Back

BackStockholders’ Equity: Structure, Transactions, and Financial Statement Presentation

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Stockholders’ Equity

Features of a Corporation

A corporation is a distinct legal entity, separate from its owners, with unique characteristics that influence its financial accounting and reporting.

Separate Legal Entity: The corporation exists independently of its owners (stockholders).

Ownership: Stockholders (or shareholders) are the owners of the corporation.

Continuous Life and Transferability: Ownership can be transferred through the buying and selling of stock, and the corporation continues regardless of changes in ownership.

Limited Liability: Stockholders are only liable for the amount they invested in the corporation.

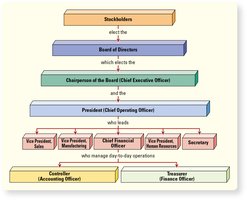

Separation of Ownership and Management: The board of directors, elected by stockholders, oversees management.

Corporate Taxation: Corporations face double taxation—corporate income is taxed, and dividends paid to stockholders are also taxed.

Government Regulation: Corporations are subject to various state and federal regulations.

Advantages and Disadvantages of a Corporation

Advantages: Limited liability, ease of raising capital, continuous existence, and transferability of ownership.

Disadvantages: Double taxation, government regulation, and separation of ownership and management.

Organizing a Corporation

Incorporators obtain a charter from the state, pay fees, sign the charter, file documents, and agree to bylaws. The charter authorizes the corporation to issue a certain number of shares.

Stockholders’ Rights

Vote: Right to vote on corporate matters.

Dividends: Right to receive a proportionate share of dividends.

Liquidation: Right to receive a share of assets upon liquidation.

Preemption: Right to maintain proportionate ownership by purchasing new shares.

Components of Stockholders’ Equity

Paid-in Capital (Contributed Capital): Amounts invested by stockholders, including stock accounts and additional paid-in capital.

Retained Earnings: Cumulative net income less dividends paid.

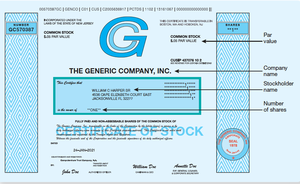

Stock Certificate Example

A stock certificate documents ownership, par value, company name, stockholder name, and number of shares.

Common Stock vs. Preferred Stock

Common Stock: Basic ownership, voting rights, residual claim on assets, and highest risk/reward.

Preferred Stock: Priority for dividends and assets in liquidation, but usually no voting rights. May have conversion features.

Par-Value and No-Par-Value Stock

Par-Value Stock: Assigned value per share; sets minimum legal capital.

No-Par-Value Stock: No assigned value; may have a stated value.

Issuance of Stock

Issuing Common Stock at Par

When stock is issued at par value, the proceeds are credited to the Common Stock account.

Journal Entry Example: Issue 10 million shares at $10 par value:

Debit: Cash $100,000,000

Credit: Common Stock $100,000,000

Issuing Common Stock Above Par

If stock is issued above par, the excess is credited to Additional Paid-in Capital.

Journal Entry Example: Issue 10 million shares at $10 per share, $1 par:

Debit: Cash $100,000,000

Credit: Common Stock $10,000,000

Credit: Additional Paid-in Capital $90,000,000

Note: No gain or loss is recognized on stock transactions with owners.

No-Par Common Stock

All proceeds are credited to Common Stock or, if a stated value exists, to Common Stock and Additional Paid-in Capital.

Example: Issue 63,069,000 shares for $266,724,000; all credited to Common Stock.

Issuing Stock for Noncash Assets or Services

Record the asset or service received and the stock issued at fair market value.

Example: Issue 15,000 shares for equipment ($4,000) and building ($120,000):

Debit: Equipment $4,000

Debit: Building $120,000

Credit: Common Stock $15,000

Credit: Additional Paid-in Capital $109,000

Ethical Note: Fair value must be objectively determined to avoid manipulation.

Preferred Stock Transactions

Similar accounting as common stock; may have separate paid-in capital accounts.

Convertible preferred stock can be exchanged for common stock at a set rate.

Authorized, Issued, and Outstanding Stock

Authorized: Maximum shares allowed by charter.

Issued: Shares distributed to stockholders.

Outstanding: Shares currently held by stockholders (issued minus treasury stock).

Treasury Stock

Nature and Purpose

Treasury stock is a corporation’s own stock that has been reacquired. It is held for various purposes, such as employee compensation, resale, or to prevent takeovers.

Recorded at cost, not par value.

Contra equity account with a debit balance.

Reported below retained earnings on the balance sheet.

Retirement and Resale of Treasury Stock

Retirement: Stock is canceled and cannot be reissued; reduces issued shares.

Resale: Increases assets and equity by cash received; no gain or loss is recognized. Excess over cost is credited to Paid-in Capital from Treasury Stock Transactions.

Summary of Treasury Stock Transactions

Purchase: Decreases assets and equity.

Resale: Increases assets and equity.

Retirement: Removes shares from equity accounts.

Employee compensation: Increases expenses and equity accounts.

Retained Earnings, Dividends, and Stock Splits

Retained Earnings

Retained earnings represent cumulative net income less net losses and dividends declared. A credit balance indicates accumulated profits; a debit balance indicates a deficit.

Dividends

Cash Dividends: Most common; requires sufficient retained earnings and cash. Declared by the board of directors.

Key Dates:

Declaration Date: Liability is recorded.

Date of Record: Determines eligible stockholders (no entry).

Payment Date: Dividend is paid and liability removed.

Preferred Dividends: Paid before common dividends; may be cumulative (dividends in arrears must be paid first) or noncumulative.

Stock Dividends

Proportional distribution of additional shares to stockholders.

Increases Common Stock and Additional Paid-in Capital; decreases Retained Earnings; total equity unchanged.

Small Stock Dividend: ≤ 25%, recorded at market value.

Large Stock Dividend: > 25%, recorded at par value.

Stock Splits

Increase number of shares and reduce par value proportionally.

Market price per share decreases; no effect on total equity or accounts.

Evaluating Company Performance

Return on Equity (ROE) and DuPont Analysis

ROE measures profitability relative to stockholders’ equity. DuPont Analysis breaks ROE into components to analyze profitability drivers.

Formula:

Earnings Per Share (EPS)

EPS indicates the net income attributable to each share of common stock.

Formula:

Example: Net income EPS = \frac{2,300}{538} = 4.28 $

Effect of Equity Financing on EPS

Issuing stock dilutes EPS and ownership; issuing debt increases risk but may increase EPS if returns exceed interest cost.

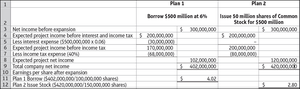

Plan 1: Borrow $500 million at 6% | Plan 2: Issue 50 million shares for $500 million | |

|---|---|---|

Net income before expansion | $300,000,000 | $300,000,000 |

Expected project income before interest and income tax | $200,000,000 | $200,000,000 |

Less: Interest expense | ($30,000,000) | - |

Expected project income before income tax | $170,000,000 | $200,000,000 |

Less: Income tax (30%) | ($51,000,000) | ($60,000,000) |

Expected project net income | $119,000,000 | $140,000,000 |

Total company net income | $419,000,000 | $440,000,000 |

Earnings per share after expansion | $4.19 | $2.93 |

Market Capitalization and Price-Earnings Ratio

Market Capitalization: Market price per share × shares outstanding.

Price-Earnings Ratio: Market price per share ÷ EPS; reflects market expectations.

Dividend Yield

Formula:

Measures the percentage return to stockholders from dividends.

Reporting Stockholders’ Equity Transactions

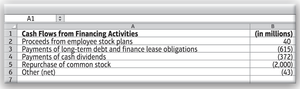

Statement of Cash Flows

Equity transactions are classified as financing activities, including issuance of stock, treasury stock transactions, and dividend payments.

Cash Flows from Financing Activities | (in millions) |

|---|---|

Proceeds from employee stock plans | 40 |

Payments of long-term debt and finance lease obligations | (615) |

Payments of cash dividends | (372) |

Repurchase of common stock | (2,000) |

Other (net) | (43) |

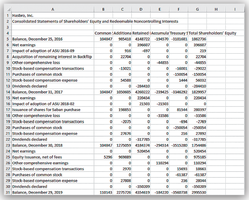

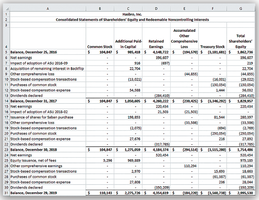

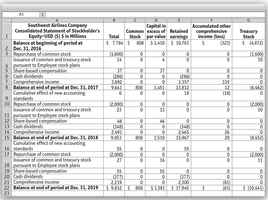

Consolidated Statements of Stockholders’ Equity

These statements summarize changes in equity accounts over a period, including common and preferred stock, additional paid-in capital, retained earnings, other comprehensive income, and treasury stock.

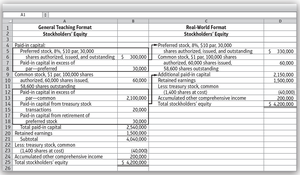

Formats for Reporting Stockholders’ Equity

Stockholders’ equity can be presented in various formats, but generally includes preferred stock, common stock, additional paid-in capital, retained earnings, accumulated other comprehensive income, and treasury stock.

General Teaching Format | Real-World Format |

|---|---|

Preferred stock, $1 par, 20,000 shares authorized, issued, and outstanding | Preferred stock, $1 par, 750,000 shares authorized, issued, and outstanding |

Paid-in capital in excess of par | Paid-in capital in excess of par |

Common stock, $1 par, 100,000 shares authorized, 60,000 shares issued and outstanding | Common stock, $1 par, 2,150,000 shares authorized, issued, and outstanding |

Paid-in capital in excess of par | Paid-in capital in excess of par |

Retained earnings | Retained earnings |

Less: Treasury stock, common | Less: Treasury stock, common |

Accumulated other comprehensive income | Accumulated other comprehensive income |

Total stockholders’ equity | Total stockholders’ equity |

Formatting Financial Statements

General Guidelines

Center and bold statement and column headings.

Wrap column headings to fit column width.

Use thousand separators and right-justify numbers.

Use a consistent number of decimal places.

Place dollar signs at the start of columns, subtotals, and totals.

Use dashes for zeros.

Single line above subtotals; single above and double below totals.

Use 11-point Calibri font and spell-check statements.