Back

BackCurrent and Long-Term Liabilities: Concepts, Calculations, and Financial Statement Analysis

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

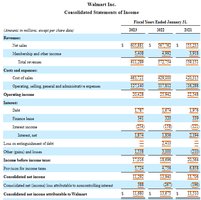

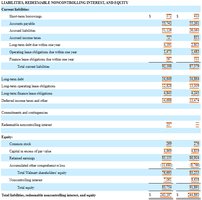

Liabilities in Financial Accounting

Classifications of Liabilities

Liabilities represent obligations that a company must settle in the future, typically through the transfer of assets or provision of services. They are classified based on their maturity:

Current Liabilities: Obligations due within one year or the operating cycle, whichever is longer.

Non-Current (Long-Term) Liabilities: Obligations due beyond one year or the operating cycle.

Proper classification is essential for accurate financial reporting and analysis.

Common Current Liabilities

Accounts Payable: Amounts owed to suppliers for goods and services purchased on credit.

Accrued Liabilities: Expenses incurred but not yet paid (e.g., wages payable, interest payable).

Unearned Revenue: Cash received before services are performed or goods delivered; recognized as a liability until earned.

Payroll Taxes: Taxes withheld from employees and employer payroll tax obligations.

Warranty Liabilities: Estimated costs of fulfilling warranty obligations on sold products.

Short-Term Debt: Notes payable and other borrowings due within one year.

Current Portion of Long-Term Debt: The amount of long-term debt due within the next year.

Common Non-Current Liabilities

Long-Term Notes Payable: Borrowings with maturities greater than one year.

Lease Liabilities: Obligations under lease agreements extending beyond one year.

Bonds Payable: Long-term debt securities issued to investors.

Current and Contingent Liabilities

Notes Payable

Notes payable are formal written promises to pay a specified amount of money at a future date, usually with interest. Key terms include:

Principal: The amount borrowed.

Interest: The cost of borrowing, calculated as principal × annual interest rate × portion of year outstanding.

Maturity Date: The date when the note is due for payment.

Notes with a maturity of one year or less are classified as current liabilities; otherwise, they are non-current.

Example: Notes Payable Journal Entries

Issuance: Dr. Cash $90,000 Cr. Notes Payable $90,000

Year-End Accrual (4 months interest): Dr. Interest Expense $2,700 Cr. Interest Payable $2,700

Interest Payment at Maturity: Dr. Interest Payable $8,100 Cr. Cash $8,100

Principal Payment at Maturity: Dr. Notes Payable $90,000 Cr. Cash $90,000

Formula for Interest:

Payroll Taxes

Employers are responsible for withholding and remitting various payroll taxes:

Employee Withholdings: Federal, state, and local income taxes; FICA (Social Security and Medicare).

Employer Obligations: Unemployment taxes; employer portion of FICA.

Example: For $40,000 in salaries, with 20% federal income tax and 7.65% FICA withheld:

Dr. Salary Expense $40,000

Cr. Employee Income Tax Payable $8,000

Cr. FICA Tax Payable (employee) $3,060

Cr. Salary Payable $28,940

Sales Taxes

Sales taxes are collected from customers and remitted to the government. They are recorded as liabilities until paid.

Example: $10,000 sale with 6.25% sales tax:

Dr. Cash $10,625

Cr. Sales $10,000

Cr. Sales Tax Payable $625

Warranty Liabilities

Estimated warranty costs are recognized as expenses in the period of sale, matching the expense to the related revenue.

Dr. Warranty Expense $30,000

Cr. Accrued Warranty Payable $30,000

Contingent Liabilities

Contingent liabilities depend on future events. They are accounted for as follows:

Accrue: If probable and estimable, record as liability and expense.

Disclose: If reasonably possible or probable but not estimable, disclose in notes.

No Reporting: If unlikely, no action required.

Long-Term Liabilities

Bonds Payable

Bonds are long-term, interest-bearing securities. Key terms include:

Principal (Face Value): Amount paid at maturity.

Coupon Rate: Annual interest rate paid to bondholders.

Maturity Date: Date when principal is repaid.

Issue Price: Amount received at issuance.

Market Interest Rate: Rate demanded by investors.

Bonds may be issued at par, premium, or discount depending on the relationship between coupon and market rates.

Accounting for Bonds Issued at Par

Issuance: Dr. Cash Cr. Bonds Payable

Interest Payments: Dr. Interest Expense Cr. Cash

Maturity: Dr. Bonds Payable Cr. Cash

Example: $10,000 bond, 9% coupon, semi-annual payments:

Coupon per period: $10,000 × 4.5% = $450

Interest expense per period: $450

Partial Year and Accrued Interest

Interest must be accrued at financial statement dates if payment dates do not align. For example, if two months of interest have accrued since the last payment:

Dr. Interest Expense $150

Cr. Interest Payable $150

Early Retirement of Bonds

Bonds may be retired before maturity, resulting in a gain or loss:

Gain: Amount paid < carrying value

Loss: Amount paid > carrying value

Example: Retiring a $10,000 bond for $9,800:

Dr. Bonds Payable $10,000

Cr. Cash $9,800

Cr. Gain $200

Leases

Types of Leases

Financing Lease: Transfers most risks and rewards of ownership to the lessee; capitalized on the balance sheet.

Operating Lease: Does not transfer significant risks and rewards; short-term operating leases (≤12 months) are expensed as incurred.

Lessee Accounting for Leases

Finance Lease: Record a right-of-use asset and a lease liability at the present value of lease payments.

Operating Lease (short-term): Expense lease payments as incurred.

Example: Capitalizing a lease with present value of payments $40,000:

Dr. Lease Asset $40,000

Cr. Lease Liability $40,000

Financial Statement Analysis: Ratios

Times-Interest-Earned Ratio

Measures a company's ability to meet interest obligations:

A higher ratio indicates lower risk of non-payment.

Debt Ratio

Indicates the proportion of assets financed by liabilities:

Higher ratios indicate greater financial risk.

Leverage Ratio (Equity Multiplier)

Shows the degree to which a company is financed by equity versus assets:

Higher leverage indicates more reliance on debt financing.

Summary Table: Key Liabilities and Their Accounting

Liability Type | Definition | Accounting Treatment |

|---|---|---|

Accounts Payable | Amounts owed to suppliers | Record when goods/services received; pay when due |

Notes Payable | Formal written promise to pay | Record principal and accrue/pay interest |

Bonds Payable | Long-term debt securities | Record at issuance; accrue/pay interest; remove at maturity/retirement |

Lease Liabilities | Obligations under lease agreements | Capitalize if finance lease; expense if short-term operating lease |

Payroll Taxes | Taxes withheld and owed | Accrue and remit to authorities |

Warranty Liabilities | Estimated future warranty costs | Estimate and accrue at sale; reduce as costs incurred |

Contingent Liabilities | Potential obligations | Accrue if probable/estimable; disclose if possible; ignore if remote |