Back

BackFinancial Accounting Unit 1: Comprehensive Study Notes and Exam Revision Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Financial Accounting

Nature and Scope of Financial Accounting

Financial accounting involves the systematic recording, classifying, summarising, and reporting of financial transactions to provide useful information for decision-making by both internal and external users. It primarily focuses on historical data and produces general-purpose financial statements.

Development: Evolved from basic record-keeping to double-entry bookkeeping and modern reporting standards. Historical note: Luca Pacioli is credited with formalizing double-entry bookkeeping.

Significance: Provides information on performance, position, and cash flows, aiding investment, lending, tax, credit, and management decisions.

Limitations: Relies on historical cost, estimates, and monetary data; excludes non-financial factors such as staff quality and reputation.

Users: Owners, investors, lenders, creditors, government, employees, managers, and analysts.

Exam sentence: Accounting information supports decision-making but is limited by reliance on estimates, historical cost, and accounting policies, while ignoring important non-financial factors.

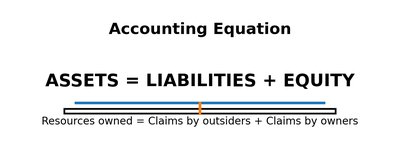

The Accounting Equation

The accounting equation forms the foundation of the double-entry system:

Formula:

Explanation: Resources owned by the business are financed by claims from outsiders (liabilities) and owners (equity).

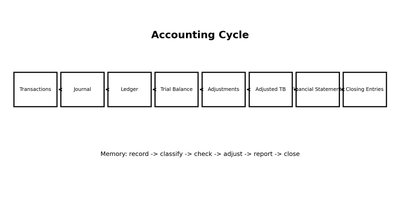

The Accounting Cycle

The accounting cycle is the sequence of steps followed to process financial transactions and prepare financial statements:

Identify transactions

Journalise in books of prime entry

Post to ledger accounts

Prepare trial balance

Make adjustments

Prepare adjusted trial balance

Prepare financial statements

Close temporary accounts

Conceptual Framework and Accounting Principles

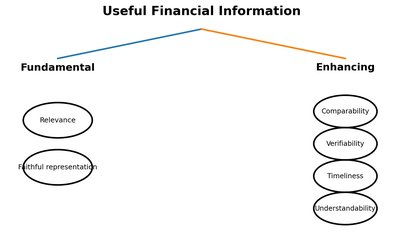

Conceptual Framework of Accounting

The conceptual framework guides the preparation and presentation of financial statements, ensuring consistency and comparability. It helps standard-setters develop standards and assists users in understanding the basis of financial reporting.

Relevance: Information should influence decisions.

Faithful representation: Information must be complete, neutral, and free from material error.

Comparability: Enables users to compare financial data across periods and entities.

Consistency: The same accounting methods should be used unless a valid reason for change exists.

Understandability: Information should be clear to users with reasonable knowledge.

Materiality: Information is material if its omission or misstatement could affect decisions.

Prudence: Do not overstate assets/income or understate liabilities/expenses.

Going concern: Assume the business will continue operating.

Business entity: Treat the owner and business as separate entities.

Revenue recognition: Record revenue when earned.

Matching: Match expenses with the revenue they help generate.

Accounting Methods: Accrual Basis vs Cash Basis

Two primary methods are used to record transactions:

Cash basis: Revenue and expenses are recorded when cash is received or paid. Suitable for simple cash tracking but not for general-purpose financial statements.

Accrual basis: Revenue is recorded when earned, and expenses when incurred, providing a fairer picture of performance by matching income and expenses to the correct period.

Accounting Standards

Accounting standards (e.g., IFRS for SMEs) provide guidelines for measuring, recording, and presenting transactions, ensuring consistency and comparability. The standard-setting process involves identifying issues, research, exposure drafts, feedback, revision, and issuance.

Recording Financial Information

Double-Entry Bookkeeping and Journal Entry Patterns

Every transaction affects at least two accounts, maintaining the balance of the accounting equation. Total debits must equal total credits.

Example: Purchase of asset for cash: Debit Asset, Credit Bank.

Example: Issue of shares for cash: Debit Bank, Credit Share Capital.

Internal Controls and Ethics

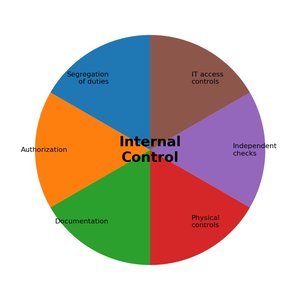

Internal Control Systems

Internal controls are policies and procedures designed to safeguard assets, prevent errors and fraud, improve accuracy, and ensure compliance with policies.

Key areas: Inventory, cash, accounts receivable, accounts payable.

Controls include: Stock counts, bank reconciliations, credit checks, segregation of duties, authorisation, documentation, IT access controls, independent checks, and physical controls.

Auditor Roles

Internal auditor: Reviews controls and operations within the organisation.

External auditor: Provides an independent opinion on the fairness of financial statements.

Ethics and Moral Integrity

Confidentiality: Do not misuse or disclose private information.

Objectivity: Avoid bias and conflicts of interest.

Integrity: Be honest and straightforward.

Collusion: Secret cooperation to commit fraud or bypass controls.

Conflicts of interest: Personal interest clashes with professional duty.

Preparation of Financial Statements

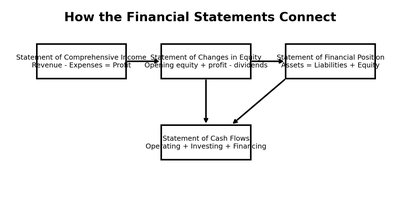

Relationship Among Financial Statements

The main financial statements are interconnected, each serving a distinct purpose but relying on information from the others:

Statement of Comprehensive Income (SOCI): Shows profit or loss (Revenue - Expenses = Profit).

Statement of Changes in Equity (SCE): Tracks changes in equity (Opening equity + profit - dividends).

Statement of Financial Position (SOFP): Presents assets, liabilities, and equity at a specific date.

Statement of Cash Flows: Summarises cash movements from operating, investing, and financing activities.

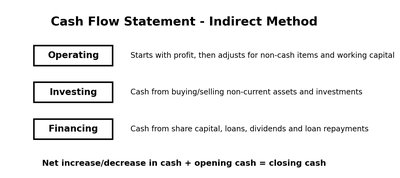

Statement of Cash Flows – Indirect Method

The indirect method starts with profit, adjusts for non-cash items (e.g., depreciation), and changes in working capital to determine cash from operating activities. Investing and financing sections show cash flows from asset transactions and financing activities, respectively.

Formula: Net increase/decrease in cash + opening cash = closing cash

Financial Statement Analysis

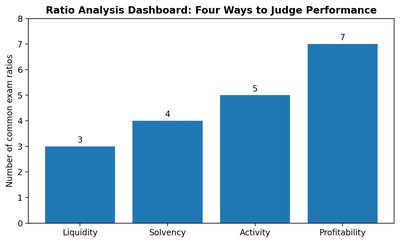

Ratio Analysis

Ratio analysis evaluates a business’s performance and financial health using relationships between financial statement figures. Ratios are grouped into four main categories:

Liquidity: Ability to meet short-term obligations (e.g., current ratio, quick ratio).

Solvency: Long-term risk and reliance on debt (e.g., debt to equity, times interest earned).

Activity: Efficiency in using assets (e.g., inventory turnover, receivables collection period).

Profitability: Ability to generate profit (e.g., gross margin, ROA, ROCE, EPS).

Significance and Limitations of Financial Statements

Significance: Informs investment, lending, and management decisions; allows comparisons; audited statements increase confidence.

Limitations: Historical data may not reflect current value; different policies reduce comparability; estimates and aggregation can obscure detail; inflation can distort figures.

Analysis of Performance

Calculate ratios correctly.

Compare results with previous periods or industry averages.

Explain reasons for changes using figures from statements.

Mention limitations (e.g., one ratio is not enough, different policies, inflation, estimates, industry differences).

Give a balanced conclusion.

Summary Table: Key Financial Ratios

Category | Ratio | Formula | Interpretation |

|---|---|---|---|

Liquidity | Current ratio | Current assets / Current liabilities | Ability to pay short-term debts |

Liquidity | Quick ratio | (Current assets - Inventory) / Current liabilities | Stricter liquidity test |

Solvency | Debt to equity | Debt / Equity × 100 | Financial risk from borrowing |

Activity | Inventory turnover | Cost of sales / Average inventory | Inventory movement efficiency |

Profitability | Gross margin | Gross profit / Sales × 100 | Profit after cost of sales |

Profitability | ROA | Net income / Average total assets × 100 | Profit earned from assets |

Practice Questions

Which principle requires expenses to be recorded in the same period as related revenue? Answer: Matching

Prepare the journal entry to issue shares for cash of $50,000. Answer: Dr Bank $50,000; Cr Share Capital $50,000

A business has current assets of $120,000 and current liabilities of $60,000. Calculate current ratio. Answer:

Explain the difference between liquidation and receivership. Answer: Receivership involves a receiver taking control to recover secured debts; liquidation winds up the entity and distributes proceeds to creditors/owners.

Additional info: These notes are based on the CAPE Unit 1 syllabus and supported by standard accounting references and IFRS for SMEs 2015.