Back

BackCurrent and Contingent Liabilities: Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Current and Contingent Liabilities

Introduction

This chapter explores the nature, recognition, and accounting for current and contingent liabilities. These obligations are critical for understanding a company's short-term financial health and risk exposure. The chapter also covers the impact of automation on accounts payable processes.

Distinguishing Between Current and Long-Term Liabilities

Definitions and Classification

Current Liabilities: Debts payable in cash within one year (or the operating cycle, if longer) from the balance sheet date. Examples include accounts payable, notes payable, accrued expenses, and unearned revenue.

Long-Term Liabilities: Debts due more than one year from the balance sheet date, such as bonds payable and long-term loans.

Current liabilities are closely tied to a company's operating activities and are settled through cash payments or services.

Examples of Current Liabilities in Operations

Operating Activity | Current Liability |

|---|---|

Purchasing inventory, supplies, paying operating expenses | Accounts payable |

Borrowing money for operations | Notes payable and accrued interest payable |

Paying employees | Accrued salaries, wages, and payroll taxes payable |

Paying income taxes | Accrued income tax payable |

Fulfilling warranty claims | Accrued warranties payable |

Processing advance cash payments from customers | Unearned (deferred) revenue |

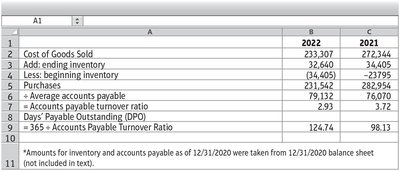

Accounts Payable and Accounts Payable Turnover

Definition and Importance

Accounts Payable: Amounts owed for products or services purchased on account.

Accounts Payable Turnover Ratio: Measures how many times a company pays off its accounts payable during a period, indicating liquidity and payment practices.

Calculating Accounts Payable Turnover

Formula:

"Purchases from suppliers" is not directly on the financial statements and is calculated as:

Days Payable Outstanding (DPO)

Formula:

Indicates the average number of days a company takes to pay its suppliers.

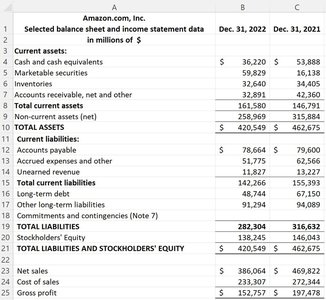

Example: Amazon.com’s Accounts Payable Turnover

Notes Payable and Accrued Interest

Definition and Recognition

Note Payable: A written promise to pay a specified amount at a future date, usually with interest.

Short-term Notes Payable: Due within one year; often used to finance operations.

Journal Entries for Notes Payable

Issuing a note for inventory purchase:

Accruing interest at year-end:

Paying off the note and interest at maturity:

Current Portion of Long-Term Debt

The portion of long-term debt due within one year is reclassified as a current liability at year-end.

Accrued Liabilities and Unearned Revenue

Accrued Liabilities

Expenses recognized as incurred but not yet paid (e.g., salaries, rent, sales tax, commissions).

Examples include sales taxes payable, payroll liabilities, and accrued warranties payable.

Sales Taxes Payable

Sales tax collected from customers is a liability until remitted to the government.

Example journal entry for cash sales and sales tax:

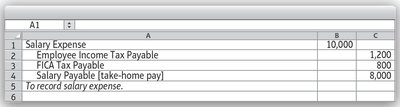

Payroll Liabilities

Includes salary expense, employee income tax payable, FICA tax payable, and salary payable (net pay).

FICA (Social Security) tax is 6.2% up to a wage base; Medicare tax is 1.45% of gross salary.

Example journal entry:

Accrued Warranties Payable

Warranty expense is estimated and accrued in the same period as the related sales revenue.

Example: If sales are $100,000 and estimated warranty claims are 3%, accrue $3,000.

Unearned Revenue

Cash received in advance for goods or services is recorded as a liability until earned.

As the service is performed, unearned revenue is reduced and revenue is recognized.

Contingent Liabilities

Definition and Recognition

Contingent Liability: A potential obligation dependent on the outcome of a future event (e.g., lawsuits, tax disputes).

Accrue if the loss is probable and can be reasonably estimated.

Disclose in notes if the loss is reasonably possible but not probable or not estimable.

No reporting required if the loss is unlikely.

IFRS vs. US GAAP

IFRS uses the term "provision" for obligations more likely than not (>50%) and requires accrual if estimable.

Contingencies under IFRS are only disclosed, not accrued, if less than 50% likely.

Robotic Process Automation (RPA) in Accounts Payable

Role of RPA

RPA can automate repetitive, rule-based tasks in the accounts payable process, such as invoice processing, data entry, and payment approvals.

Benefits include error reduction, audit trails, and freeing employees for higher-value work.

Criteria for RPA Suitability

Tasks are rule-based and repetitive.

High volume of structured data is processed.

Errors in the process are costly.

Expected benefits exceed automation costs.

Summary Table: Common Current Liabilities

Liability | Description |

|---|---|

Accounts Payable | Amounts owed to suppliers for purchases on credit |

Notes Payable | Written promises to pay a specified amount with interest |

Accrued Expenses | Expenses incurred but not yet paid (e.g., salaries, interest) |

Unearned Revenue | Cash received before goods/services are provided |

Sales Tax Payable | Sales tax collected from customers, owed to government |

Payroll Liabilities | Employee compensation and related taxes payable |

Accrued Warranties Payable | Estimated warranty claims on products sold |

Current Portion of Long-Term Debt | Portion of long-term debt due within one year |

Additional info: These notes include expanded academic context, formulas, and examples to ensure completeness and clarity for exam preparation.