Back

BackTransaction Analysis and the Accounting Cycle: Debits, Credits, and Financial Statements

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Ch. 2 Transaction Analysis

Concept: Debits and Credits

In financial accounting, every business transaction affects at least two accounts and is recorded using a system of debits and credits. This ensures that the accounting equation remains balanced after each transaction.

Transaction: An exchange where you receive something and give something in return.

Double-entry system: Every transaction impacts at least two accounts, with equal debit and credit amounts.

Debits: Increase Asset and Expense accounts.

Credits: Increase Liability, Equity, and Revenue accounts.

Account Type | Increased by |

|---|---|

Assets | Debits |

Expenses | Debits |

Liabilities | Credits |

Equity | Credits |

Revenues | Credits |

Example: If Fun Times Happy Company purchases a machine for $50,000, the journal entry would debit Equipment (an asset) and credit Cash (an asset), reflecting the exchange.

Concept: The General Flow of Accounts

Accounts follow a general flow formula to determine their ending balances:

Accounts Receivable: Represents amounts owed by customers. Increased by credit sales, decreased by cash collections.

Retained Earnings: Accumulates net income not paid as dividends. Increased by net income, decreased by dividends.

Example (Accounts Receivable): If the beginning balance is $1,200, credit sales are $2,000, and the ending balance is $1,800, cash collected can be calculated using the flow formula.

Example (Retained Earnings): Beginning balance $55,000, revenues $40,000, expenses $32,000, dividends $6,000. The ending balance is calculated as $55,000 + ($40,000 - $32,000) - $6,000 = $57,000.

Concept: Transaction Analysis – Business Formation Example

Transaction analysis involves recording the effects of business activities on the accounting equation and preparing journal entries. Each transaction must keep the equation balanced:

Example Transactions:

(a) Owner invests cash for common stock: Increase assets (cash) and equity (common stock).

(b) Purchase of land with cash: Increase land, decrease cash (both assets).

(c) Purchase of supplies on account: Increase supplies (asset), increase accounts payable (liability).

(d) Revenue earned on account: Increase accounts receivable (asset), increase revenue (equity).

(e) Payment of wages: Decrease cash (asset), increase wage expense (equity reduction).

(f) Collection from customers: Increase cash, decrease accounts receivable (both assets).

(g) Payment of dividends: Decrease cash, increase dividends (equity reduction).

(h) Personal purchase by owner: Not a business transaction; not recorded in company books.

Concept: Trial Balance

A trial balance is a list of all accounts and their balances at a specific point in time. It is used to verify that total debits equal total credits before preparing financial statements.

T-account: A visual tool to track increases and decreases in an account.

Trial Balance Order: Accounts are typically listed in the following order: Assets, Liabilities, Equity, Revenues, Expenses.

Account | Debit | Credit |

|---|---|---|

Cash | ||

Accounts Receivable | ||

Supplies | ||

Land | ||

Accounts Payable | ||

Common Stock | ||

Dividends | ||

Revenues | ||

Wage Expense | ||

Total |

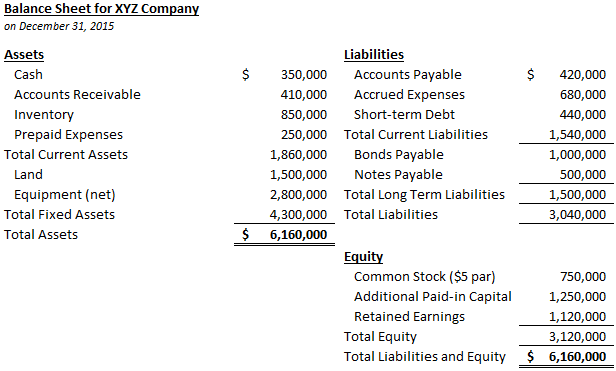

Concept: Classified Balance Sheet Components

The classified balance sheet presents a company's assets, liabilities, and equity at a specific point in time, grouping assets and liabilities into current and long-term categories for clarity.

Current Assets: Assets expected to be converted to cash or used within one year (e.g., cash, accounts receivable, inventory).

Long-Term Assets: Assets held for more than one year (e.g., land, equipment).

Current Liabilities: Obligations due within one year (e.g., accounts payable, short-term debt).

Long-Term Liabilities: Obligations due after one year (e.g., bonds payable, notes payable).

Order of Liquidity: Current assets are listed in order of liquidity, typically: Cash, Accounts Receivable, Inventory, Prepaid Expenses, Other Current Assets.

Example: Classified Balance Sheet

The following is an example of a classified balance sheet for XYZ Company as of December 31, 2015:

Total Assets: $6,160,000

Total Liabilities: $3,040,000

Total Equity: $3,120,000

Total Liabilities and Equity: $6,160,000 (balances with total assets)

Additional info: The classified balance sheet format helps users assess the company's liquidity, solvency, and financial flexibility by clearly distinguishing between short-term and long-term resources and obligations.