Back

BackInvesting Activities: Physical Assets, Receivables, Inventory, and Depreciation

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

The Balance Sheet and Asset Classification

Introduction to the Balance Sheet

The balance sheet, also known as the statement of financial position, provides a snapshot of a company's financial condition at a specific point in time. It summarizes what the firm owns (assets) and what it owes to both external parties (liabilities) and internal owners (equity).

Assets: Resources owned by the company.

Liabilities: Obligations to outsiders.

Equity: Owners' residual interest in the assets after deducting liabilities.

Consolidation

When a parent company owns more than 50% of the voting stock of another company, their financial statements are combined in a process called consolidation.

Balance Sheet Format

There is no prescribed format for the balance sheet by the FASB, SEC, or IASB, but most firms use a classified balance sheet, grouping assets and liabilities by their nature and liquidity.

Asset Classification

Assets are typically classified as:

Current Assets: Expected to be converted to cash or used up within one year (e.g., cash, accounts receivable, inventory).

Long-Term Assets: Provide economic benefits beyond one year (e.g., property, plant, and equipment, intangible assets).

Another important classification is:

Physical Assets: Tangible items such as inventory and PP&E.

Financial Assets: Assets based on contractual rights to future cash flows (e.g., marketable securities).

Current Assets: Accounts Receivable (A/R) and Allowance for Doubtful Accounts

Nature and Importance of Accounts Receivable

Accounts Receivable (A/R) represent amounts owed by customers from credit sales. The net realizable value of A/R is the actual amount expected to be collected, after deducting an allowance for doubtful accounts.

Net Realizable Value = Accounts Receivable – Allowance for Doubtful Accounts

Allowance for Doubtful Accounts

The allowance for doubtful accounts is a contra-asset account that estimates the portion of receivables that may not be collected. This estimate is crucial for assessing the quality of earnings and the accuracy of the balance sheet.

Should reflect credit sales volume, past experience, customer base, credit policies, collection practices, and economic conditions.

Methods for Estimating Bad Debts

Direct Write-Off Method: Recognizes bad debts only when specific accounts are deemed uncollectible.

Allowance Method: Estimates uncollectible accounts at the end of each period, matching bad debt expense to the period's sales.

Bad Debt Ratio (Allowance Method):

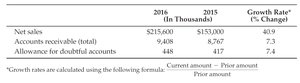

Analyzing Receivables and Earnings Quality

Analyzing the relationship between sales, accounts receivable, and the allowance for doubtful accounts helps assess the quality of earnings and the risk of default.

Consistent growth rates among these accounts indicate stable earnings quality.

Discrepancies may signal changes in credit policy, collection issues, or economic shifts.

Example: Receivables and Allowance Analysis

Growth rates are calculated as:

Current Assets: Inventory and Inventory Accounting Methods

Inventory Accounting Methods

Inventory can be valued using different cost flow assumptions, which affect both the income statement and the balance sheet:

FIFO (First-In, First-Out): Assumes earliest goods purchased are sold first.

LIFO (Last-In, First-Out): Assumes latest goods purchased are sold first.

Average Cost: Allocates cost based on the weighted average of all units available for sale.

The choice of method impacts reported profits, taxes, and asset values, especially during periods of inflation.

Inventory Methods: Example and Effects

FIFO: Lower cost of goods sold, higher ending inventory during inflation.

LIFO: Higher cost of goods sold, lower ending inventory during inflation (not allowed under IFRS).

Average Cost: Results fall between FIFO and LIFO.

LIFO Reserve

Companies using LIFO must disclose the amount by which inventory would differ if FIFO were used. This difference is called the LIFO reserve.

Fixed Assets: Property, Plant, and Equipment (PP&E) and Depreciation

Nature of PP&E

Property, Plant, and Equipment (PP&E) are long-term tangible assets used in operations and not intended for sale. They are recorded at book value and depreciated over their useful lives.

Examples: Land, buildings, machinery, equipment, leasehold improvements.

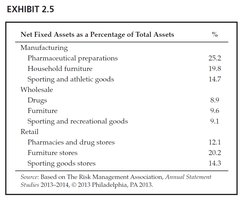

Relative Proportion of Fixed Assets

The proportion of fixed assets varies by industry and business model. Manufacturing firms typically have higher percentages of fixed assets compared to retailers or wholesalers.

Depreciation Methods

Depreciation allocates the cost of tangible fixed assets over their useful lives. Common methods include:

Straight-Line Method: Equal expense each year.

Accelerated Methods: Higher expense in earlier years.

Units-of-Production Method: Expense based on actual usage.

Straight-Line Depreciation Formula:

Units-of-Production Depreciation Formula:

Leasehold Improvements

Improvements made to leased property are amortized over the shorter of the economic life of the improvement or the lease term.

Other Assets

Other assets may include investment assets, property held for sale, start-up costs, cash surrender value of life insurance, long-term advance payments, and intangible assets (other than goodwill).

Additional info: The notes above integrate and expand upon the provided slides and images, ensuring a comprehensive, self-contained study guide for financial accounting students.