Back

BackInternational Corporate Finance and Working Capital Management: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

International Corporate Finance

Foreign Exchange Basics

Foreign exchange rates are the prices at which one currency can be exchanged for another. These rates are quoted either directly or indirectly, depending on the perspective of the local currency.

Direct Quotation: The amount of local currency needed to buy one unit of foreign currency.

Indirect Quotation: The amount of foreign currency that can be purchased with one unit of local currency.

Conversion Formula:

Exchange Rate Fluctuations and the FX Market

Exchange rates fluctuate constantly due to supply and demand in the foreign exchange (FX) market, which operates globally and continuously.

Drivers of Supply and Demand:

Trade of goods and services

Investment in securities

Central bank actions

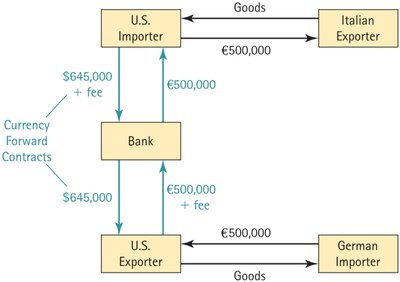

Exchange Rate Risk and Hedging

Firms engaged in international transactions face exchange rate risk, which can be mitigated using currency forward contracts. These contracts lock in an exchange rate for a future transaction, reducing uncertainty.

Currency Forward Contract: Specifies the exchange rate, amount, and delivery date.

Hedging: Reduces risk but does not guarantee a better outcome; it provides certainty.

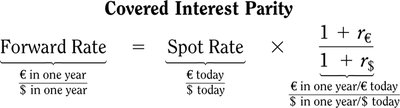

Forward Exchange Rate and Covered Interest Parity

The forward exchange rate is used in currency forward contracts for future exchanges. When forward rates are not available, the covered interest parity equation estimates implied forward rates based on interest rate differentials.

Covered Interest Parity Equation: Where and are the risk-free rates in the respective currencies.

Internationally Integrated Capital Markets

In integrated capital markets, investors can freely exchange currencies and securities, making the value of an investment independent of the currency used in analysis.

Implication: Valuation methods yield equivalent results regardless of currency.

Valuation of Foreign Projects

There are two methods to calculate the net present value (NPV) of a foreign project:

Convert foreign cash flows to home currency using forward rates, then discount at the domestic rate.

Discount foreign cash flows at the foreign rate, then convert the NPV to home currency at the spot rate.

Example: Axelrod, Inc.

Axelrod, Inc. evaluates a UK project with the following incremental earnings forecast:

Method 1: Free Cash Flow Conversion

Convert pound free cash flows to dollars using forward exchange rates.

Discount dollar cash flows at the domestic rate to obtain NPV.

Method 2: NPV Conversion

Discount pound cash flows at the pound discount rate.

Convert the resulting NPV to dollars at the spot rate.

Both methods yield the same NPV in integrated markets.

Working Capital Management

Overview of Working Capital

Working capital is essential for a firm's day-to-day operations and includes cash, inventory, accounts receivable, and accounts payable.

Net Working Capital:

Current Assets: Cash, inventory, accounts receivable

Current Liabilities: Accounts payable, bills

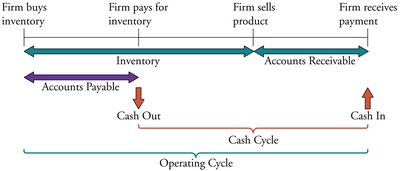

Cash and Operating Cycle

The cash cycle tracks the flow of cash through inventory purchases, sales, and collections. The operating cycle includes both the cash cycle and the time inventory is held.

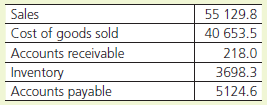

Cash Conversion Cycle (CCC)

The CCC measures the time between cash outflows for inventory and cash inflows from sales.

Formula:

Inventory Days:

Accounts Receivable Days:

Accounts Payable Days:

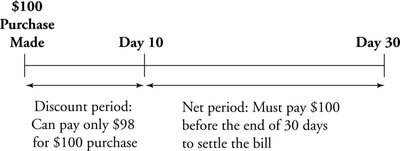

Trade Credit

Trade credit is the credit extended by firms to their customers, often with terms that offer discounts for early payment.

Example Terms: 2/10, net 30 means a 2% discount if paid within 10 days, otherwise full payment within 30 days.

Cost of Trade Credit and Effective Annual Rate (EAR)

The cost of forgoing trade credit discounts can be calculated as an effective annual rate (EAR), which is often much higher than bank loan rates.

Formula: Where is the discount rate and is the number of periods per year.

Application: If the EAR is high, buyers should take the discount and borrow from a bank if needed.

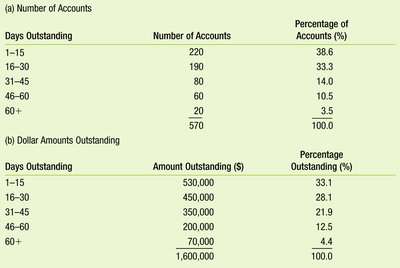

Receivables Management

Managing accounts receivable involves monitoring collection periods and analyzing aging schedules to assess credit risk.

Aging Schedule: Categorizes accounts by days outstanding and dollar amounts.

Payables Management

Firms should manage accounts payable efficiently, taking advantage of trade credit discounts when possible and avoiding unnecessary early payments.

Decision Rule: Pay within the discount window to maximize benefits; stretching payments can be a cheap source of funding but risks supplier relationships.

Inventory Management

Maintaining optimal inventory levels prevents stock-outs but excessive inventory increases costs. Just-in-Time (JIT) inventory management minimizes inventory holding.

Costs: Acquisition, order, and carrying costs

JIT: Inventory acquired as needed, minimizing balances

Cash Management

Firms hold cash for operational needs, precautionary purposes, and to meet bank requirements. Excess cash can be invested in short-term securities.

Alternative Investments: Short-term government debt, bank-accepted bills

Summary

Foreign exchange and hedging are crucial for international corporate finance.

Integrated capital markets allow equivalent valuation methods for foreign projects.

Working capital management maximizes firm value by optimizing cash cycles, trade credit, receivables, payables, inventory, and cash balances.