Back

BackInvesting Activities and Financial Asset Classification: Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Financial Assets and Investment Activities

Introduction to Financial Assets

Financial assets are resources based on contractual agreements that relate to future cash flows. They are a key component of the balance sheet and are classified based on the investor’s intention and the nature of the investment. The main categories include non-strategic and strategic investments.

Non-Strategic Investments

Classification of Non-Strategic Investments

Non-strategic investments are typically made without the intention of exerting significant influence or control over the investee. The classification of these investments depends on the investor’s intent and the characteristics of the financial instrument.

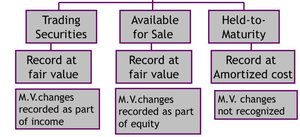

Trading Securities: Debt or equity securities held for short-term resale. Reported at fair value, with gains and losses recognized in the income statement.

Available-for-Sale Securities: Securities held for an indefinite period, reported at fair value. Unrealized gains and losses are included in other comprehensive income and accumulated in equity.

Held-to-Maturity Securities: Debt securities intended to be held until maturity. Reported at amortized cost, with unrealized gains and losses not recognized.

Accounting for Non-Strategic Investments

Trading Securities: Changes in market value (realized and unrealized) are recognized in the income statement.

Available-for-Sale Securities: Unrealized gains and losses are reported in other comprehensive income, not in the income statement until realized.

Held-to-Maturity Securities: Only realized gains and losses are recognized in the income statement; market value changes are ignored.

Dividend Treatment

Dividends received from investments are always reported in the income statement, regardless of the classification of the security.

Example: Trading Securities

Suppose Trading Co. buys 12,000 shares of Walmart at $10 each, receives $0.20 per share in dividends, and the shares are valued at $19 at year-end. The investment is classified as a trading security and reported at fair value ($228,000) under current assets. The income statement reflects both the realized dividend income and the unrealized gain:

Initial value: $120,000

Ending value: $228,000

Dividend income: $2,400

Total income increase:

Income Statement vs. Statement of Comprehensive Income

IAS 1 allows two presentation options:

Single Statement: Statement of Comprehensive Income, including all income and expenses.

Two Statements: Separate Income Statement and Statement of Comprehensive Income. The latter includes items not recognized in profit or loss, such as unrealized gains on available-for-sale securities.

Strategic Investments

Types of Strategic Investments

Strategic investments are made to exert significant influence or control over another entity. The main types include:

Subsidiary: More than 50% ownership; parent controls the subsidiary.

Joint Operations: Joint control of assets and obligations, but not a separate legal entity.

Joint Venture: Separate entity with joint control over net assets by two or more parties.

Associate: Significant influence, usually with 20-50% ownership.

Accounting for Strategic Investments

Consolidation (Subsidiaries): Parent and subsidiaries’ assets, liabilities, revenues, and expenses are aggregated. Intercompany transactions are eliminated. Minority interest represents the portion not owned by the parent.

Equity Method (Associates and Joint Ventures): Investment is initially recorded at cost, increased by the investor’s share of net income, and decreased by dividends received. The investor reports its share of the investee’s earnings as equity earnings in the income statement.

Example: Equity Method

Global Corp. acquires 25% of Synergy, Inc. for $500,000. If Synergy reports $100,000 net income and pays $20,000 in dividends, Global records:

Share of earnings: $25,000 (25% of $100,000)

Dividends received: $5,000 (25% of $20,000)

Journal entries:

Increase investment and recognize equity earnings: Investment $25,000 / Equity earnings $25,000

Decrease investment for dividends: Cash $5,000 / Investment $5,000

Other Assets

Examples of Other Assets

Property held for sale

Start-up costs

Cash surrender value of life insurance

Long-term advance payments

Intangible assets (excluding goodwill)

Summary Table: Financial Asset Classification

Classification | Measurement Basis | Recognition of Market Value Changes |

|---|---|---|

Trading Securities | Fair Value | Income Statement |

Available-for-Sale | Fair Value | Other Comprehensive Income |

Held-to-Maturity | Amortized Cost | Not Recognized |

Key Formulas

Fair Value of Investment:

Dividend Income:

Unrealized Gain/Loss:

Equity Method Share of Earnings:

Dividends Received (Equity Method):