Back

BackIntroduction to Financial Accounting: Key Concepts and Financial Statements

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Introduction to Accounting

The Role of Accounting

Accounting is often referred to as the "language of business" because it provides essential information about a company's financial activities to various stakeholders. This information is communicated through financial statements, which are standardized reports that summarize a company's financial position and performance.

Users of Accounting Information: Managers, investors, creditors, government agencies, taxing authorities, and non-profit organizations all rely on accounting data for decision-making.

Business Organization Forms: Proprietorships (one owner), partnerships (two or more owners), and corporations (owned by shareholders).

The Financial Statements

Overview of Financial Statements

Financial statements are formal records that present the financial activities and position of a business. Each statement covers a specific period or date and serves a unique purpose.

Income Statement: Reports profitability over a period (revenues minus expenses = net income).

Statement of Retained Earnings: Shows changes in retained earnings over time.

Statement of Changes in Equity (IFRS): Details changes in common shares and retained earnings for public corporations.

Balance Sheet (Statement of Financial Position): Presents assets, liabilities, and shareholders’ equity at a specific date.

Statement of Cash Flows: Summarizes cash inflows and outflows from operating, investing, and financing activities.

Accounting Standards

GAAP (Generally Accepted Accounting Principles): The rules and guidelines for financial reporting.

IFRS (International Financial Reporting Standards): Used by publicly accountable enterprises.

ASPE (Accounting Standards for Private Enterprises): Used by private companies.

Elements of Financial Statements

The Income Statement

The income statement measures a company's profitability over a period. Under ASPE, it is calculated as:

Net Income = Revenues - Expenses

Under IFRS (from 2027), income and expenses must be classified into five categories: operating, investing, financing, income taxes, and discontinued operations.

Statement of Retained Earnings / Changes in Equity

Retained Earnings: The portion of net income kept in the business over time.

Statement of Changes in Equity (IFRS): Shows changes in common shares and retained earnings.

The Balance Sheet

The balance sheet reports a company's financial position at a specific date. It is structured as follows:

Assets: Economic resources expected to provide future benefits (e.g., cash, receivables, inventory, land).

Liabilities: Debts or obligations owed to outsiders (e.g., accounts payable, notes payable).

Shareholders’ Equity: Owners’ claims on the assets, including common shares and retained earnings.

The Statement of Cash Flows

This statement categorizes cash movements into:

Operating Activities: Cash from core business operations.

Investing Activities: Cash used for or provided by investments in assets.

Financing Activities: Cash from issuing shares, borrowing, or paying dividends.

The Accounting Equation

Basic Equation

The foundation of accounting is the accounting equation:

Assets: Resources owned by the business.

Liabilities: Claims by creditors.

Shareholders’ Equity: Owners’ claims (common shares + retained earnings).

Net Income and Retained Earnings

Net income increases retained earnings, while dividends and expenses decrease it:

Analyzing Financial Statements

Key Questions

Can the company sell its products/services?

Is the company profitable?

What percentage of sales revenue is profit?

Can the company collect receivables?

Can the company pay its liabilities?

Where is cash coming from and how is it used?

Common ratios include:

Profit Margin:

Current Ratio:

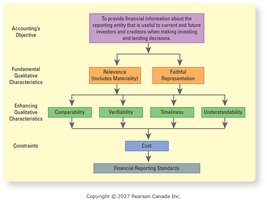

Conceptual Framework and Accounting Assumptions

Conceptual Framework

The conceptual framework guides the preparation and presentation of financial statements. It emphasizes relevance, faithful representation, and enhancing qualitative characteristics such as comparability, verifiability, timeliness, and understandability.

Key Accounting Assumptions

Separate Entity Assumption: The business is a distinct entity from its owners.

Going-Concern Assumption: The business will continue operating in the foreseeable future.

Historical Cost Assumption: Assets are recorded at their original cost.

Stable Monetary Unit Assumption: The currency's value is stable over time.

Ethics and Decision-Making in Accounting

Ethical Considerations

Business decisions are influenced by economic, legal, and ethical factors. Accountants must evaluate the ethical implications of their actions and ensure compliance with laws and professional standards.

Auditor’s Role: To provide an independent opinion on the fairness of financial statements relative to GAAP.

Accounting and ESG (Environmental, Social, Governance)

Role of Accounting in ESG

ESG reporting helps organizations identify opportunities, mitigate risks, and protect their reputation and profitability. Accounting tracks and reports on environmental, social, and governance measures.

Environmental: Energy use, emissions, waste.

Social: Employee turnover, volunteerism, workplace safety.

Governance: Board diversity, anti-corruption training, privacy training.

Careers and Tools in Accounting

Career Paths

External auditor

Management accountant

Internal auditor

Budget analyst

Financial analyst

Tools and Technologies

Spreadsheets (e.g., Excel)

Data analytics

Artificial intelligence (AI)

Machine learning

Robotic process automation (RPA)

Proper use of technology is essential to avoid errors and ensure data integrity.

Introduction to Excel

Excel is a fundamental tool in accounting for organizing, analyzing, and presenting financial data. Key components of a blank worksheet include the quick access toolbar, ribbon tabs, formula bar, worksheet tabs, and more.

Practice Problem: Preparing a Balance Sheet

Example: Alexa Markowitz, Realtor

Given a set of transactions and balances, students are asked to prepare a balance sheet and determine which items are relevant. Only business-related assets, liabilities, and equity are included; personal items are excluded due to the separate entity assumption.

Relevant Items: Business bank account, office supplies, franchise, land, business furniture, business liabilities.

Irrelevant Items: Personal bank account, personal mortgage, personal charge account (not related to the business).

Example Balance Sheet Structure:

Assets | Liabilities | Shareholders' Equity |

|---|---|---|

Business bank account | Note payable (land) | Common shares |

Office supplies | Accounts payable (furniture) | |

Franchise | ||

Land | ||

Furniture |

Additional info: Only business transactions are included in the balance sheet due to the separate entity assumption.