Back

BackFinancial Statements, Balance Day Adjustments, and Cash Budgets – Guided Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

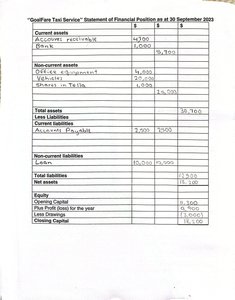

Q1. Complete the Income Statement and Statement of Financial Position for 'GoalFare Taxi Service' for the year ended 30 September 2021.

Background

Topic: Financial Statements Preparation

This question tests your ability to prepare an Income Statement (also known as a Statement of Financial Performance) and a Statement of Financial Position (also known as a Balance Sheet) using a trial balance. You will also need to classify expenses as transportation, administration, or finance costs.

Key Terms and Formulas

Income Statement: Summarizes revenues and expenses to determine profit or loss for the period.

Statement of Financial Position: Shows assets, liabilities, and equity at a specific date.

Key Formula for Profit:

Assets = Liabilities + Equity

Step-by-Step Guidance

Start by identifying all income and expense items from the trial balance. List income (e.g., Fees received) at the top of the Income Statement.

Classify each expense as either Transportation, Administration, or Finance cost. For example, Driver's salary is a transportation expense, while Office rent is an administration expense.

Sum each category of expenses and subtract the total expenses from total income to find the profit or loss for the year (but do not calculate the final value yet).

For the Statement of Financial Position, list all assets (current and non-current), liabilities (current and non-current), and equity items. Make sure the accounting equation balances: Assets = Liabilities + Equity.

Include the profit (or loss) for the year in the equity section, but do not finalize the closing capital calculation yet.

Try solving on your own before revealing the answer!

Final Answer:

The completed Income Statement and Statement of Financial Position will show the calculated profit (or loss) for the year and the balanced assets, liabilities, and equity. The classification of expenses ensures accurate reporting and analysis.

Q2. Classify each item as Revenue, Expense, Asset, Liability, or Equity.

Background

Topic: Classification of Accounts

This question tests your understanding of the five main types of accounts in accounting: Revenue, Expense, Asset, Liability, and Equity. Proper classification is essential for accurate financial reporting.

Key Terms

Revenue: Income earned from business operations.

Expense: Costs incurred in earning revenue.

Asset: Resources owned by the business.

Liability: Obligations owed to outsiders.

Equity: Owner's interest in the business.

Step-by-Step Guidance

Review each item in the list and recall its definition and role in the business.

Decide if the item represents income, an expense, something the business owns, owes, or the owner's claim.

Mark the correct column for each item (do not complete the entire table yet).

Try solving on your own before revealing the answer!

Final Answer:

Each item is classified according to its nature. For example, 'Bank' is an Asset, 'Wages' is an Expense, and 'Capital' is Equity. Accurate classification is crucial for preparing financial statements.

Q3. Prepare an Income Statement for Regina's Real Estate Agency for the year ended 31 March 2016.

Background

Topic: Income Statement Preparation

This question requires you to organize revenue and expenses into an Income Statement format to determine the profit or loss for the period.

Key Terms and Formulas

Income Statement: Summarizes revenues and expenses for a period.

Key Formula:

Step-by-Step Guidance

List all revenue items at the top of the statement (e.g., Commission Received).

Group expenses into Selling, Administration, and Finance Costs as appropriate.

Sum each category and subtract total expenses from total revenue to find profit or loss (do not calculate the final value yet).

Try solving on your own before revealing the answer!

Final Answer:

The completed Income Statement will show the profit or loss for Regina's Real Estate Agency for the year ended 31 March 2016, based on the provided revenues and expenses.