Back

BackPlant Assets, Natural Resources, and Intangibles – Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Plant Assets, Natural Resources, and Intangibles

Introduction

This chapter covers the accounting for property, plant, and equipment (PP&E), natural resources, and intangible assets. It explains how to measure, depreciate, and report these assets, as well as how to account for their disposal and evaluate business performance using asset-related ratios.

Property, Plant, and Equipment (PP&E)

Definition and Characteristics

PP&E are long-lived, tangible assets used in business operations, such as land, buildings, equipment, furniture, fixtures, and vehicles.

They are recorded at historical cost, which includes the purchase price and all costs necessary to get the asset ready for use.

The cost of PP&E is allocated to expense over its useful life through depreciation, following the matching principle.

Measuring the Cost of PP&E

Historical cost includes purchase price, taxes, commissions, and other costs to prepare the asset for use.

The cost principle requires assets to be recorded at their actual cost.

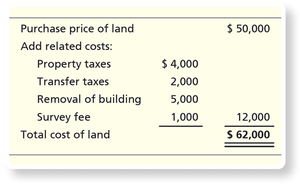

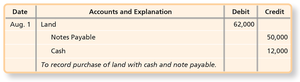

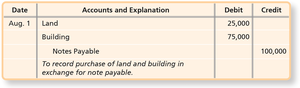

Land and Land Improvements

Cost of land includes purchase price, brokerage commission, survey/legal fees, delinquent property taxes, title transfer fees, and clearing costs.

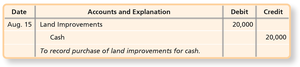

Land improvements (e.g., fencing, paving, lighting) are recorded separately and depreciated.

Buildings, Machinery, and Equipment

Building costs include construction or purchase price and renovation costs.

Machinery and equipment costs include purchase price (less discounts), transportation, insurance in transit, taxes, commissions, installation, and testing.

Furniture and Fixtures

Includes desks, chairs, cabinets, etc. Costs include purchase price and all costs to ready the asset for use.

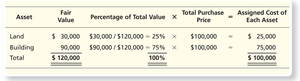

Lump-Sum (Basket) Purchases

When multiple assets are purchased together, the total cost is allocated based on each asset's relative fair market value (relative-market-value method).

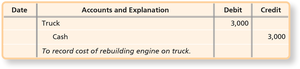

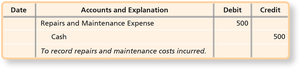

Capital and Revenue Expenditures

Capital expenditures increase asset capacity, efficiency, or useful life (e.g., extraordinary repairs).

Revenue expenditures maintain the asset in working order (e.g., routine repairs).

Data Analytics in Accounting

Data analytics help companies optimize property investments, monitor resource consumption, and plan maintenance.

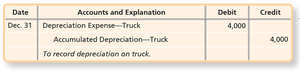

Depreciation of Plant Assets

What Is Depreciation?

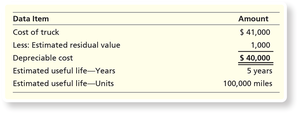

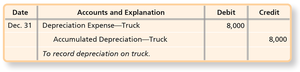

Depreciation allocates the cost of a plant asset (except land) over its useful life.

Depreciation is based on cost, estimated useful life, and estimated residual value.

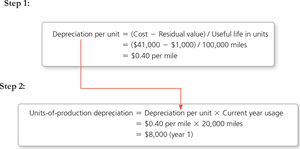

Depreciable cost = Cost – Estimated residual value.

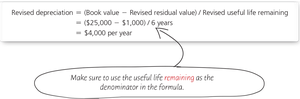

Depreciation Methods

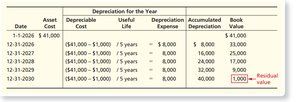

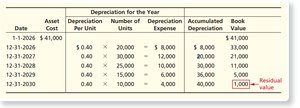

Straight-Line Method: Allocates equal depreciation each year.

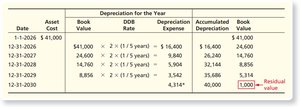

Units-of-Production Method: Depreciation varies with asset usage.

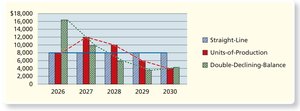

Double-Declining-Balance Method: Accelerated method, more expense early in asset's life.

Depreciation for Tax Purposes

The IRS requires the Modified Accelerated Cost Recovery System (MACRS) for tax reporting, which is not GAAP-compliant.

Partial-Year Depreciation

Depreciation is prorated for assets purchased during the year, often using the modified half-month convention.

Changing Estimates

If useful life or residual value estimates change, recalculate depreciation for current and future periods only.

Reporting PP&E

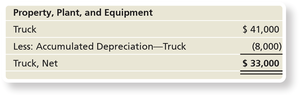

PP&E are reported at book value (cost minus accumulated depreciation) on the balance sheet.

Disposal of Plant Assets

Recording Disposals

Disposals may involve discarding, selling, or exchanging assets.

Steps: Update depreciation, remove asset and accumulated depreciation, record cash received/paid, recognize gain or loss.

Natural Resources

Accounting for Natural Resources

Natural resources are depleted using the units-of-production method.

Depletion expense is recorded as the resource is used.

Intangible Assets

Definition and Types

Intangible assets lack physical substance (e.g., patents, copyrights, trademarks, franchises, goodwill).

Purchased intangibles are recorded at cost.

Intangibles with definite lives are amortized; those with indefinite lives are tested for impairment.

Patents

Exclusive right to produce/sell an invention for 20 years.

Amortized over the shorter of useful or legal life.

Copyrights and Trademarks

Copyrights: Exclusive right to creative works, lasting life of creator plus 70 years.

Trademarks: Distinctive identifications of products/services, often renewable indefinitely.

Franchises and Licenses

Franchises: Rights to sell goods/services under specific conditions.

Licenses: Government-granted privileges to use public property.

Goodwill

Goodwill is the excess paid over the fair value of net assets in a business acquisition.

Not amortized; tested for impairment annually.

Asset Turnover Ratio

Evaluating Business Performance

The asset turnover ratio measures how efficiently a company uses its assets to generate sales.

Formula:

A higher ratio indicates more efficient use of assets.

Exchanges of Plant Assets

Accounting for Exchanges

Exchanges with commercial substance require recognition of gains or losses.

Journal entries reflect the removal of old asset, recognition of gain/loss, and recording of new asset and any cash paid/received.

Additional info: This summary covers all major aspects of accounting for plant assets, natural resources, and intangibles, including measurement, depreciation, disposal, and performance evaluation, as outlined in a typical financial accounting curriculum.