Back

BackPlant Assets, Natural Resources, and Intangibles: Comprehensive Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Plant Assets, Natural Resources, and Intangibles

Introduction

This chapter covers the accounting for plant assets, natural resources, and intangible assets. It explains how to measure, depreciate, and report these long-lived assets, as well as how to handle their disposal, impairment, and the impact on financial statements and cash flows. The chapter also discusses differences between U.S. GAAP and IFRS, and the influence of ESG factors.

Accounting for the Cost of Plant Assets

Definition and Measurement

Plant assets are tangible long-lived assets used in operations, such as land, buildings, and equipment.

The cost of a plant asset is the sum of all expenditures necessary to acquire the asset and prepare it for its intended use.

Costs include purchase price, taxes, commissions, and costs to make the asset ready for use.

Land

Costs included: purchase price, brokerage commission, survey fees, legal fees, back property taxes, grading, clearing, and removal of unwanted buildings.

Costs not included: fencing, paving, security systems, lighting (these are land improvements and are depreciated separately).

Buildings, Machinery, and Equipment

Building construction costs: architectural fees, permits, contractor charges, materials, labor, overhead, and interest during construction.

Building purchase costs: purchase price, commissions, taxes, repairs, and renovations.

Equipment costs: purchase price (less discounts), transportation, insurance in transit, taxes, commissions, installation, testing, and special platforms.

Land Improvements and Leasehold Improvements

Land improvements: driveways, signs, fences, sprinkler systems, etc. (depreciated over useful life).

Leasehold improvements: improvements to leased property, amortized over the lease term.

Lump-Sum (Basket) Purchases

When multiple assets are purchased together, the total cost is allocated based on relative market values (relative-sales-value method).

Capital Expenditures vs. Immediate Expenses

Definitions

Capital expenditures: Costs that increase an asset’s capacity or extend its useful life; added to the asset account.

Immediate expenses: Costs that are expensed as incurred, typically for routine maintenance or immaterial amounts.

Leased Assets

Leasing allows use of assets without large upfront payments.

Most leases result in both a right-of-use asset and a lease liability on the balance sheet.

Depreciation of Plant Assets

Concept and Purpose

Depreciation allocates the cost of a plant asset over its useful life.

Reported as depreciation expense on the income statement; land is not depreciated.

Key Terms in Depreciation

Cost: All expenditures to acquire and prepare the asset.

Estimated useful life: Expected period of use.

Estimated residual value: Expected value at end of useful life.

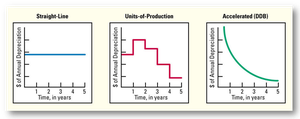

Depreciation Methods

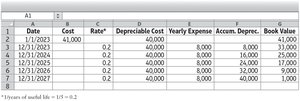

Straight-line method: Allocates equal depreciation each period.

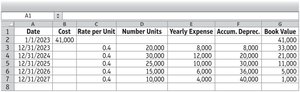

Units-of-production method: Depreciation based on usage or output.

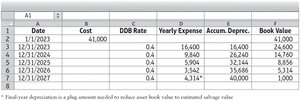

Double-declining-balance (DDB) method: Accelerated method, higher depreciation in early years.

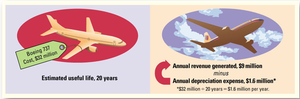

Straight-Line Method Example

Annual Depreciation Expense = (Cost - Residual Value) / Useful Life

Units-of-Production Method Example

Depreciation per Unit = (Cost - Residual Value) / Total Estimated Units

Double-Declining-Balance Method Example

Annual Depreciation Expense = Book Value at Beginning of Year × (2 / Useful Life)

Comparing Depreciation Methods

Straight-line: Even expense, best for assets generating revenue evenly.

Units-of-production: Best for assets that wear out with use.

DDB: Best for assets generating more revenue early in life.

Depreciation Methods in Practice

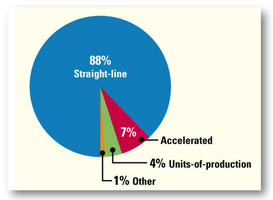

Most companies use straight-line depreciation for financial reporting.

Other Issues in Accounting for Plant Assets

Tax Depreciation

Accelerated methods (e.g., DDB, MACRS) are often used for tax purposes to maximize deductions and conserve cash.

Partial-Year Depreciation

Depreciation is prorated for assets acquired or disposed of during the year.

Changes in Useful Life

Changes are treated as changes in accounting estimates and applied prospectively.

Fully Depreciated Assets

Assets can continue to be used, but no further depreciation is recorded.

Remove asset and accumulated depreciation from the books upon disposal.

Disposal of Plant Assets

Accounting for Disposal

Update depreciation to date of disposal.

Remove asset and accumulated depreciation from the books.

Record any gain or loss on disposal.

GAAP vs. IFRS: Depreciation and Asset Reporting

GAAP: Uses historical cost and depreciates composite assets.

IFRS: Uses component approach, depreciating each significant part separately; allows reversal of impairment losses in some cases.

Natural Resources and Intangible Assets

Natural Resources

Examples: oil, minerals, timber.

Depletion allocates cost as resources are extracted and sold.

Intangible Assets

No physical substance; carry special rights (e.g., patents, copyrights, trademarks, franchises, goodwill).

Finite life intangibles are amortized; indefinite life intangibles are tested for impairment.

Goodwill

Excess of purchase price over fair value of net assets acquired; only recorded when purchased.

Tested for impairment, not amortized.

Research and Development (R&D) Costs

Expensed as incurred under U.S. GAAP; some development costs may be capitalized under IFRS if criteria are met.

Asset Impairment

Definition and Process

Occurs when expected future cash flows are less than the asset’s book value.

Impairment loss is recognized to reduce carrying value to fair value.

Rate of Return on Assets (ROA)

Definition and Calculation

Measures how efficiently assets generate net income.

Formula:

DuPont Analysis:

ESG Factors and Long-Lived Assets

Environmental, Social, and Governance (ESG) factors can affect asset values, useful lives, and impairment assessments.

Examples: regulatory changes, reputational risks, and shifts in societal values.

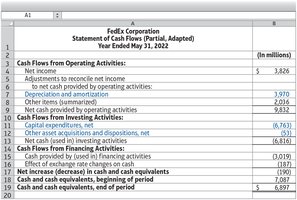

Cash Flow Impact of Long-Lived Asset Transactions

Statement of Cash Flows

Acquisitions: Investing outflows.

Sales: Investing inflows.

Depreciation/amortization: Added back to net income in operating activities (non-cash expense).

Calculating Depreciation Using Excel Functions

SLN function: Calculates straight-line depreciation.

DDB function: Calculates double-declining-balance depreciation.

Summary Table: Depreciation Methods Comparison

Method | Best For | Expense Pattern |

|---|---|---|

Straight-Line | Assets generating revenue evenly | Equal each year |

Units-of-Production | Assets that wear out with use | Varies with usage |

Double-Declining-Balance | Assets generating more revenue early | Higher in early years |

Additional info: These notes expand on the provided slides and images with academic context, definitions, and formulas to ensure a comprehensive, self-contained study guide for financial accounting students.