Back

BackMerchandising Operations: Financial Accounting Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Merchandising Operations

Introduction to Merchandising Operations

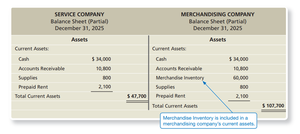

Merchandising operations involve businesses that purchase goods (merchandise) for resale to customers. These businesses differ from service companies in that they earn revenue by selling tangible products rather than providing services. Merchandising companies can be classified as either wholesalers (who sell to retailers) or retailers (who sell directly to consumers).

Merchandise Inventory: Goods held for resale to customers.

Wholesaler: Buys goods from manufacturers and sells to retailers.

Retailer: Buys goods from manufacturers or wholesalers and sells to consumers.

The Operating Cycle of a Merchandising Business

The operating cycle for a merchandising business begins with the purchase of inventory, followed by the sale of inventory to customers, and concludes with the collection of cash from those customers. This cycle is crucial for understanding cash flow and inventory management in merchandising operations.

Step 1: Purchase inventory from suppliers.

Step 2: Sell inventory to customers (often on account).

Step 3: Collect cash from customers.

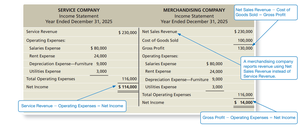

Financial Statements of Merchandising Companies

Merchandising companies report Sales Revenue instead of Service Revenue. The cost of merchandise sold is reported as Cost of Goods Sold (COGS). The difference between Net Sales Revenue and COGS is Gross Profit. Operating expenses are then deducted to arrive at Net Income.

Net Sales Revenue = Sales Revenue - Sales Returns and Allowances - Sales Discounts

Gross Profit = Net Sales Revenue - Cost of Goods Sold

Net Income = Gross Profit - Operating Expenses

Merchandise Inventory Systems

Perpetual vs. Periodic Inventory Systems

Businesses must track inventory to determine the value on hand and the value sold. There are two main inventory systems:

Perpetual Inventory System: Continuously updates inventory records for each purchase and sale.

Periodic Inventory System: Updates inventory records at the end of the period based on a physical count.

Purchasing Merchandise Inventory (Perpetual System)

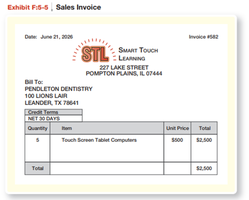

Recording Purchases

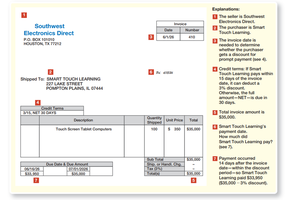

Purchases of merchandise inventory are recorded in the Merchandise Inventory account. Invoices (bills) are used to document purchases, and payment terms may include discounts for early payment.

Purchase Returns and Allowances

Purchase returns occur when defective or unsuitable goods are returned to the seller. Purchase allowances are reductions in the invoice price for goods kept by the purchaser despite being unsatisfactory.

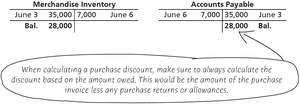

Purchase Discounts

Purchase discounts are incentives for early payment. Credit terms such as "3/15, net 30" mean a 3% discount is available if paid within 15 days; otherwise, the full amount is due in 30 days.

Transportation Costs

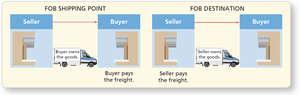

Shipping terms determine when ownership transfers and who pays freight:

FOB Shipping Point: Buyer owns goods in transit and pays freight (Freight In).

FOB Destination: Seller owns goods in transit and pays freight (Freight Out).

Net Cost of Inventory Purchased

The net cost of inventory is calculated as:

Net Cost = Purchases - Purchase Returns and Allowances - Purchase Discounts + Freight In

Sales of Merchandise Inventory (Perpetual System)

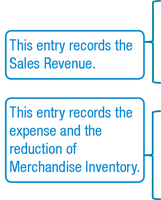

Recording Sales

Sales transactions require two entries: one to record the revenue and one to record the cost of goods sold and reduction in inventory.

Sales on Account

Sales may be made on account (credit sales), with or without discounts for early payment. Sales discounts reduce the amount of revenue recognized if payment is made within the discount period.

Sales Returns and Allowances

Sales returns occur when customers return goods. Sales allowances are reductions in the amount owed by the customer without returning goods. Both are contra-revenue accounts that reduce total sales revenue.

Transportation Costs—Freight Out

Freight Out is a delivery expense to the seller when goods are shipped to customers under FOB Destination terms.

Adjusting and Closing Entries for Merchandisers

Inventory Shrinkage

Inventory shrinkage is the loss of inventory due to theft, damage, or errors. Businesses adjust the Merchandise Inventory account to reflect the actual physical count at period end.

Closing Entries

The four-step closing process for a merchandising company includes closing revenue, expense, and dividend accounts to Retained Earnings, and adjusting for inventory shrinkage and estimated sales returns.

Financial Statements for Merchandisers

Income Statement Formats

Merchandisers may use a single-step or multi-step income statement:

Single-Step Income Statement: Groups all revenues together and all expenses together.

Multi-Step Income Statement: Reports subtotals such as gross profit and operating income, highlighting key relationships.

Gross Profit Percentage

Evaluating Business Performance

The gross profit percentage measures the profitability of each sales dollar above the cost of goods sold. It is calculated as:

Gross Profit Percentage = (Gross Profit / Net Sales Revenue) × 100%

Periodic Inventory System (Appendix)

Recording Purchases and Sales

Under the periodic system, inventory records are updated at the end of the period. Purchases, purchase returns and allowances, purchase discounts, and freight in are recorded in separate accounts. Cost of goods sold is calculated at period end.

Closing Entries (Periodic System)

Temporary accounts such as Purchases, Purchase Returns and Allowances, Purchase Discounts, and Freight In are closed to Income Summary at period end.

Net Method for Sales Discounts (Appendix)

Recording Sales at Net Amount

Under the net method, sales are recorded at the net amount (after deducting sales discounts). If the customer does not pay within the discount period, the discount lost is recorded as additional revenue.

Additional info: These notes are based on Chapter 5 of Horngren’s Financial & Managerial Accounting, focusing on merchandising operations, inventory systems, and related financial reporting.