Back

BackStatement of Cash Flows: Structure, Analysis, and Application

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Statement of Cash Flows

Introduction to the Statement of Cash Flows

The Statement of Cash Flows is a core financial statement that provides information about a company's cash inflows and outflows during an accounting period. It is essential for understanding a company's liquidity, solvency, and overall financial health. The statement is developed using data from the balance sheet and income statement, typically requiring two years of balance sheets and one year of income statement data.

Importance of Cash Flow

Cash flow is critical because it determines a company's ability to pay employees, suppliers, and creditors.

It is possible for a company to report positive net income but still face liquidity problems if it cannot convert earnings into cash.

Cash flow analysis helps identify whether a company is generating sufficient cash from its operations or relying on external financing.

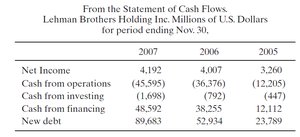

Example: The collapse of Lehman Brothers illustrates the importance of cash flow. Despite reporting rising net income, the company failed to generate cash from operations and relied on borrowings, ultimately leading to bankruptcy.

Sections of the Statement of Cash Flows

The statement is divided into three main sections, each reflecting different types of cash activities:

Operating Activities: Cash flows related to the core business operations, such as cash received from customers and cash paid to suppliers and employees.

Investing Activities: Cash flows from the acquisition and disposal of long-term assets and investments, such as purchasing equipment or selling securities.

Financing Activities: Cash flows related to borrowing, repaying debt, issuing shares, and paying dividends.

Cash and Cash Equivalents

Cash includes currency, bank deposits, and highly liquid investments (cash equivalents) such as T-bills, notes, commercial paper, and certificates of deposit (CDs).

The statement measures cash at the beginning and end of the year, both found on the balance sheet.

Details of Cash Flow Activities

Operating Activities

Inflows: Revenues from sales of goods and services, returns from suppliers, and interest received.

Outflows: Payments for inventory, taxes, operating expenses (SG&A), and interest on debt.

Investing Activities

Inflows: Proceeds from the sale of assets and securities.

Outflows: Capital expenditures, acquisitions, and purchases of securities.

Financing Activities

Inflows: Proceeds from borrowing and issuing shares.

Outflows: Repayment of debt, purchase of own shares, and payment of dividends.

Methods for Preparing the Statement of Cash Flows

Direct Method: Lists major classes of gross cash receipts and payments.

Indirect Method: Starts with net income and adjusts for non-cash items and changes in working capital.

Formula (Indirect Method):

Classifying Cash Flow Activities: Case Study Example

In practice, companies must classify each cash flow as operating, investing, or financing. For example, in the Nike Inc. case study, students are asked to assign each financial activity to the correct section of the cash flow statement and determine its effect on cash balance.

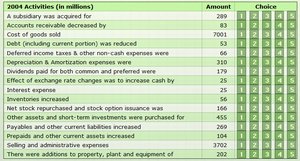

Activity | Amount (in millions) | Classification |

|---|---|---|

A subsidiary was acquired for | 289 | Investing |

Accounts receivable decreased by | 701 | Operating |

Cost of goods sold | 3603 | Operating |

Debt (including current portion) was reduced | 56 | Financing |

Depreciation & Amortization expenses were | 229 | Operating |

Dividends paid for both common and preferred were | 219 | Financing |

Effect of exchange rate changes was to increase cash by | 25 | Separate line item |

Interest expense | 85 | Operating |

Inventories increased | 56 | Operating |

Net stock repurchased and stock option issuance was | 415 | Financing |

Other assets and short-term investments were purchased for | 455 | Investing |

Payables and other current liabilities increased | 140 | Operating |

Prepaid and other current assets increased | 102 | Operating |

Selling and administrative expenses | 1044 | Operating |

There were additions to property, plant and equipment of | 702 | Investing |

Additional info: This table helps students practice the classification of cash flows, a key skill in financial accounting.

Summary Table of Cash Flow

The Summary Table is a tool for analyzing the statement of cash flows by common-sizing the data. It shows cash inflows and outflows as percentages of total inflows and outflows, respectively. The table typically aggregates cash from operations and provides details for investing and financing activities.

Highlights the importance of internal cash generation from operations.

Shows the implications for investing and financing when operational cash generation is insufficient.

Analysis of the Statement of Cash Flows

Cash Flow from Operating Activities

Ongoing business success depends on generating cash from operations.

Early-stage companies may use more cash than they generate, while mature companies should generate significant cash from operations.

Analysis of Cash Inflows and Outflows

Excess cash from operations is preferred for financing capital expenditures, debt repayment, and dividends.

When analyzing outflows, consider their necessity and how they are financed (short-term assets with short-term debt, long-term assets with long-term debt or equity).

Practice and Application

Students are encouraged to practice with real company data and summary tables to reinforce their understanding of cash flow analysis.

Excel activities and interactive simulations can help develop practical skills in preparing and analyzing statements of cash flows.