Back

BackReceivables and Revenue: Recognition, Management, and Reporting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Receivables and Revenue

Revenue Recognition (GAAP)

Revenue recognition is a fundamental principle in financial accounting, governed by Generally Accepted Accounting Principles (GAAP). Proper recognition ensures that revenues are recorded when earned, and expenses are matched to the revenues they generate.

Revenue is recognized when: Goods are delivered or services are performed.

Expense recognition: Expenses are recognized when incurred, matching them to the related revenues.

Example: Apple Inc. delivers 1,000 iPhones to AT&T, recognizes revenue when delivered, and matches the cost of goods sold to the sale.

Shortening the Credit Cycle

Businesses aim to accelerate cash flow from sales by shortening the credit cycle. This is achieved through sales discounts, charging interest, and emphasizing credit card sales.

Sales Discounts: Incentives for early payment, recorded as a contra revenue account.

Credit Card Sales: Fees are deducted from sales revenue; e.g., Apple sells a MacBook Pro Max for $4,000, VISA charges a 2% fee.

Discount Format: 2/10, n/30 means 2% discount if paid within 10 days, otherwise full payment due in 30 days.

Sales Returns and Allowances

Sales returns and allowances account for merchandise returned by customers or price reductions. Estimations are made each period based on historical experience.

Sales Returns: Increase sales returns and accrue a liability (Sales Refunds Payable).

Inventory Returns: Adjust inventory and decrease cost of goods sold.

Net Sales: Net Sales = Sales revenue – Sales discounts – Sales returns & allowance

Example: Amazon estimates 1% returns on $50 billion sales; actual returns and cost adjustments are recorded.

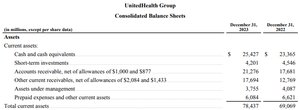

Accounts Receivable

Accounts receivable are amounts owed by customers for goods or services sold on credit. They are tracked using subsidiary ledgers and are reported net of allowances for uncollectible accounts.

Acquisition: Through sales of goods and services.

Control: By tracking subsidiary ledger accounts by customer.

Reporting: Net of allowance for uncollectible accounts.

Uncollectible Accounts (Allowance Method)

Losses from failure to collect accounts receivable are estimated and recorded using the allowance method, in accordance with GAAP.

Journal Entry: DR: Uncollectible account expense (Bad debt expense) CR: Allowance for Uncollectible Accounts

Estimation Methods:

Percent-of-Sales Method (Income Statement Approach): Uncollectible-account expense computed as a percent of revenue.

Aging-of-Receivables Method (Balance Sheet Approach): Specific accounts are analyzed based on how long they have been outstanding.

Example: Apple estimates 0.02% of $400,000 million revenues as uncollectible.

Writing Off Uncollectible Accounts

When a specific account is determined to be uncollectible, it is written off against the allowance for uncollectible accounts.

Example: Apple writes off $9 (RS) and $3 (TM) from accounts receivable.

Effect: Reduces both accounts receivable and allowance for uncollectible accounts; net receivables remain unchanged.

Direct Write-Off Method

This method records expense when a specific customer’s account proves to be uncollectible. It is less preferable and not GAAP-compliant.

No allowance for uncollectibles: May overstate assets.

Fails to match expenses: Does not recognize uncollectible accounts in the same period as related revenue.

Computing Cash Collections from Customers

Cash collections from customers are computed by analyzing changes in accounts receivable, sales, and write-offs.

Formula:

Example Table:

Beg. Bal. | Sales | Write-offs | Collections | End. Bal. |

|---|---|---|---|---|

200 | 1,500 | 100 | X = 1,600 | 400 |

Notes Receivable and Interest Revenue

Notes receivable are formal written promises to pay a specified amount plus interest. Interest revenue is recognized over time.

Interest Formula: Where P = principal, I/R = interest rate, T = time (fraction of year).

Issuance Example: Whitman Inc. signs a 6-month, 9% promissory note with BOA for $1 million.

Adjusting for Accrued Interest: Interest revenue is accrued at period end.

Reporting: Notes receivable and accrued interest are reported in financial statements.

Liquidity and Ratios

Liquidity measures a company’s ability to meet short-term obligations. Ratios such as the current ratio and accounts receivable turnover are used to assess liquidity.

Current Ratio:

Accounts Receivable Turnover:

Summary Table: Allowance for Uncollectible Accounts

Accounts Receivable—RS | Accounts Receivable—TM | Allowance for Uncollectible Accounts |

|---|---|---|

9 | 3 | 100 |

9 (written off) | 3 (written off) | 88 |

Summary Table: Accounts Receivable Cash Collections

Beg. Bal. | Sales | Write-offs | Collections | End. Bal. |

|---|---|---|---|---|

200 | 1,500 | 100 | X = 1,600 | 400 |

Financial Statement Examples

Financial statements disclose receivables, allowances, and net sales. These are critical for understanding a company’s financial health.

Key Terms

Accounts Receivable: Amounts owed by customers.

Allowance for Uncollectible Accounts: Estimated amount of receivables not expected to be collected.

Sales Discounts: Incentives for early payment.

Sales Returns and Allowances: Reductions in sales for returned goods or allowances.

Notes Receivable: Formal written promises to pay.

Interest Revenue: Income earned from lending money.

Additional info: Academic context and examples were expanded for clarity and completeness. Tables were recreated and formulas provided in LaTeX format for exam preparation.