Back

BackInternal Control, Revenue Recognition, Receivables, and Inventory: Exam 2 Review Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Internal Control and Cash

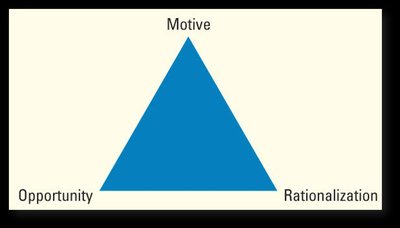

The Fraud Triangle

The Fraud Triangle explains the three elements necessary for fraud to occur in an organization: motive, opportunity, and rationalization. Understanding these elements helps organizations design controls to prevent fraud.

Motive: The need or pressure to commit fraud (e.g., financial difficulties).

Opportunity: The ability to commit fraud, often due to weak internal controls.

Rationalization: The mindset that justifies the fraudulent act.

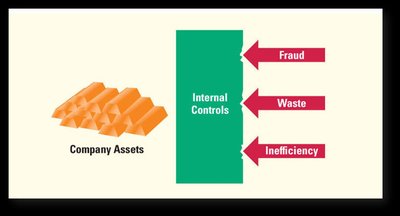

The Function of an Internal Control System

Internal controls are processes and procedures implemented to safeguard company assets, ensure accurate financial reporting, and promote operational efficiency. They act as barriers against fraud, waste, and inefficiency.

Fraud: Intentional misrepresentation for personal gain.

Waste: Inefficient use of resources.

Inefficiency: Failure to maximize productivity or minimize costs.

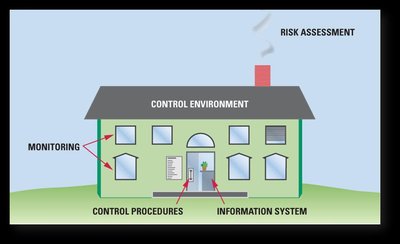

The Components of Internal Control

Internal control systems are structured around several key components, often illustrated as parts of a house:

Control Environment: The overall attitude, awareness, and actions of management regarding internal controls.

Risk Assessment: Identifying and analyzing risks that may prevent the achievement of objectives.

Control Procedures: Policies and procedures that help ensure management directives are carried out.

Information System: Methods and records established to record, process, summarize, and report transactions.

Monitoring: Ongoing evaluations to ensure controls are operating as intended.

Internal Control Procedures

Smart Hiring Practices: Background checks, training, supervision, competitive salaries, and clear responsibilities.

Separation of Duties: Different individuals handle asset custody, record keeping, and transaction approval to reduce risk of error or fraud.

Adequate Records: Maintain detailed, prenumbered documents (hard copy or electronic) for all transactions.

Information Technology: Use of electronic systems (e.g., bar codes, sensors) to improve accuracy and speed.

Cash Receipts by Mail

Proper segregation of duties is essential in handling cash receipts by mail. The process typically involves the mailroom, treasurer, accounting department, and controller, each with distinct responsibilities to prevent fraud and errors.

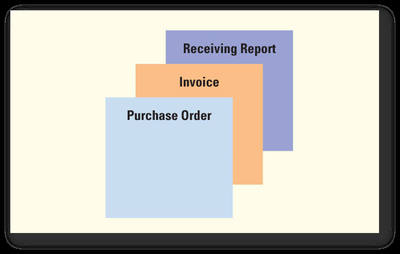

Controls Over Payment by Check

To safeguard cash, duties related to purchasing, receiving goods, preparing payments, and approving payments should be separated. The payment packet (purchase order, invoice, receiving report) is used to authorize payments.

Petty Cash

Petty cash funds are used for minor expenses. The imprest system ensures that the sum of cash on hand plus vouchers equals the established fund balance. Debit cards may also be used for small payments.

Limitations of Internal Control

Collusion: Two or more employees working together to circumvent controls.

Management Override: Executives bypassing controls for personal gain.

Human Limitations: Fatigue, negligence, or simple error.

Cost-Benefit Principle: The benefits of controls should outweigh their costs.

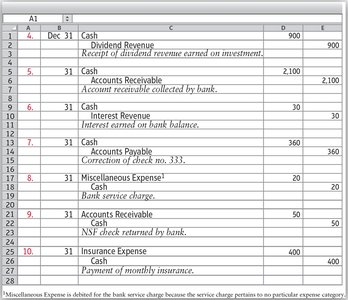

Bank Reconciliation

Bank reconciliation compares the company’s records (book side) with the bank statement (bank side) to identify discrepancies and ensure accuracy.

Bank Side Adjustments: Deposits in transit, outstanding checks, bank errors.

Book Side Adjustments: Bank collections, electronic funds transfers, service charges, interest revenue, NSF checks, cost of printed checks, book errors.

Journalizing Transactions from the Bank Reconciliation

Adjusting entries are made to record items identified during the bank reconciliation process, such as interest earned, service charges, and NSF checks.

Reporting Cash on the Balance Sheet

Cash equivalents are highly liquid investments with maturities of three months or less and are reported with cash on the balance sheet.

Revenue Recognition and Receivables

GAAP Revenue Recognition Principles

Revenue is recognized when earned, typically when goods are delivered or services performed, and is measured at the amount of cash or fair value of assets received. A contract (written or oral) creates enforceable rights and obligations.

Five Steps for Revenue Recognition:

Identify the contract(s)

Identify the performance obligation(s)

Determine the transaction price

Allocate the transaction price to the performance obligations

Recognize revenue when the entity satisfies the obligations

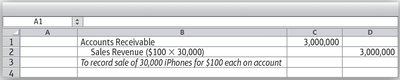

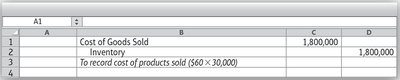

Example: Sale of Goods on Account

When Apple delivers 30,000 iPhones at $100 each (cost $60 each) to a customer on account, the following entries are made:

Shipping Terms

FOB Shipping Point: Ownership transfers and revenue is recognized when goods leave the seller's dock.

FOB Destination: Ownership transfers and revenue is recognized upon delivery to the customer.

Speeding Up Cash Flow from Sales

Offer sales discounts for early payment (e.g., 2/10, n/30).

Charge interest on overdue accounts.

Emphasize credit card or bankcard sales.

Improve credit and collection procedures.

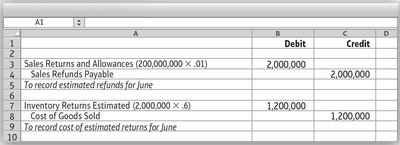

Sales Returns, Allowances, and Discounts

Customers may return goods or receive allowances for unsatisfactory items. Sales discounts incentivize early payment. These are recorded as reductions to sales revenue.

Credit Memo: Document authorizing a credit to the customer’s account.

Types of Receivables

Accounts Receivable: Amounts due from customers for sales on credit.

Notes Receivable: Written promises to pay a certain amount in the future.

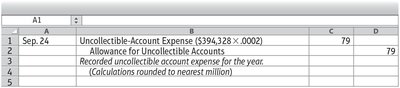

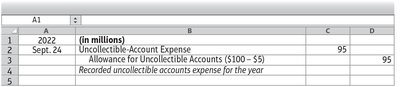

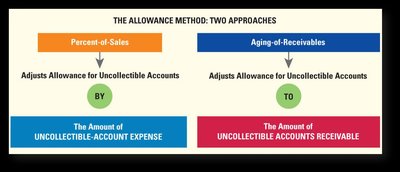

Allowance for Uncollectible Accounts

Companies estimate and record uncollectible accounts expense to match bad debts with related revenue. The Allowance for Uncollectible Accounts is a contra-asset account that reduces accounts receivable to the amount expected to be collected.

Percent-of-Sales Method: Estimates uncollectibles as a percentage of sales (income statement approach).

Aging-of-Receivables Method: Estimates uncollectibles based on the age of each account (balance sheet approach).

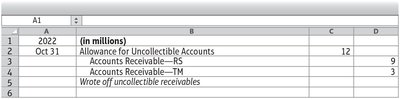

Writing Off Uncollectible Accounts

When specific accounts are deemed uncollectible, they are written off against the allowance account.

Comparison of Allowance Methods

Direct Write-Off Method

This method records bad debt expense only when a specific account is determined to be uncollectible. It is not GAAP-compliant because it may overstate assets and does not match expenses with revenues.

Receivables Ratios

Quick (Acid-Test) Ratio: Measures liquidity using cash, short-term investments, and net receivables.

Accounts Receivable Turnover:

Days' Sales Outstanding (DSO):

Inventory and Cost of Goods Sold

Inventory Accounting

Inventory is recorded as an asset until sold, at which point its cost is transferred to Cost of Goods Sold (COGS) on the income statement. Gross profit is sales revenue minus COGS.

Inventory Systems

Perpetual System: Continuously updates inventory records for each purchase and sale.

Periodic System: Updates inventory records at the end of the period based on a physical count.

Inventory Costing Methods

Specific Identification: Tracks the actual cost of each item sold.

Average-Cost: Uses the weighted average cost of all units available for sale.

FIFO (First-In, First-Out): Assumes earliest goods purchased are the first sold.

LIFO (Last-In, First-Out): Assumes latest goods purchased are the first sold.

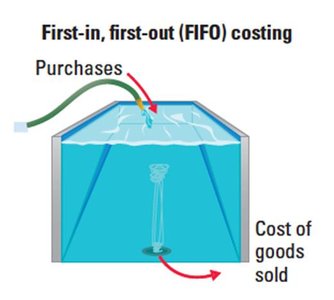

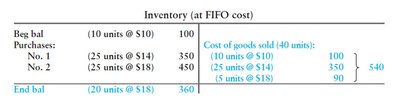

FIFO Method

Under FIFO, the first costs into inventory are the first assigned to COGS. Ending inventory consists of the most recent purchases.

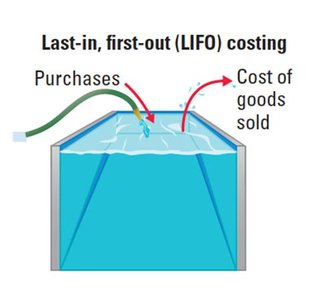

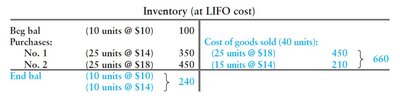

LIFO Method

Under LIFO, the last costs into inventory are the first assigned to COGS. Ending inventory consists of the oldest costs.

Income Effects of Inventory Methods

When prices are rising, FIFO results in lower COGS and higher gross profit, while LIFO results in higher COGS and lower gross profit. The reverse is true when prices are falling.

Tax Advantages of LIFO: In periods of rising prices, LIFO yields lower taxable income and lower taxes.

Balance Sheet Effects: FIFO provides a more up-to-date inventory value.

LIFO Liquidation

LIFO liquidation occurs when inventory levels fall below previous periods, causing older, lower costs to be included in COGS, which can artificially inflate profits.

GAAP Requirements for Inventory

Disclosure: Financial statements must provide enough information for users to make informed decisions.

Representational Faithfulness: Inventory methods and material transactions must be properly disclosed.

Consistency: Companies should use comparable methods from period to period.

Lower-of-Cost-or-Market (LCM) Rule

Inventory must be reported at the lower of its historical cost or market value (usually net realizable value), ensuring assets are not overstated.

Inventory Turnover and Days Inventory Outstanding (DIO)

Inventory Turnover:

Days Inventory Outstanding (DIO):

These ratios indicate how efficiently inventory is managed and how quickly it is sold.