Back

BackGross and Net Profit Computation in Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Application of Gross and Net Profit Computation in Business Case Analysis

Identification and Extraction of Financial Data from Case Studies

Understanding how to identify and extract relevant financial data is essential for accurate profit computation in accounting. The main components include sales (revenue), cost of goods sold (COGS), opening and closing stock, purchases, and expenses.

Sales (Revenue): Total income generated from business activities. Sales may be cash or credit sales, but both are included unless stated otherwise.

Interpretation: Sales represent inflow, not profit.

Example: If a business sells 100 units at TZS 50,000 each, Sales = 100 × 50,000 = TZS 5,000,000.

Cost of Goods Sold (COGS)

COGS is the direct cost of inventory that has been sold during the accounting period. It is a critical figure for determining gross profit.

Formula:

Critical Insight: COGS reflects only sold inventory, not total purchases.

Opening Stock

Opening stock, also called beginning inventory, represents the total value of goods available for sale or use at the start of a financial period. It includes raw materials, work-in-progress (WIP), and finished goods depending on the nature of the business. This figure is crucial because it directly affects the cost of goods sold (COGS), gross profit, cash flow planning, and financial reporting.

Components: Raw Materials, Work-in-Progress, Finished Goods, Supplies, and Obsolete Stock (depending on accounting policies).

Calculation Methods:

Sum of Inventory Components:

Using Sales and COGS Data:

Using COGS and Purchases:

Closing Stock

Closing stock is the value of inventory a business holds at the end of an accounting period, including raw materials, work-in-progress, and finished goods. It is recorded as a current asset on the balance sheet.

Purchases

Purchases refer to saleable goods or merchandise bought in a business. They can be classified as cash or credit purchases.

Cash Purchase: Payment is made immediately using cash or bank transfer. Recorded by debiting the cash account and crediting the expense or asset account.

Credit Purchase: Payment is made after the purchase. Recorded by debiting the purchase account and crediting the creditor's account.

Examples: Stationery purchased by a stationer, cloth by a cloth merchant, cement by a cement dealer.

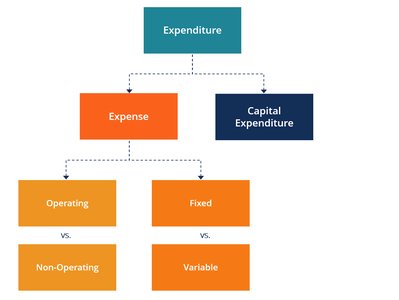

Expenses

An expense is the cost incurred to acquire goods or services, or to operate a business, which is recorded on the income statement and reduces net income. Expenses are recognized when incurred, not necessarily when paid, due to the accrual principle.

Operating Expenses: Day-to-day costs such as salaries, rent, utilities, office supplies, and marketing.

Non-Operating Expenses: Costs not directly tied to core operations, like interest payments or investment losses.

Fixed vs. Variable Expenses: Fixed expenses remain constant (e.g., rent), while variable expenses fluctuate with business activity (e.g., raw materials).

Capital vs. Operational Expenses: Capital expenses involve long-term asset purchases and are depreciated, while operational expenses are consumed within the accounting period.

Types of Expenses

Operating: COGS, marketing, salaries, SG&A, rent, depreciation, etc.

Non-Operating: Interest, taxes, impairment charges.

Fixed: Rent, salaries (sometimes fixed/variable).

Variable: Transaction fees, commissions, marketing (sometimes fixed/variable).

Gross Profit and Cost of Goods Sold

Gross Profit

Gross profit is the difference between net sales revenue and the cost of goods sold. It is a key indicator of a company's profitability from its core activities.

Formula:

Example 1: Laura sells 100 t-shirts for $800 (COGS = $300), Gross Profit = $500.

Example 2: Rich prepares tax returns with no COGS; Gross Profit = Revenue.

Example 3: If annual net sales revenue is $1,000,000 and COGS is $600,000, Gross Profit = $400,000.

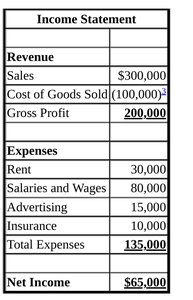

Application Example

Consider a business with sales of $300,000 and COGS of $100,000. The gross profit is $200,000, which is used to cover operating expenses such as rent, salaries, and other costs.

Income Statement Structure

The income statement summarizes revenues, COGS, gross profit, expenses, and net income for a period.

Revenue | |

|---|---|

Sales | $300,000 |

Cost of Goods Sold | ($100,000) |

Gross Profit | $200,000 |

Expenses | |

Rent | 30,000 |

Salaries and Wages | 80,000 |

Advertising | 15,000 |

Insurance | 10,000 |

Total Expenses | 135,000 |

Net Income | $65,000 |

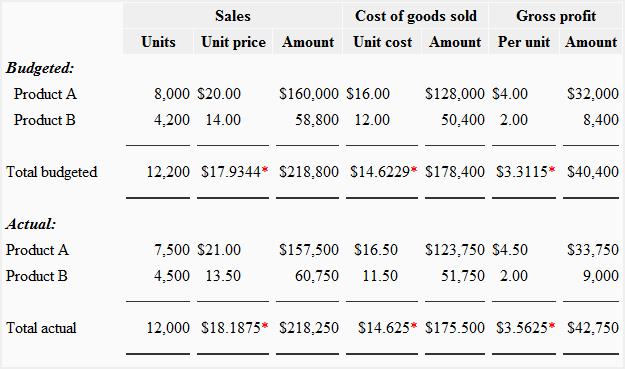

Budgeted vs. Actual Performance Analysis

Comparing budgeted and actual figures for sales, COGS, and gross profit helps businesses assess performance and identify variances.

Sales | Cost of Goods Sold | Gross Profit | ||||||

|---|---|---|---|---|---|---|---|---|

Units | Unit price | Amount | Unit cost | Amount | Per unit | Amount | ||

Budgeted: | ||||||||

Product A | 8,000 | $20.00 | $160,000 | $16.00 | $128,000 | $4.00 | $32,000 | |

Product B | 4,200 | 14.00 | 58,800 | 12.00 | 50,400 | 2.00 | 8,400 | |

Total budgeted | 12,200 | $17.9344* | $218,800 | $14.6229* | $178,400 | $3.3115* | $40,400 | |

Actual: | ||||||||

Product A | 7,500 | $21.00 | $157,500 | $16.50 | $123,750 | $4.50 | $33,750 | |

Product B | 4,500 | 13.50 | 60,750 | 11.50 | 51,750 | 2.00 | 9,000 | |

Total actual | 12,000 | $18.1875* | $218,250 | $14.625* | $175,500 | $3.5625* | $42,750 | |

Practice Questions

Question 1: A business has Sales = $500,000, Cost of Goods Sold = $320,000. Required: Calculate the gross profit. Solution:

Question 2 (Intermediate): A trader reports Sales = $750,000, Opening Stock = $100,000, Purchases = $400,000, Closing Stock = $150,000. Required: Calculate COGS and Gross Profit. COGS: Gross Profit:

Question 3: From a case study: Total sales were $900,000, COGS was 60% of sales. Required: Calculate the gross profit. COGS: Gross Profit:

Additional info: These notes cover core concepts from "Merchandising Operations," "Inventory," and "Gross Profit" computation, which are foundational for financial accounting students.