Back

BackStockholders’ Equity: Structure, Transactions, and Analysis

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Stockholders’ Equity

Definition and Overview

Stockholders’ equity represents the residual interest in the assets of a corporation after deducting liabilities. It is also known as shareholders’ equity and is a fundamental component of the balance sheet.

Equity Formula:

Residual Interest: Equity holders have claims on assets after creditors’ claims are satisfied.

Balance Sheet Equation:

Additional info: The image above visually represents the balance sheet equation, showing assets balanced against liabilities and equity.

Components of Stockholders’ Equity

Stockholders’ equity is composed of several key sections, each reflecting different sources and uses of capital:

Contributed Capital: Capital received from shareholders in exchange for stock.

Retained Earnings: Cumulative net income retained in the company, not distributed as dividends.

Treasury Stock: Shares repurchased by the company, recorded as a contra-equity account.

Accumulated Other Comprehensive Income (AOCI): Cumulative net gains/losses from specific items not included in net income.

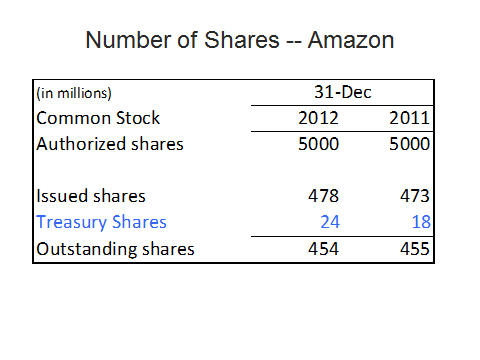

Capital Stock: Authorized, Issued, and Outstanding Shares

Definitions

Corporations issue shares of stock to raise capital. The terminology surrounding shares is important for understanding equity structure:

Authorized Shares: Maximum number of shares a corporation can legally issue.

Issued Shares: Shares that have been sold to investors.

Outstanding Shares: Issued shares currently held by shareholders (not including treasury shares).

Treasury Shares: Issued shares reacquired by the corporation.

Type | Description |

|---|---|

Authorized Shares | Maximum allowed by corporate charter |

Issued Shares | Sold to investors |

Outstanding Shares | Held by shareholders |

Treasury Shares | Reacquired by company |

Additional info: The table above illustrates the relationship between authorized, issued, treasury, and outstanding shares for Amazon.

Common Stock

Characteristics

Common stock represents basic ownership in a corporation and confers several rights and responsibilities:

Voting Rights: Common shareholders typically vote on major corporate matters.

Residual Value: Entitled to residual assets after obligations are met.

Limited Liability: Shareholders are not personally liable for corporate debts.

Par Value: Nominal value assigned to shares; often set very low.

Issuing Common Stock

Common stock can be issued with or without par value. The accounting treatment differs accordingly:

Without Par Value: Entire proceeds credited to common stock.

With Par Value: Par value credited to common stock; excess credited to Additional Paid-In Capital (APIC).

Example (With Par Value):

Issue 5,000 shares at $10 each, $1 par value:

Journal Entry: Dr. Cash $50,000 Cr. Common Stock $5,000 Cr. APIC $45,000

Preferred Stock

Characteristics and Preferences

Preferred stock is a class of stock with specific rights and preferences, often including:

Dividend Preference: Paid before common dividends.

Cumulative Dividends: Unpaid dividends accumulate and must be paid before common dividends.

Bankruptcy Preference: Paid before common shareholders in liquidation.

Limited Voting Rights: Usually none unless specified.

Example (Cumulative Preferred Dividend):

Preferred dividend per year:

Year 11: Pay 3 years’ dividends (9), common receives remainder.

Treasury Stock

Definition and Purpose

Treasury stock consists of shares reacquired by the corporation. It is a contra-equity account and reduces total equity.

No Voting or Dividend Rights: Treasury shares do not participate in voting or dividends.

Recorded at Cost: When reacquired, recorded at purchase price.

Reasons for Buyback: Alternative to dividends, increase EPS, meet option requirements, perceived undervaluation.

Additional info: The chart above shows the impact of share buybacks on Berkshire Hathaway’s share price, reflecting management’s belief in undervaluation.

Retained Earnings

Definition and Link to Financial Statements

Retained earnings represent the cumulative net income retained by the company, not distributed as dividends. It links the income statement to the balance sheet.

Formula:

Dividends: Subtracted directly from retained earnings, not treated as an expense.

Dividends

Types and Key Dates

Dividends are distributions of earnings to shareholders. They become legal obligations only after declaration by the board.

Cash Dividends: Most common; paid in cash.

Stock Dividends: Paid in additional shares; discussed in advanced courses.

Key Dates: Declaration Date (liability recorded), Date of Record (no entry), Payment Date (cash paid).

Other Comprehensive Income (OCI) and Accumulated OCI (AOCI)

Definition

OCI includes gains and losses from specific sources not included in net income, such as unrealized gains/losses on certain securities, foreign currency translation, derivative hedges, and pension adjustments. AOCI is the cumulative net OCI reported on the balance sheet.

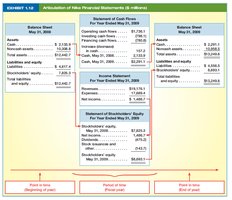

Statement of Stockholders’ Equity

Format and Purpose

The statement of stockholders’ equity summarizes changes in equity accounts over a period. It reconciles beginning and ending balances and links to the balance sheet.

Format: Beginning balances, changes during period, ending balances.

Purpose: Provides transparency regarding equity transactions.

Additional info: The image above illustrates the articulation between the balance sheet, income statement, and statement of stockholders’ equity.

Book Value vs. Market Value

Comparison

Book value is the value of equity as reported under GAAP or IFRS, while market value is determined by the market price of shares.

Book Value:

Market Value:

Differences: Market value reflects future expectations, risk, and other qualitative factors.

Equity Exercises: Questrom Inc.

Calculation Examples

Given equity account balances, students can calculate shares issued, issue price, treasury shares, and total equity:

Number of Common Shares Issued:

Number of Preferred Shares Issued:

Issue Price per Common Share:

Issue Price per Preferred Share:

Number of Shares in Treasury:

Total Stockholders’ Equity:

Common Shares Outstanding:

Summary Table: Equity Components

Component | Description |

|---|---|

Contributed Capital | Capital received for stock issued |

Retained Earnings | Net income retained, not distributed |

Treasury Stock | Shares repurchased by company |

AOCI | Cumulative other comprehensive income |