Back

BackLong-Lived Assets: Recognition, Depreciation, and Disposal

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Long-Lived Assets and Related Expense Accounts

Overview of Long-Lived Assets

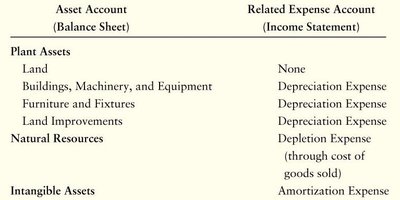

Long-lived assets, also known as non-current assets, are resources expected to provide economic benefits over multiple periods. These assets are classified into plant assets (Property, Plant, and Equipment), natural resources, and intangible assets. Each asset type has a corresponding expense account that reflects the allocation of its cost over time.

Plant Assets: Land, Buildings, Machinery, Equipment, Furniture, Fixtures, and Land Improvements.

Natural Resources: Assets like mineral deposits, oil fields, and timber tracts.

Intangible Assets: Non-physical assets such as patents, copyrights, and trademarks.

Property, Plant, and Equipment (PPE): Initial Recognition and Measurement

Determining the Cost of PPE

The cost of a PPE asset is the sum of all expenditures necessary to acquire the asset and prepare it for its intended use. This includes the purchase price and all directly attributable costs.

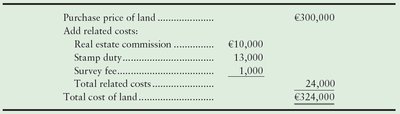

Land: Purchase price, brokerage commission, survey fees, legal fees, back property taxes, grading, clearing, and removal of unwanted buildings.

Land Improvements: Costs for driveways, signs, fences, sprinkler systems, and similar items.

Buildings (Construction): Architectural fees, building permits, contractor charges, materials, labor, overhead, and interest on construction financing.

Buildings (Purchase): Purchase price, brokerage commission, taxes, and renovation costs.

Equipment: Purchase price (net of discounts), transportation, insurance in transit, taxes, commissions, installation, testing, and special platforms.

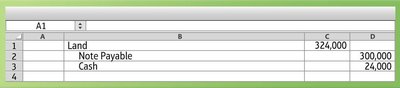

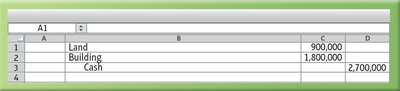

Example: Calculating the Cost of Land

When acquiring land, all related costs are added to the purchase price to determine the total cost recognized on the balance sheet.

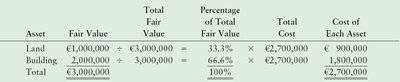

Lump-Sum (Basket) Purchases

When multiple assets are purchased together for a single price, the total cost is allocated to each asset based on their relative fair values. This is known as the relative-sales-value method.

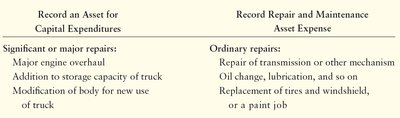

Capital Expenditures vs. Immediate Expenses

Capitalization of Subsequent Costs

Subsequent expenditures on PPE are either capitalized or expensed, depending on their nature:

Capital Expenditure: Increases asset capacity or extends useful life; added to the asset's cost.

Immediate Expense: Ordinary repairs and maintenance; expensed in the period incurred.

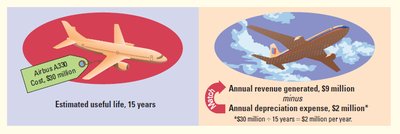

Depreciation of Plant Assets

Concept and Measurement of Depreciation

Depreciation is the systematic allocation of the cost of a tangible asset over its useful life. It matches the asset's cost with the revenue it helps generate. Land is not depreciated because it does not have a finite useful life.

Book Value: The carrying amount of an asset on the balance sheet, calculated as:

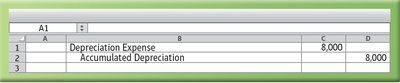

Depreciation Expense: Reported on the income statement.

Key Depreciation Concepts

Cost: All expenditures to acquire and prepare the asset for use.

Estimated Useful Life: The expected period of service.

Estimated Residual Value: Expected value at the end of useful life.

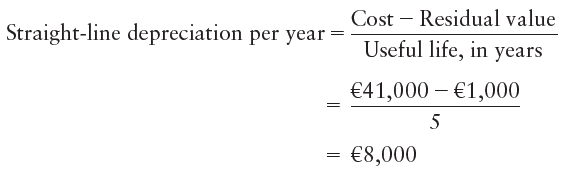

Depreciation Methods

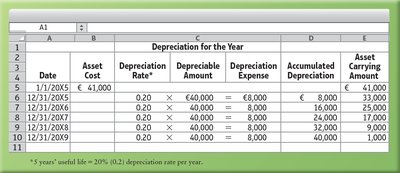

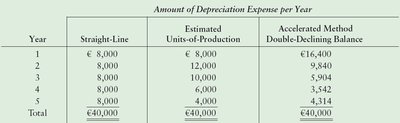

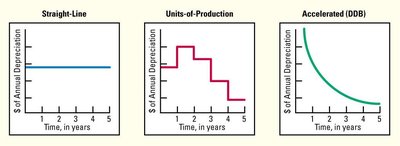

Straight-Line Method

This method allocates an equal amount of depreciation each year over the asset's useful life.

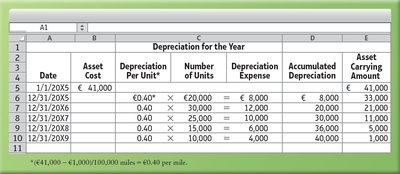

Units-of-Production Method

This method allocates depreciation based on actual usage or output.

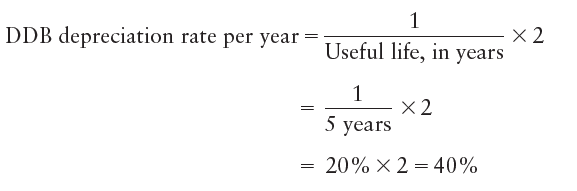

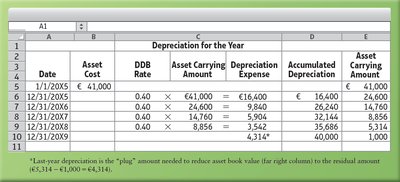

Double-Declining-Balance (DDB) Method

This accelerated method records higher depreciation in the early years of an asset's life. The depreciation rate is double the straight-line rate and is applied to the asset's book value at the start of each year.

Comparison of Depreciation Methods

The choice of depreciation method affects the pattern of expense recognition:

Straight-Line: Even expense over time; best for assets generating consistent revenue.

Units-of-Production: Expense varies with usage; best for assets whose wear depends on use.

Double-Declining-Balance: Higher expense in early years; best for assets generating more revenue early in life.

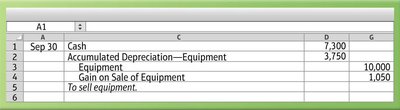

Disposal of Property, Plant, and Equipment (PPE)

Accounting for Disposals

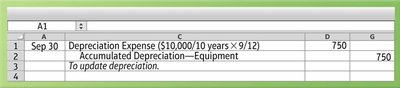

When disposing of PPE, depreciation must be updated to the date of disposal. The asset and its accumulated depreciation are removed from the books, and any gain or loss is recognized.

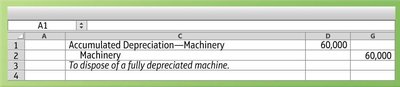

Fully Depreciated Asset: Remove both the asset and accumulated depreciation; no gain or loss if no proceeds are received.

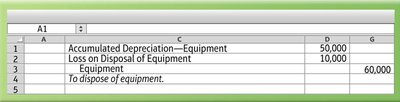

Not Fully Depreciated Asset: Remove asset and accumulated depreciation; recognize loss if book value exceeds proceeds.

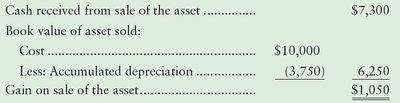

Sale of Asset: Compare proceeds to book value; recognize gain or loss.

Additional info: The notes above include expanded academic context and examples to ensure the material is self-contained and suitable for exam preparation.