Back

BackConstructing and Understanding the Income Statement for Sole Traders

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Accounting

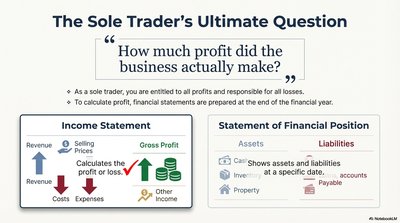

The Sole Trader’s Ultimate Question

Accounting for sole traders centers on determining the actual profit made by the business. Financial statements are prepared at the end of the financial year to answer this question, with the Income Statement and Statement of Financial Position as key documents.

Income Statement: Calculates profit or loss by comparing revenue and expenses.

Statement of Financial Position: Shows assets and liabilities at a specific date.

Key Terms: Revenue, Costs, Expenses, Assets, Liabilities

Transaction Analysis

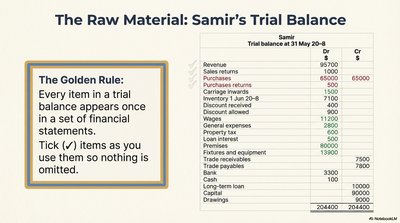

Trial Balance as Raw Material

The trial balance is the starting point for preparing financial statements. Every item in the trial balance appears once in the set of financial statements, ensuring completeness and accuracy.

Golden Rule: Tick items as they are used to avoid omissions.

Application: All ledger entries are transformed into the narrative of business performance.

Accrual Accounting Concepts

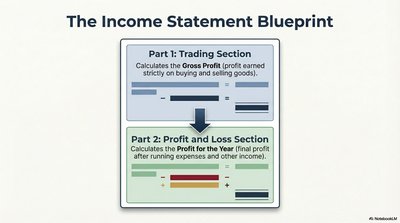

Income Statement Blueprint

The income statement is divided into two main sections: the Trading Section and the Profit & Loss Section. This structure ensures that all relevant revenues and expenses are matched to the period in which they occur.

Trading Section: Calculates gross profit from buying and selling goods.

Profit & Loss Section: Calculates final profit after all expenses and other income.

Merchandising Operations

Building the Income Statement: Step-by-Step Guide

The income statement is constructed in a logical sequence, starting from revenue and ending with net profit. Each step ensures accurate calculation of profit for sole traders.

Start with Revenue (Sales): Total income from business activities before deductions.

Deduct Cost of Goods Sold (COGS): Direct costs attributable to the production of goods sold.

Calculate Gross Profit: Revenue minus COGS.

Subtract Operating Expenses: Indirect costs incurred during normal operations.

Determine Net Profit (Net Income): Gross profit minus total operating expenses.

Inventory

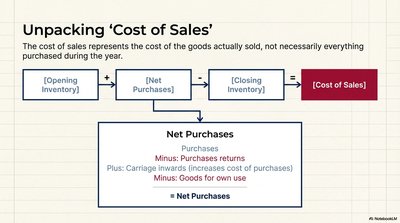

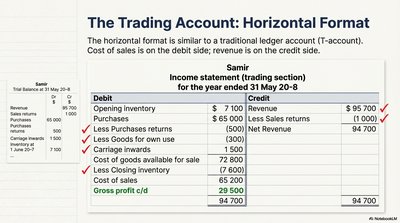

Unpacking 'Cost of Sales'

The cost of sales represents the cost of goods actually sold, not necessarily everything purchased during the year. It is calculated using opening inventory, net purchases, and closing inventory.

Formula: $\text{Cost of Sales} = \text{Opening Inventory} + \text{Net Purchases} - \text{Closing Inventory}$

Net Purchases: Purchases minus purchase returns, plus carriage inwards, minus goods for own use.

Internal Controls and Reporting Cash

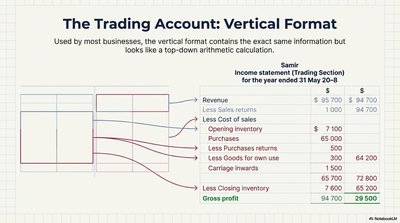

Trading Account Formats

The trading account can be presented in horizontal (T-account) or vertical formats. Both formats show the same information but differ in layout.

Horizontal Format: Debit and credit sides, similar to ledger accounts.

Vertical Format: Top-down arithmetic calculation, used by most businesses.

Financial Statement Analysis

Carrying the Profit Forward

Gross profit is carried forward from the trading section to the profit and loss section, serving as the starting point for calculating final profit.

Purpose: Ensures continuity and accuracy in profit calculation.

Statement of Cash Flows

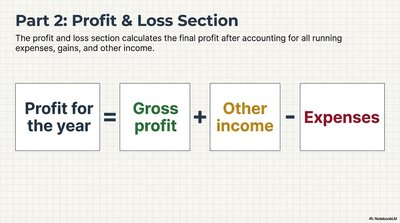

Profit & Loss Section

The profit and loss section calculates the final profit for the year after accounting for all running expenses, gains, and other income.

Formula: $\text{Profit for the year} = \text{Gross profit} + \text{Other income} - \text{Expenses}$

Financial Statement Analysis

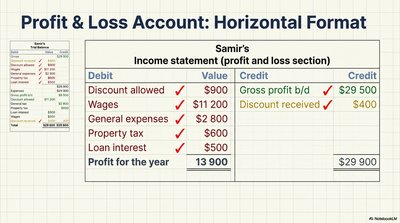

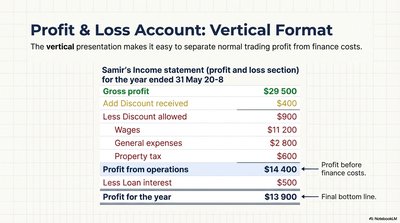

Profit & Loss Account Formats

The profit and loss account can be presented in horizontal or vertical formats, making it easy to separate normal trading profit from finance costs.

Horizontal Format: Shows debits and credits for each item.

Vertical Format: Presents a clear calculation from gross profit to final profit for the year.

Financial Statement Analysis

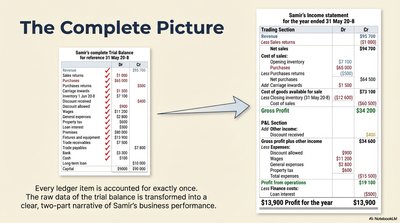

The Complete Picture

Every ledger item is accounted for exactly once. The trial balance is transformed into a clear, two-part narrative of business performance, showing both trading and profit & loss sections.

Application: Ensures comprehensive and accurate financial reporting.

Formulas and Examples

Key Formulas Used in Income Statement Preparation

Gross Profit: $\text{Gross Profit} = \text{Selling Price of Goods} - \text{Cost of Sales}$

Cost of Sales: $\text{Cost of Sales} = \text{Opening Inventory} + \text{Net Purchases} - \text{Closing Inventory}$

Profit for the Year: $\text{Profit for the Year} = \text{Gross Profit} + \text{Other Income} - \text{Expenses}$

Example: Trading Account (Vertical Format)

Item | Amount ($) |

|---|---|

Revenue | 95,700 |

Less Sales Returns | 1,000 |

Net Revenue | 94,700 |

Opening Inventory | 7,100 |

Purchases | 65,000 |

Less Purchases Returns | 500 |

Less Goods for Own Use | 500 |

Carriage Inwards | 700 |

Cost of Goods Available for Sale | 72,800 |

Less Closing Inventory | 67,600 |

Cost of Sales | 5,200 |

Gross Profit | 29,500 |

Example: Profit & Loss Account (Vertical Format)

Item | Amount ($) |

|---|---|

Gross Profit | 29,500 |

Add Discount Received | 400 |

Less Discount Allowed | 900 |

Wages | 11,200 |

General Expenses | 2,800 |

Property Tax | 600 |

Profit from Operations | 14,400 |

Less Loan Interest | 500 |

Profit for the Year | 13,900 |