Back

BackIntroduction to Accounting: Role, Types, Stakeholders, and Career Paths

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Role of Accounting in Society

Importance of Accounting

Accounting is the process of organizing, analyzing, and communicating financial information for decision-making. It is often referred to as the "language of business" because it enables organizations to communicate their financial performance and position to various stakeholders. Understanding accounting is essential for nearly all business-related careers.

Definition: Accounting involves recording, classifying, and summarizing financial transactions.

Purpose: To provide accurate, timely information to decision makers.

Scope: Used in businesses, governmental entities, and not-for-profit organizations.

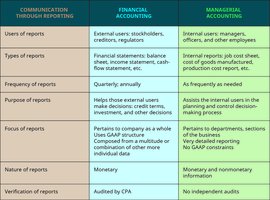

Distinguishing Financial and Managerial Accounting

Accounting is divided into two main branches: financial accounting and managerial accounting. Each serves different purposes and users.

Financial Accounting: Measures financial performance using standardized reports for external users such as investors, creditors, and regulators.

Managerial Accounting: Provides both financial and nonfinancial information for internal users, such as managers, to assist in decision-making, budgeting, and planning.

Example: Financial accounting reports include the balance sheet and income statement, while managerial accounting reports may include job cost sheets and production cost reports.

Users of Accounting Information

Internal and External Users

Accounting information is used by both internal and external users, each applying the information differently.

Internal Users: Managers and employees use accounting data for day-to-day and strategic decisions.

External Users: Investors, analysts, loan officers, and government auditors use financial statements to evaluate performance and make investment or lending decisions.

Characteristics of Financial Accounting Information

Financial accounting information is communicated through financial statements and is primarily historical in nature. It is prepared according to generally accepted accounting principles (GAAP), set by the Financial Accounting Standards Board (FASB).

Key Financial Statements: Income Statement, Statement of Owner’s Equity, Balance Sheet, Statement of Cash Flows.

Transaction: Any business activity with an associated cost or value.

Accounting Systems: Examples include QuickBooks (for small organizations) and SAP (for large/multinational organizations).

Characteristics of Managerial Accounting Information

Managerial accounting is not governed by standardized conventions and is tailored to internal needs. It often includes strategic and competitive information, which is closely protected.

Flexibility: Managerial accountants must adapt to the information needs of management.

Types of Information: Both financial and nonfinancial data are used.

Typical Accounting Activities and Organizational Types

Categories of Organizations

Organizations can be classified as for-profit, governmental, or not-for-profit entities. For-profit businesses are further divided into manufacturing, retail, and service types.

Manufacturing: Produces goods from raw materials.

Retail: Sells goods produced by others.

Service: Provides intangible benefits rather than tangible products.

Example: An auto manufacturing plant (manufacturing), a car sales lot (retail), and a taxi service (service) illustrate the three business types.

Accounting and Business Stakeholders

Stakeholders and Their Interests

Stakeholders are individuals or groups who rely on financial information to make decisions. They include stockholders, creditors, governmental agencies, customers, managers, and employees.

Stockholders: Owners interested in company success and stock value.

Creditors/Lenders: Assess risk and repayment ability.

Governmental Agencies: Require financial reports for regulatory purposes.

Customers: May be businesses (B2B) or end-users.

Managers/Employees: Use financial information for job security and organizational decisions.

Ways Organizations Raise Funding

Profitable Operations: Income from business activities.

Borrowing: Debt funding from banks or lenders.

Issuing Stock: Equity funding by selling ownership shares.

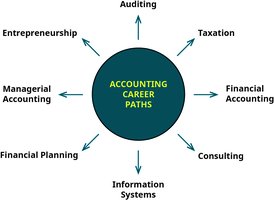

Career Paths in Accounting

Characteristics and Education of Accounting Professionals

Accounting professionals possess personal attributes such as goal orientation, analytical skills, and attention to detail. Entry-level positions typically require a bachelor’s degree, while advanced roles may require certifications or graduate degrees.

Related Careers: Financial analyst, personal financial planner, business executive.

Major Categories of Accounting Functions

Auditing

Taxation

Financial accounting

Consulting

Accounting information services

Cost and managerial accounting

Financial planning

Entrepreneurship

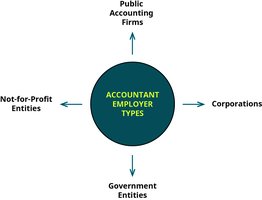

Accountant Employer Types

Public accounting firms

Corporations

Government entities

Not-for-profit entities

Potential Certifications for Accountants

Certified Public Accountant (CPA)

Certified Management Accountant (CMA)

Certified Internal Auditor (CIA)

Certified Fraud Examiner (CFE)

Chartered Financial Analyst (CFA)

Certified Financial Planner (CFP)

Summary

Accounting is essential for organizing, analyzing, and communicating financial information.

Financial accounting is for external users; managerial accounting is for internal users.

Organizations are classified as for-profit, governmental, or not-for-profit.

Stakeholders rely on accounting information for decision-making.

Career paths in accounting are diverse, with opportunities in various sectors and certifications available for advancement.