Back

BackMeasuring and Reporting Financial Position: Study Notes for Financial Accounting Students

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Measuring and Reporting Financial Position

The Major Financial Statements

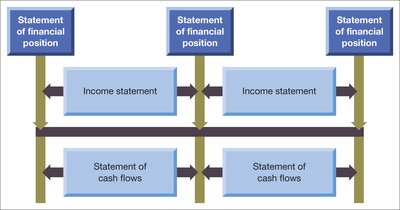

The three principal financial statements in financial accounting are the statement of financial position (balance sheet), income statement (profit and loss account), and statement of cash flows. Each provides a distinct perspective on a business's financial health.

Statement of Financial Position: Shows the assets of a business and the claims on those assets at a specific point in time.

Income Statement: Measures and reports the profit (or loss) generated during a period by comparing revenues and expenses.

Statement of Cash Flows: Details the sources and uses of cash over a period.

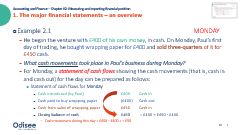

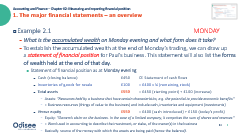

Example: Business Transactions and Financial Statements

Consider a simple business scenario where an individual starts a venture selling gift wrapping paper. The following illustrates how each financial statement is prepared and interpreted:

Statement of Cash Flows: Tracks cash introduced, cash spent on inventory, and cash received from sales.

Income Statement: Calculates profit as the difference between sales revenue and the cost of goods sold.

Statement of Financial Position: Summarizes the accumulated wealth, showing cash and unsold inventory as assets, and equity as the owner's claim.

The Statement of Financial Position

Definition and Purpose

The statement of financial position (balance sheet) is a snapshot of a business's assets and the claims against those assets (equity and liabilities) at a specific point in time. It answers the question: "What is the accumulated wealth at the end of a period, and in what form is it held?"

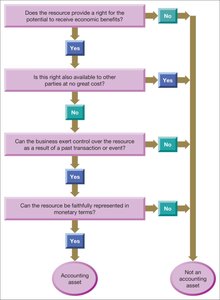

Assets: Economic resources controlled by the business, capable of providing future economic benefits.

Claims: Sources of funding for assets, divided into equity (owner's claim) and liabilities (claims of outsiders).

Characteristics of Assets

For an item to be recognized as an asset in the statement of financial position, it must meet several criteria:

Provide potential economic benefits.

Be under the control of the business.

Result from a past transaction or event.

Be capable of measurement in monetary terms.

Types of Claims: Equity and Liabilities

Claims on assets are classified as:

Equity: Owner's claim, including initial capital and accumulated profits.

Liabilities: Outsiders' claims, arising from past transactions and requiring future settlement.

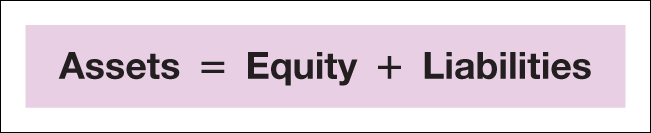

The Accounting Equation

The statement of financial position is governed by the fundamental accounting equation:

Extended Accounting Equation

The equation can be extended to reflect changes over a period:

Classifying Assets and Claims

Current vs Non-Current Assets

Assets are classified based on their intended use and liquidity:

Current Assets: Held for sale or consumption within the business's operating cycle, expected to be sold within a year, or are cash/near cash.

Non-Current Assets: Held for long-term use, including tangible (property, plant, equipment) and intangible (patents, copyrights) assets.

Current vs Non-Current Liabilities

Liabilities are classified by their settlement period:

Current Liabilities: Due for settlement within the operating cycle or within a year.

Non-Current Liabilities: Due for settlement beyond one year.

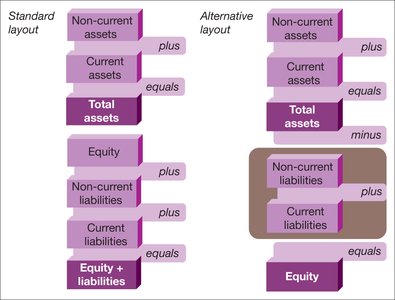

Statement Layouts

Standard and Alternative Layouts

Statements of financial position can be presented in different layouts:

Standard Layout: Lists assets at the top, followed by equity and liabilities.

Alternative Layout: Deducts liabilities from assets to show net assets, with equity below.

Standard Layout | Alternative Layout |

|---|---|

Assets Equity Liabilities | Assets Liabilities Net Assets Equity |

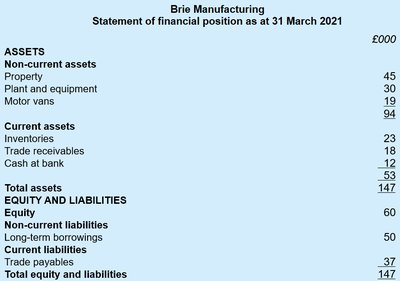

Example: Statement of Financial Position

ASSETS | CLAIMS = EQUITY AND LIABILITIES |

|---|---|

Non-current assets Property: £45,000 Plant and equipment: £30,000 Motor vans: £19,000 Current assets Inventories: £23,000 Trade receivables: £18,000 Cash at bank: £12,000 Total assets: £147,000 | Equity: £60,000 Non-current liabilities Long-term borrowings: £50,000 Current liabilities Trade payables: £37,000 Total equity and liabilities: £147,000 |

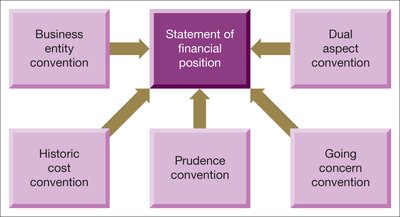

Accounting Conventions

Key Conventions Influencing the Statement of Financial Position

Accounting conventions are rules developed to address practical issues in preparing financial statements:

Business Entity Convention: Business and owner are treated as separate entities.

Historic Cost Convention: Assets are recorded at their acquisition cost.

Prudence Convention: Caution is exercised to avoid overstating financial strength.

Going Concern Convention: Assumes the business will continue operations for the foreseeable future.

Dual Aspect Convention: Every transaction affects two aspects of the statement (double-entry bookkeeping).

Money Measurement and Asset Valuation

Money Measurement

Only resources that can be measured reliably in monetary terms are recognized as assets. Some resources, such as goodwill or human resources, are excluded due to measurement difficulties.

Valuing Assets: Historic Cost vs Fair Value

Historic Cost: Assets are initially recorded at their purchase price.

Fair Value: International standards allow assets to be valued at current market value if reliably measurable.

Amortisation/Depreciation: Non-current assets with finite lives are depreciated over time to reflect usage.

Impairment: Assets are written down if their recoverable amount falls below carrying value.

Usefulness and Limitations of the Statement of Financial Position

The statement of financial position provides insights into how a business is financed and how its funds are deployed. It is useful for assessing business value, financial risk, and effectiveness, but it has limitations due to measurement conventions and the exclusion of certain resources.

Summary Table: Asset and Liability Classification

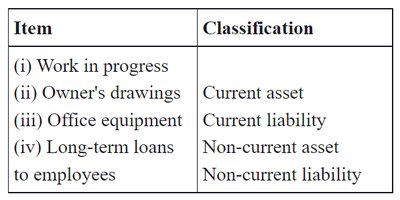

Item | Classification |

|---|---|

Work in progress | Current asset |

Owner's drawings | Current liability |

Office equipment | Non-current asset |

Long-term loans to employees | Non-current liability |

Quiz and Review Questions

Test your understanding with questions on asset classification, accounting conventions, and statement layouts. These help reinforce key concepts and ensure mastery of the material.

Key Formulas

Conclusion

Understanding the statement of financial position is fundamental for financial accounting students. It provides a comprehensive view of a business's financial health, the nature of its assets and claims, and the conventions that guide its preparation.