Back

BackManaging Costs and Earned Value Analysis in Construction Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Managing Costs in Construction Accounting

Monitoring and Controlling Process

Effective cost management in construction projects requires a systematic approach to monitoring and controlling expenses. The process typically involves establishing a baseline, collecting and assessing data, and taking corrective action when necessary.

Establish a Baseline: Set initial budgets and schedules for all project components.

Collect Data: Gather information on actual costs incurred for materials, labor, subcontractors, equipment, and overhead.

Assess Data: Compare actual costs to budgeted amounts to identify variances.

Take Corrective Action: Implement changes to address cost overruns or inefficiencies.

Material Purchases

Material purchases are managed through purchase orders, which must be approved by the project manager. Supervisors may have limited authority for small purchases.

Purchase Orders: Ensure accountability and control over material expenses.

Approval Process: Project manager approval is required for significant purchases.

Labor Costs

Labor costs are challenging to control and are tracked using timecards, preferably electronic for efficiency. Timely processing is essential to maintain accurate records.

Timecards: Used to record hours worked and calculate labor costs.

Electronic Systems: Improve accuracy and speed of data collection.

Subcontractor Costs

Subcontractor payments often require progress payments and can be difficult to assess for percent completion.

Progress Payments: Payments made based on work completed.

Percent Complete: Estimation required for payment calculation.

Equipment Costs

Equipment costs are managed similarly to labor, using equipment time cards or information systems. Prompt return of equipment after use is crucial.

Equipment Time Cards: Track usage and costs.

Information Systems: Provide detailed tracking and reporting.

Other Costs and General Overhead

Other costs, such as utility bills, require project manager approval if not covered by purchase orders. General overhead must be managed as aggressively as direct construction costs.

Approval Process: Ensures oversight for miscellaneous expenses.

Overhead Management: Controls indirect costs impacting project profitability.

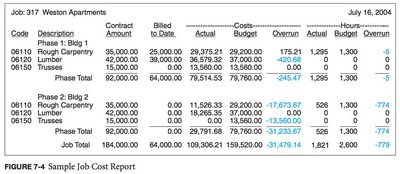

Job Profitability and Earned Value Analysis

Job Profitability

Job profitability is updated weekly, including cost to complete, estimated cost at completion, and estimated profit. Committed costs should be included even if not tracked in the accounting system.

Cost to Complete: Estimate of remaining expenses.

Estimated Cost at Completion: Total projected cost for the project.

Estimated Profit: Difference between contract amount and total costs.

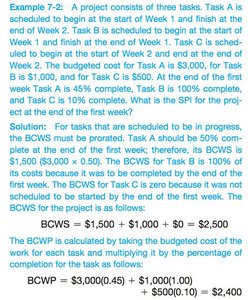

Earned Value Analysis

Earned value analysis is a method for measuring project performance with respect to schedule and cost. It uses two key indexes: the Schedule Performance Index (SPI) and the Cost Performance Index (CPI).

Schedule Performance Index (SPI): Measures progress relative to the schedule.

Cost Performance Index (CPI): Measures cost efficiency relative to the budget.

Required Values: Actual Cost of Work Performed (ACWP), Budgeted Cost of Work Scheduled (BCWS), Budgeted Cost of Work Performed (BCWP).

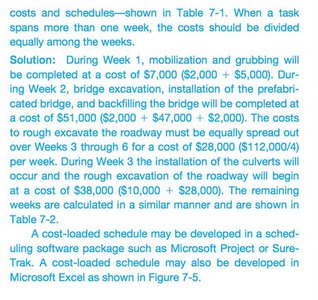

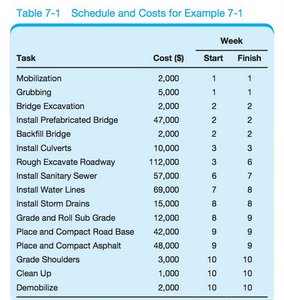

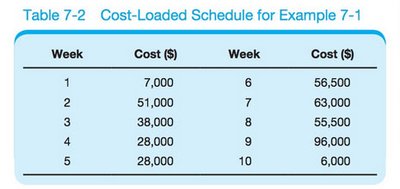

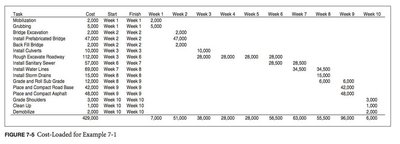

Cost-Loaded Schedule

A cost-loaded schedule assigns costs to tasks and determines weekly or monthly expenses. This helps in tracking and controlling project costs over time.

Task Assignment: Each task is assigned a cost and scheduled over specific weeks.

Cost Distribution: Costs are spread across the project timeline.

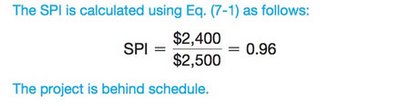

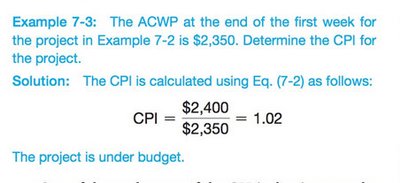

Calculation of SPI and CPI

The SPI and CPI are calculated using the following formulas:

SPI Formula:

CPI Formula:

Example calculations:

SPI Example: (Project is behind schedule)

CPI Example: (Project is under budget)

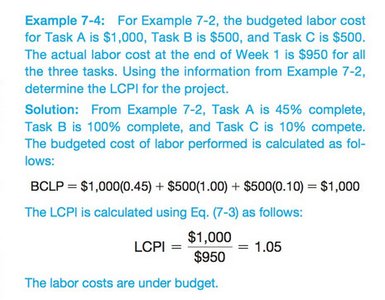

Labor Cost Performance Index (LCPI)

The LCPI measures control of in-house labor costs and is calculated similarly to CPI, but only considers labor expenses.

LCPI Formula:

BCLP: Budgeted Cost of Labor Performed

ACLP: Actual Cost of Labor Performed

Example calculation:

LCPI Example: (Labor costs are under budget)

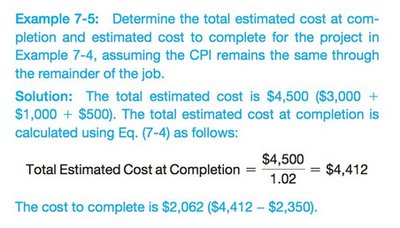

Total Estimated Cost at Completion

The total estimated cost at completion is calculated by dividing the total estimated cost by the CPI, assuming the CPI remains constant.

Formula:

Example:

Variance Analysis

Variance analysis compares budgeted costs to actual or estimated costs to identify areas of overrun or savings.

Variance:

Purpose: Helps management identify and address cost discrepancies.

Project Closeout Audit

Audit Process

At project completion, a closeout audit is performed to validate data, identify areas of success, and learn from mistakes. This process helps improve future project management and cost control.

Data Validation: Ensures accuracy of reported costs and performance.

Performance Review: Identifies best practices and areas for improvement.

Design-Build Projects

Budgeting and Monitoring

Design-build projects require budgeting, cost estimation, variance determination, and redesign as needed. Monitoring and controlling design costs (such as architect and engineer fees) use similar methods as construction cost control.

Design to Budget: Establish and adhere to a budget throughout the design phase.

Cost Estimates: Prepare detailed estimates and monitor variances.

Redesign: Adjust plans to stay within budget.

Conclusion

Managing construction costs requires robust cost control procedures, early approval against budgets, and the use of accounting reports and earned value analysis. SPI and CPI are essential for measuring scheduling and cost efficiency. Project closeout audits provide valuable lessons for future projects.