Back

BackReceivables, Inventory, and Plant Assets: Principles of Accounting Chapters 5–7 Study Guide

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Chapter 5: Receivables and Revenue

Trade Accounts Receivable

Trade accounts receivable are amounts owed to a company by its customers resulting from the sale of goods or services. These are typically classified as current assets on the balance sheet.

Definition: Receivables arising from sales of products or services.

Classification: Reported as current assets, not noncurrent assets.

Example: A company sells merchandise to a customer on credit; the amount owed is a trade receivable.

Net Realizable Value of Accounts Receivable

The net realizable value (NRV) of accounts receivable is the amount a company expects to collect, after accounting for estimated uncollectible accounts.

Formula:

Example: If Accounts Receivable is $140,000 and Allowance is $12,000, NRV is $128,000.

Allowance Method for Uncollectible Accounts

The allowance method estimates bad debts and records them as an expense, creating a contra-asset account (Allowance for Uncollectible Accounts).

Percentage of Sales Method: Bad debt expense is calculated as a percentage of credit sales.

Journal Entry:

Example: expense.

Aging Method for Allowance

The aging method estimates uncollectible accounts based on the outstanding receivables and adjusts the allowance account accordingly.

Calculation:

Adjustment: Increase allowance to required balance.

Example: ; if current allowance is expense.

Write-Offs of Uncollectible Accounts

When a specific account is determined to be uncollectible, it is written off against the allowance account.

Journal Entry:

Effect: No change in net realizable value.

Interest Calculation on Loans

Interest on loans is calculated based on principal, rate, and time.

Formula:

Example: for 6 months.

Chapter 6: Inventory and Cost of Goods Sold

Periodic Inventory Formula

The periodic inventory formula is used to calculate cost of goods sold (COGS) and beginning inventory.

Formula:

Example: If purchases are $50,000, ending inventory is $25,000, sales are $100,000, and gross profit is $32,000, COGS is $68,000 and beginning inventory is $43,000.

Perpetual Inventory System

In the perpetual system, inventory and cost of goods sold are updated continuously.

Sales Entry: Debit Accounts Receivable/Cash, Credit Sales; Debit Cost of Goods Sold, Credit Inventory.

Inventory Classification

Inventory is classified as a current asset on the balance sheet.

Current Asset: Inventory is expected to be sold or used within one year.

FOB Destination and Inventory Ownership

FOB destination means ownership transfers when goods are received by the buyer.

Implication: Goods in transit are not included in buyer's inventory until received.

Inventory Costing Methods

Different methods affect COGS and ending inventory values.

FIFO (First-In, First-Out): Oldest costs assigned to COGS; newest costs to ending inventory.

LIFO (Last-In, First-Out): Newest costs assigned to COGS; oldest costs to ending inventory.

Weighted-Average: Average cost per unit applied to both COGS and ending inventory.

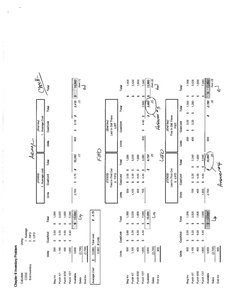

Worked Example: Hefty Company Inventory Methods

Hefty Company inventory and sales:

Beginning Inventory: 500 units @ $3.00

Purchases: 1,100 units @ $3.20; 400 units @ $4.00; 1,600 units @ $4.40

Total units: 3,600; Sales: 2,700 units

Weighted-Average Calculation:

Total cost: $13,660; Average cost per unit: $13,660 / 3,600 = $3.7944

COGS: 2,700 x $3.7944 = $10,245

FIFO and LIFO: Refer to worked solutions for specific COGS and ending inventory values.

Additional info: The included image provides a comparative table of inventory costing methods (FIFO, LIFO, Weighted-Average), showing calculations for ending inventory and cost of goods sold based on the Hefty Company example. This visual aids in understanding how each method allocates costs.

Chapter 7: Plant Assets, Natural Resources, and Intangibles

Capitalization vs. Expense

Costs to acquire and prepare assets for use are capitalized; costs with no future benefit are expensed.

Capitalized: Broker's fees, freight, installation fees.

Expensed: Repairs during installation.

Asset Acquisition and Allocation

Costs related to acquiring land and constructing buildings are allocated to the respective assets.

Land: Purchase price plus legal fees.

Building: Architect's fees plus construction costs.

Example: Land: $152,000; Building: $275,000.

Subsequent Expenditures on Plant Assets

Routine maintenance is expensed; improvements that extend life or increase capacity are capitalized.

Example: Replacing tires is a maintenance expense; replacing an engine may be capitalized.

Depreciation Methods and Book Value

Depreciation allocates the cost of a tangible asset over its useful life.

Straight-Line Method:

Book Value:

Example: Truck cost $20,000, residual $4,000, 4-year life; after 3 years, book value is $8,000.

Depreciation Journal Entry

Entry: Debit Depreciation Expense, Credit Accumulated Depreciation.

Disposal of Plant Assets

When an asset is sold, remove its cost and accumulated depreciation, and record any gain or loss.

Loss: Sale proceeds less than book value.

Journal Entry: Debit Accumulated Depreciation, Credit Machinery, record Cash and Loss.

Intangible Assets and Amortization

Intangible assets are non-physical assets, amortized over their useful life.

Amortization: Systematic allocation of cost of intangible assets.

Examples: Patents, copyrights, goodwill.

Goodwill

Goodwill is the excess of purchase price over the fair value of net identifiable assets acquired in a business combination.

Recorded only when purchased: Internally generated goodwill is not recognized.

Impairment: Goodwill is not amortized, but tested for impairment.

Return on Assets (ROA)

ROA measures profitability relative to average total assets.

Formula:

Example: Net income $720,000, ROA 12%, average assets $6,000,000.