepts include:

Output VAT: Charged on sales of goods and services by VAT-registered businesses.

Input VAT: Paid on purchases of goods and services; can be claimed back if incurred in making taxable supplies.

Registration: Compulsory if taxable supplies exceed R1 million in 12 months; voluntary if above R50,000 but below R1 million.

Types of Supplies:

Standard-rated (15%)

Zero-rated (0%)

Exempt (no VAT charged or claimable)

Documentation: Tax invoices, debit notes, and credit notes are required to claim input VAT.

VAT Calculation Formulas:

VAT Portion (from inclusive price):

VAT Exclusive Price:

VAT Inclusive Price:

VAT Calculation Steps:

Calculate output tax (income/payments received).

Calculate input tax (expenditures/refunds).

Determine VAT adjustments.

If output tax < input tax, a credit is refundable; if output tax > input tax, a debit is payable.

Examples of VAT Application

Zero-rated supplies (e.g., exports, basic foodstuffs) allow input VAT claims but are taxed at 0%.

Exempt supplies (e.g., financial services, residential accommodation) do not allow input VAT claims.

Some expenses (e.g., entertainment, club memberships, private motor cars) are denied input VAT even if incurred in business.

Merchandising Operations

Subsidiary Journals and Their Purpose

Subsidiary journals are used to group and record similar transactions before posting to the general ledger. Common journals include:

Cash Receipts Journal (CRJ): Records all cash received by the business.

Cash Payments Journal (CPJ): Records all cash payments made by the business.

Purchases Journal (PJ): Records credit purchases of goods and services.

Purchases Returns Journal (PRJ): Records returns of goods previously purchased on credit.

Sales Journal (SJ): Records credit sales of goods and services.

Sales Returns Journal (SRJ): Records returns of goods previously sold on credit.

Petty Cash Journal (PCJ): Records small cash payments made from petty cash.

General Journal (GJ): Used for transactions not fitting into other journals.

Example: Petty Cash Journal

Petty cash is used for small, routine payments. The petty cash journal records these transactions, ensuring proper allocation to expense accounts and VAT where applicable.

All amounts are typically VAT inclusive.

Petty cash is replenished periodically to maintain a fixed imprest amount.

Transaction Analysis and Journal Entries

Sample Transactions and Journal Entries

Transactions must be analyzed to determine the correct journal, VAT treatment, and amounts. For example:

Credit Purchases: Recorded in the Purchases Journal; VAT input is calculated and claimed.

Credit Sales: Recorded in the Sales Journal; VAT output is calculated and paid to the tax authority.

Returns: Purchases returns and sales returns are recorded in their respective journals, adjusting for VAT.

Petty Cash Payments: Recorded in the Petty Cash Journal, with VAT input claimed where applicable.

Example: VAT Calculation

Sold merchandise for R16,330 (VAT inclusive): VAT Output =

Purchased office furniture for R11,895 (VAT exclusive): VAT Input =

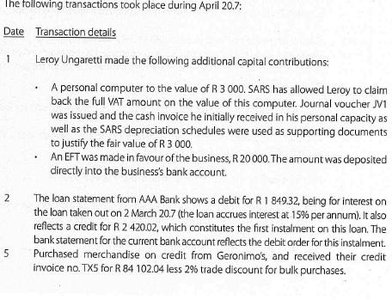

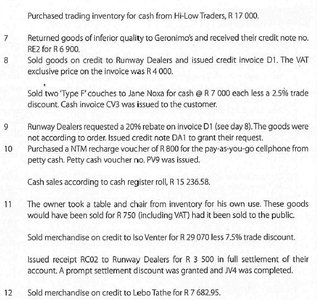

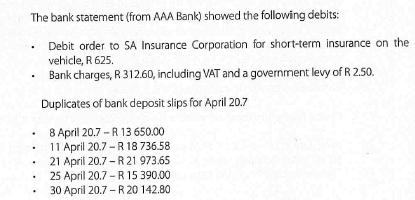

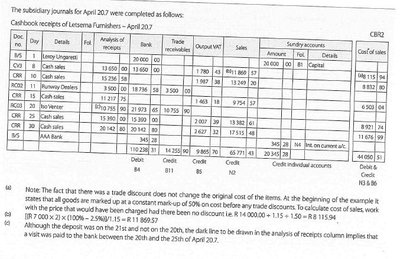

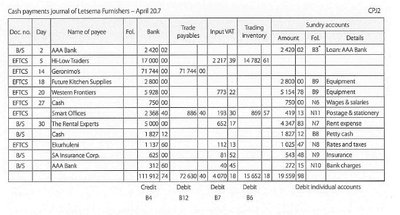

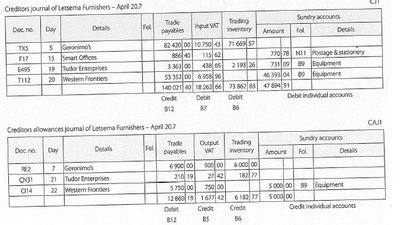

Comprehensive Example: Letesma Furnishers

Transaction Listing and Journal Preparation

A detailed list of transactions for a business (e.g., Letesma Furnishers) is analyzed and recorded in the appropriate journals. This includes capital contributions, purchases, sales, returns, petty cash transactions, and bank transactions. Each transaction is classified, VAT is calculated, and entries are posted to the relevant journals.

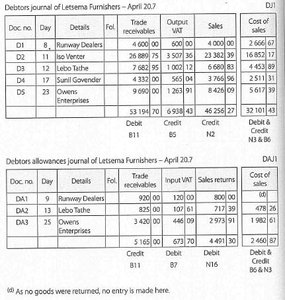

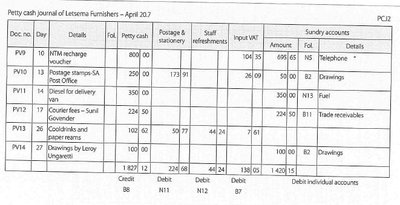

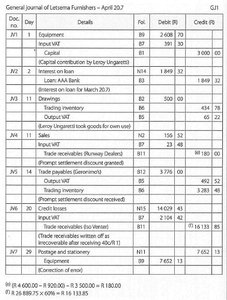

Subsidiary Journals: Completed Examples

Below are examples of completed subsidiary journals for April 20.7, showing how transactions are summarized and VAT is accounted for:

Cash Receipts Journal (CRJ): Summarizes all cash received, including analysis of receipts, VAT, and allocation to sundry accounts.

Cash Payments Journal (CPJ): Summarizes all cash payments, including trade payables, VAT, and allocation to sundry accounts.

Creditors (Purchases) Journal and Creditors Allowances Journal: Record credit purchases and returns, with VAT and allocation to relevant accounts.

Debtors (Sales) Journal and Debtors Allowances Journal: Record credit sales and returns, with VAT and allocation to relevant accounts.

Petty Cash Journal: Records small cash payments, VAT, and allocation to expense accounts.

General Journal: Used for transactions not fitting into other journals, such as corrections, capital contributions, and adjustments.

Key Points to Remember

Every transaction must be recorded in a subsidiary journal before posting to the general ledger.

Subsidiary journals group similar transactions and facilitate analysis and control.

VAT must be correctly calculated and allocated for each transaction.

Proper documentation is essential for VAT claims and compliance.

Understanding the flow from transaction to financial statement is critical for accurate financial reporting.

Additional info:

Examples and templates provided are based on South African VAT legislation (15% standard rate).

All journal examples are for educational purposes and illustrate the process of summarizing and posting transactions in the accounting cycle.