Back

BackInternal Control, Receivables, and Inventory: Study Guide for Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Internal Control and Cash

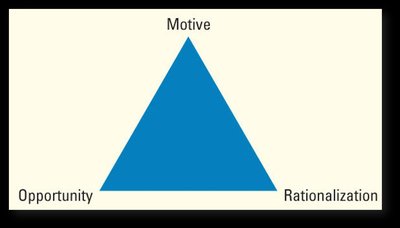

The Fraud Triangle

The fraud triangle is a foundational concept in internal control, explaining the three elements necessary for fraud to occur: motive, opportunity, and rationalization. Understanding these elements helps organizations design controls to prevent fraud.

Motive: The drive or need to commit fraud, often financial pressure.

Opportunity: The ability to commit fraud, usually due to weak internal controls.

Rationalization: The justification or reasoning that makes fraud acceptable to the perpetrator.

Example: An employee with financial difficulties (motive), who finds a way to bypass controls (opportunity), and believes they deserve the money (rationalization).

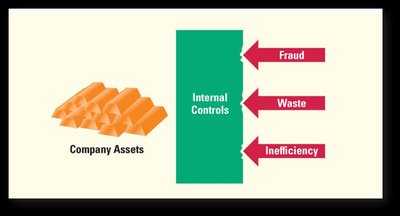

The Function of an Internal Control System

Internal controls are processes and procedures designed to safeguard company assets, prevent fraud, waste, and inefficiency, and ensure accurate financial reporting.

Fraud Prevention: Controls block unauthorized access to assets.

Waste Reduction: Controls ensure resources are used efficiently.

Inefficiency Prevention: Controls streamline operations.

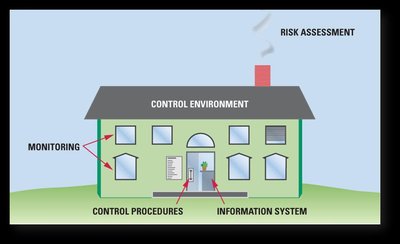

The Components of Internal Control System

An effective internal control system consists of several interrelated components, often illustrated as a house structure. These components work together to ensure the integrity of financial information and asset protection.

Control Environment: The overall attitude, awareness, and actions of management and employees regarding internal controls.

Risk Assessment: Identifying and analyzing risks that may affect the achievement of objectives.

Control Procedures: Policies and procedures that help ensure management directives are carried out.

Information System: The methods used to record, process, and report financial data.

Monitoring: Ongoing evaluations to ensure controls are functioning as intended.

Internal Control Procedures

Internal control procedures are specific actions taken to achieve the objectives of internal control. These include:

Smart Hiring Practices: Background checks, training, supervision, competitive salaries, and clear responsibilities.

Separation of Duties: Dividing asset handling, record keeping, and transaction approval among different employees.

Adequate Records: Maintaining detailed, prenumbered documents for transactions.

Information Technology: Using electronic systems for improved accuracy and speed (e.g., bar codes, sensors).

Cash Receipts by Mail

Cash receipts by mail require strict controls to prevent theft and ensure accurate recording. The process involves several departments and steps.

Mailroom: Receives checks and remittance advices.

Treasurer: Prepares deposit ticket and deposits checks in the bank.

Accounting Department: Records the total amount credited to cash.

Controller: Oversees the process for accuracy.

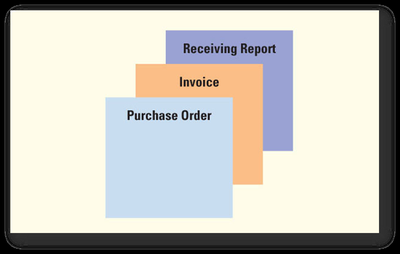

Controls Over Payment by Check

Controls over payment by check involve splitting duties to prevent fraud and errors.

Purchasing goods and receiving goods are handled by different employees.

Preparing checks or EFTs and approval of payment are separated.

Payment Packet: Includes purchase order, invoice, and receiving report to ensure all steps are verified before payment.

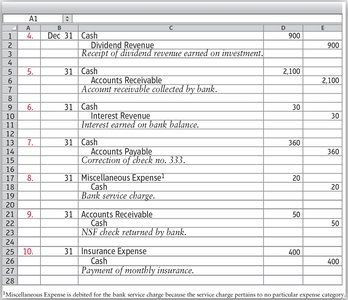

Bank Reconciliation and Journalizing Transactions

Bank reconciliation compares the company's records with the bank's records to identify discrepancies. Adjustments are then journalized to correct the books.

Bank Side: Deposits in transit, outstanding checks, bank errors.

Book Side: Bank collections, EFTs, service charges, interest revenue, NSF checks, printed check costs, book errors.

Journalizing: Entries are made to record corrections and adjustments.

Receivables and Revenue

Revenue Recognition under GAAP

Revenue is recognized when it is earned, typically when goods are delivered or services performed. The amount recorded is the cash received or the fair market value of assets received.

Contract: Agreement between two parties creating enforceable rights.

Five Steps:

Identify the contract(s)

Identify performance obligations

Determine transaction price

Allocate transaction price

Recognize revenue when obligations are satisfied

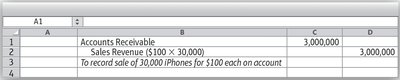

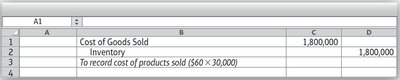

Example: Apple delivers 30,000 iPhones to AT&T for $100 each; revenue is recognized when delivered.

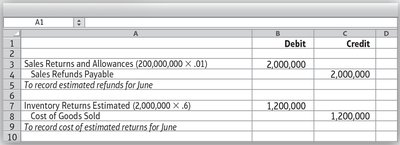

Sales Returns and Allowances

Sales returns and allowances account for customers' rights to return unsatisfactory goods. Companies estimate returns based on historical data and adjust inventory and revenue accordingly.

Credit Memo: Document authorizing a credit to the customer's account.

Example: Apple estimates 1% returns on $200 million sales; entries adjust sales and inventory.

Sales Discounts

Sales discounts incentivize early payment by offering a percentage off the sales price if paid within a specified period (e.g., 2/10, n/30).

2/10, n/30: 2% discount if paid within 10 days; otherwise, full payment due in 30 days.

Types of Receivables

Receivables are monetary claims against others, classified as current assets. They arise from selling goods/services (accounts receivable) or lending money (notes receivable).

Trade Receivables: Claims from sales transactions.

Notes Receivable: Claims from lending money.

Allowance for Uncollectible Accounts

Companies estimate uncollectible accounts to avoid overstating assets. The allowance method records losses based on past experience and creates a contra account to accounts receivable.

Uncollectible-Account Expense: Cost of accounts not expected to be collected.

Allowance for Uncollectible Accounts: Contra account showing expected uncollectibles.

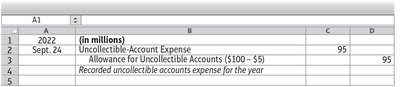

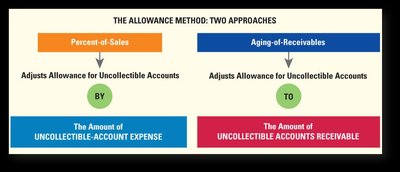

Estimating Uncollectibles: Percent-of-Sales and Aging-of-Receivables Methods

Two main methods are used to estimate uncollectibles:

Percent-of-Sales Method: Calculates expense as a percent of revenue (income statement approach).

Aging-of-Receivables Method: Analyzes accounts based on how long they are outstanding (balance sheet approach).

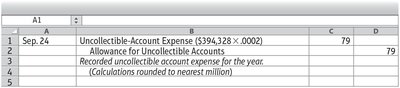

Example: Apple estimates uncollectibles as 0.0002 of $394,328 million revenue; entry updates allowance.

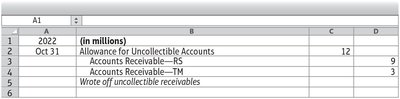

Writing Off Uncollectible Accounts

When specific accounts are determined to be uncollectible, they are written off against the allowance account.

Example: Apple writes off receivables from RS and TM.

Direct Write-Off Method

An alternative to the allowance method, the direct write-off method records expense only when a specific account is proven uncollectible. It is not GAAP-compliant and may overstate assets.

Drawback: Fails to match expense with revenue period.

Receivables Ratios

Key ratios help evaluate the efficiency of receivables management:

Quick (Acid-Test) Ratio: Measures liquidity using cash, short-term investments, and net receivables.

Accounts Receivable Turnover:

Days' Sales Outstanding (DSO):

Inventory and Cost of Goods Sold

Inventory Accounting

Inventory is an asset until sold, at which point its cost becomes an expense (cost of goods sold) on the income statement. Gross profit is sales revenue minus cost of goods sold.

Inventory on Hand: Asset on balance sheet.

Cost of Goods Sold: Expense on income statement.

Gross Profit:

Periodic vs. Perpetual Inventory Systems

Inventory systems track goods bought, sold, and on hand:

Perpetual System: Continuous record; used for all goods.

Periodic System: Record updated periodically; used for inexpensive goods.

Inventory Costing Methods

Companies can use several methods to assign costs to inventory and cost of goods sold:

Specific-Identification Method: Tracks individual items.

Average-Cost Method: Uses weighted average cost.

First-In, First-Out (FIFO) Method: First costs in are first costs out.

Last-In, First-Out (LIFO) Method: Last costs in are first costs out.

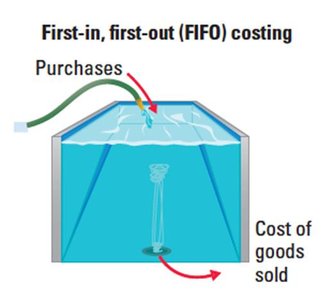

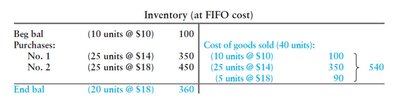

FIFO Method

FIFO assigns the earliest costs to cost of goods sold, leaving the most recent costs in ending inventory.

Example: Inventory and cost of goods sold calculated using FIFO.

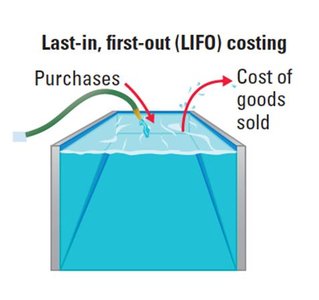

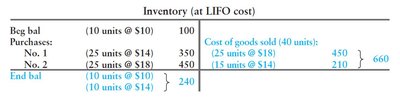

LIFO Method

LIFO assigns the most recent costs to cost of goods sold, leaving the oldest costs in ending inventory.

Example: Inventory and cost of goods sold calculated using LIFO.

Income Effects of Inventory Methods

Different inventory methods affect cost of goods sold, gross profit, and taxes. When costs are rising, LIFO results in higher cost of goods sold and lower taxable income, reducing taxes.

Method | Sales Revenue | Cost of Goods Sold | Gross Profit |

|---|---|---|---|

FIFO | $1,000 | $540 (lowest) | $460 (highest) |

LIFO | $1,000 | $660 (highest) | $340 (lowest) |

Average | $1,000 | $600 | $400 |

Tax Advantages: LIFO reduces taxable income and taxes when costs are rising.

Lower-of-Cost-or-Market (LCM) Rule

The LCM rule requires inventory to be reported at the lower of its historical cost or market value (net realizable value), ensuring relevance and representational faithfulness.

Inventory Turnover and Days Inventory Outstanding (DIO)

Inventory turnover measures how quickly inventory is sold. Days inventory outstanding (DIO) shows the average number of days inventory is held before sale.

Inventory Turnover:

Average Inventory:

DIO:

GAAP Principles for Inventory

GAAP requires disclosure, representational faithfulness, and consistency in inventory accounting. Companies must report enough information for outsiders to make informed decisions and use comparable methods from period to period.