Back

BackStep-by-Step Guidance for Adjusting Entries and Trial Balance Corrections in Financial Accounting

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

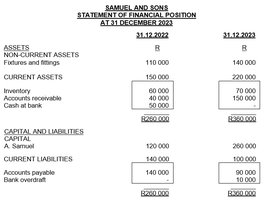

Q1. From the above information, calculate the firm's profit or loss for the year ended 31 December 2023.

Background

Topic: Financial Statements – Profit Calculation

This question tests your ability to derive profit or loss from the Statement of Financial Position, considering the effects of adjusting entries and omitted transactions.

Key Terms and Formulas:

Profit: The increase in equity during the period, excluding owner contributions and withdrawals.

Statement of Financial Position: Shows assets, liabilities, and equity at year-end.

Drawings: Withdrawals by the owner, which reduce equity.

Formula for profit:

Step-by-Step Guidance

Identify the opening and closing capital balances from the Statement of Financial Position for 2022 and 2023.

Determine the amount of drawings for the year (given in the question or notes).

Apply the profit formula to set up your calculation, substituting the values for closing capital, opening capital, and drawings.

Check if all values are correctly sourced from the financial statements and notes.

Try solving on your own before revealing the answer!

Final Answer: Profit for 2023 is R200,000

This calculation uses the closing capital, opening capital, and drawings as per the Statement of Financial Position.

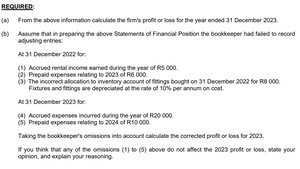

Q2. Assume that in preparing the above Statements of Financial Position, the bookkeeper has failed to record adjusting entries. Calculate the corrected profit or loss for 2023, taking the omissions into account.

Background

Topic: Adjusting Entries and Their Impact on Profit

This question tests your understanding of how omitted adjusting entries (such as accrued income, prepaid expenses, depreciation, and accrued expenses payable) affect the calculation of profit.

Key Terms and Formulas:

Accrued Income: Income earned but not yet received.

Prepaid Expenses: Expenses paid in advance, not yet incurred.

Depreciation: Allocation of the cost of an asset over its useful life.

Accrued Expenses Payable: Expenses incurred but not yet paid.

Corrected Profit: Adjusted for omitted entries.

Step-by-Step Guidance

List each omitted adjusting entry and determine its effect on profit (overstated or understated).

Calculate the adjustment for each entry (e.g., accrued rent income, prepaid expenses, depreciation, accrued expenses payable, prepaid expenses for 2024).

Set up the corrected profit calculation by starting with the previously calculated profit and adjusting for each omission.

Sum the adjustments to determine the net effect on profit, but stop before the final calculation.

Try solving on your own before revealing the answer!

Final Answer: Corrected Profit for 2023 is R178,200

Each adjustment reflects the impact of omitted entries on profit, ensuring the profit figure is accurate for the period.

Q3. If you think that any of the omissions (1) to (5) above do not affect the 2023 profit or loss, state your opinion and explain your reasoning.

Background

Topic: Effects of Adjusting Entries on Financial Statements

This question tests your ability to critically evaluate the impact of omitted adjusting entries on profit or loss, using accounting principles.

Key Terms:

Matching Principle: Expenses and incomes should be matched to the period in which they are incurred or earned.

Accrual Basis: Recognizes income and expenses when they are earned/incurred, not when cash is received/paid.

Step-by-Step Guidance

Review each omitted entry and consider whether it relates to the current financial period.

Apply the matching principle to determine if the omission would cause profit to be overstated or understated.

Formulate your opinion based on whether the omission violates accrual accounting principles.

Prepare a brief explanation for your reasoning, but stop before stating your final opinion.

Try solving on your own before revealing the answer!

Final Answer: All omissions affect profit due to the matching principle.

Omitting adjusting entries causes profit to be misstated, as expenses and incomes are not matched to the correct period.

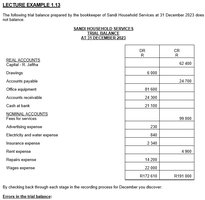

Q4. Explain how you would correct errors 1 to 12 in the trial balance.

Background

Topic: Correction of Errors in Trial Balance

This question tests your understanding of how to identify and correct errors in the trial balance using appropriate accounting procedures.

Key Terms:

Trial Balance: A list of all ledger accounts and their balances at a point in time.

Correcting Journal Entry: An entry made to fix errors in the ledger or trial balance.

Step-by-Step Guidance

Identify the nature of each error (e.g., omission, incorrect posting, wrong account, wrong amount).

Determine the correct entry for each error, specifying which accounts and amounts are affected.

Prepare the correcting journal entry for each error, but stop before posting the final entries.

Check that the corrections will restore the trial balance to equality between debits and credits.

Try solving on your own before revealing the answer!

Final Answer: Correcting entries are made for each error to restore the trial balance.

Each error is corrected by a journal entry that adjusts the affected accounts, ensuring the trial balance is accurate.