Back

BackStep-by-Step Guidance for Journalising March Transactions (Seasonal Cards)

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

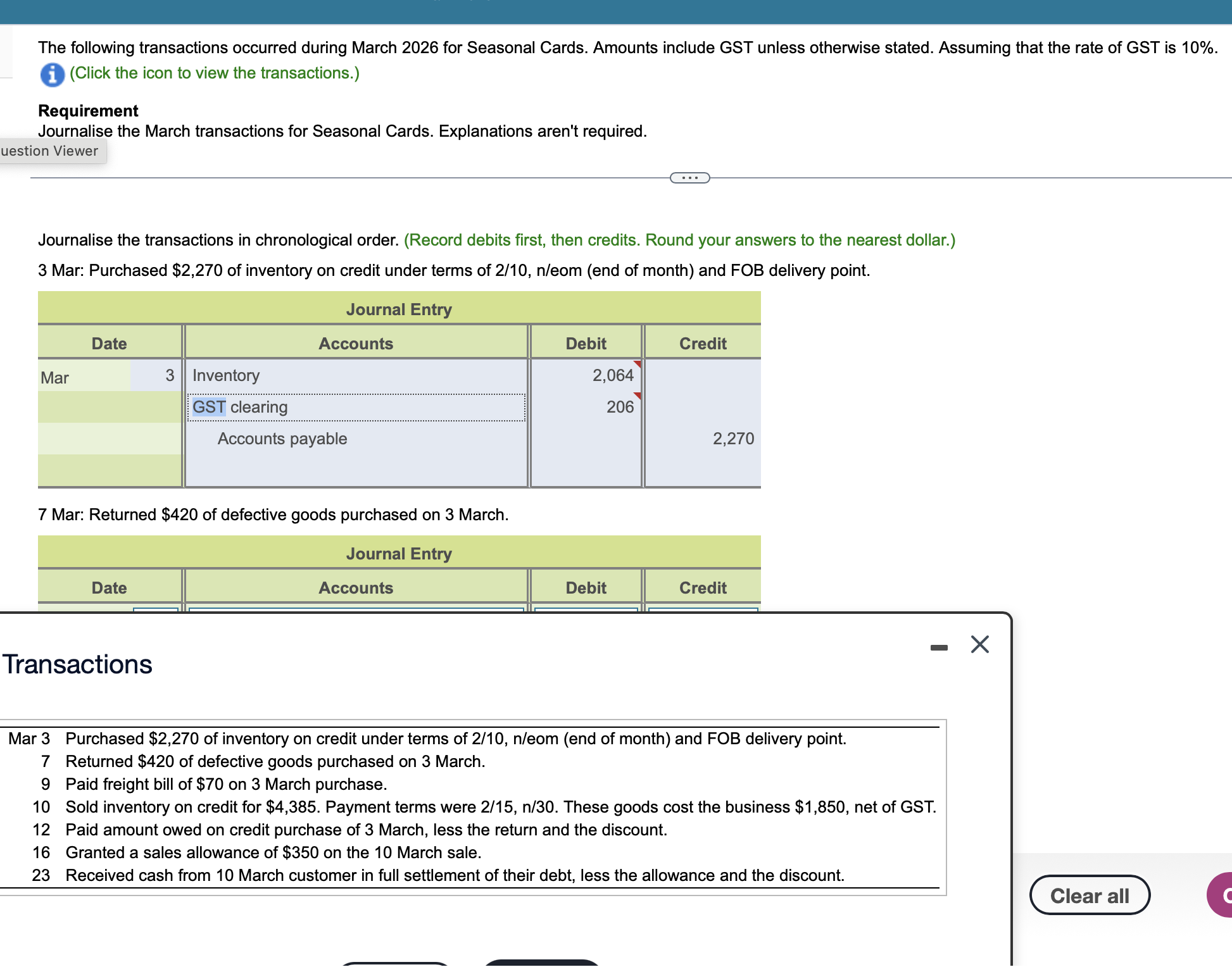

Q1. Journalise the March transactions for Seasonal Cards in chronological order. (Record debits first, then credits. Round your answers to the nearest dollar.)

Background

Topic: Financial Accounting – Journal Entries for Merchandising Transactions

This question tests your understanding of how to record business transactions in the general journal, including purchases, sales, returns, allowances, discounts, and GST (Goods and Services Tax) implications.

Key Terms and Formulas

Inventory: Goods purchased for resale.

Accounts Payable: Amount owed to suppliers.

GST Clearing: Account used to record GST paid or collected.

Sales Allowance: Reduction in the selling price due to issues with goods.

Sales Discount: Reduction in amount owed by customer for early payment.

Journal Entry Format: Date, Account Titles, Debit Amounts, Credit Amounts.

GST Calculation: GST is 10% of the net amount (unless otherwise stated).

Step-by-Step Guidance

Start by identifying each transaction and the accounts affected. For purchases, consider Inventory, GST Clearing, and Accounts Payable. For sales, consider Accounts Receivable, Sales Revenue, GST Clearing, and Cost of Goods Sold.

For the 3 March purchase: Calculate the GST portion ($2,270 × 10/11 for net inventory, $2,270 × 1/11 for GST). Record Inventory and GST Clearing as debits, Accounts Payable as credit.

For the 7 March return: Calculate the GST portion of the returned goods ($420 × 10/11 for net inventory, $420 × 1/11 for GST). Record Accounts Payable as debit, Inventory and GST Clearing as credits.

For the 9 March freight bill: Since it's FOB delivery point, the buyer pays freight. Record Freight-In (or Inventory) as debit, Accounts Payable or Cash as credit. GST may apply if not included.

For the 10 March sale: Record Accounts Receivable (including GST), Sales Revenue (net of GST), GST Clearing (credit), and Cost of Goods Sold (debit), Inventory (credit).

Try solving on your own before revealing the answer!