Back

BackTransaction Analysis in Financial Accounting: Chapter 2 Study Notes

Study Guide - Smart Notes

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Tailored notes based on your materials, expanded with key definitions, examples, and context.

Transaction Analysis in Financial Accounting

Introduction

Transaction analysis is a foundational concept in financial accounting, focusing on how business events impact the accounting equation and individual accounts. This study guide covers the identification and classification of transactions, the rules of debit and credit, journalizing and posting, constructing a trial balance, and introduces machine learning applications in accounting.

Recognizing Business Transactions and Types of Accounts

Definition and Nature of Transactions

Transaction: Any event with a financial impact on the business that can be measured reliably.

Transactions involve an exchange: something is given and something is received.

Accounting records both sides of every transaction to ensure objectivity and completeness.

Examples: Selling goods, purchasing supplies, paying salaries.

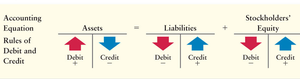

The Accounting Equation

The basic relationship in accounting is expressed as:

Assets: Resources owned by the business.

Liabilities: External claims on assets (debts).

Stockholders' Equity: Internal claims (owners' interest).

Types of Accounts

Assets: Cash, Accounts Receivable, Notes Receivable, Inventory, Prepaid Expenses, Investments, Property Plant & Equipment.

Liabilities: Accounts Payable, Notes Payable, Accrued Liabilities.

Stockholders' Equity: Common Stock, Retained Earnings, Dividends, Revenues, Expenses.

Example Table: Classification of Accounts

Account | Type |

|---|---|

Cash | Asset |

Accounts Payable | Liability |

Common Stock | Stockholders' Equity |

Service Revenue | Revenue (SE) |

Rent Expense | Expense (SE) |

Analyzing the Impact of Transactions on the Accounting Equation

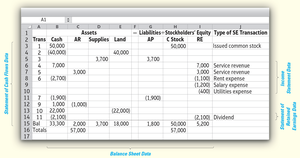

Transaction Analysis Example: Alladin Travel, Inc.

Each transaction affects at least two accounts and must be analyzed for its impact on assets, liabilities, and equity.

Transaction 1: Owners invest $50,000 cash, business issues common stock.

Transaction 2: Purchase of land for $40,000 cash.

Transaction 3: Supplies purchased on account ($3,700).

Transaction 4: Service revenue earned ($7,000).

Transaction 5: Services performed on account (Accounts Receivable).

Transaction 6: Payment of expenses (rent, salaries, utilities).

Transaction 7: Payment on account payable.

Transaction 8: Personal transaction by stockholder (no entry).

Transaction 9: Collection from customer on account.

Transaction 10: Sale of land for cash at cost.

Transaction 11: Declaration and payment of dividend.

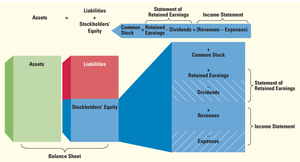

Financial Statements Flow

Information from transactions flows into financial statements: Income Statement, Statement of Retained Earnings, and Balance Sheet.

Analyzing the Impact of Transactions on Accounts

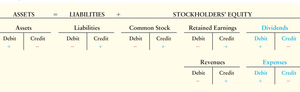

Double-Entry System and T-Accounts

Every transaction affects at least two accounts.

Debits and credits are used to indicate increases or decreases in accounts.

T-Account: Visual tool to track debits (left) and credits (right).

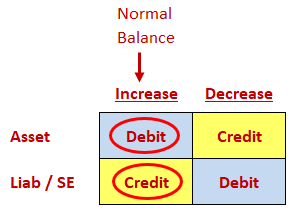

Normal Balances

Assets: Increased by debits, decreased by credits.

Liabilities and Stockholders' Equity: Increased by credits, decreased by debits.

Expanded Accounting Equation

The expanded equation includes revenues, expenses, and dividends:

Journalizing Transactions and Posting to the Ledger

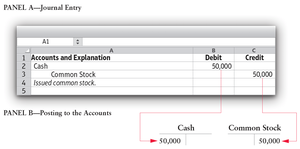

Journal Entries

Transactions are first recorded in the journal as journal entries.

Each entry specifies accounts affected, amounts, and whether each is a debit or credit.

Example: Issuing common stock for cash

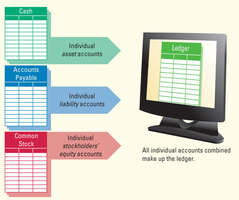

Posting to the Ledger

Posting transfers journal entry amounts to individual ledger accounts.

The ledger is the collection of all accounts.

Flow of Accounting Data

Transaction occurs → Transaction analyzed → Journal entry made → Amounts posted to ledger accounts.

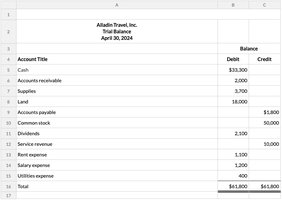

Constructing a Trial Balance

Purpose and Structure

A trial balance lists all accounts and their balances at a specific date.

Ensures that total debits equal total credits.

Facilitates preparation of financial statements.

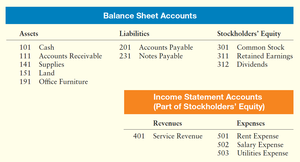

Chart of Accounts

Organization and Use

A chart of accounts lists all account titles and numbers used by a business.

Accounts are grouped by type: assets, liabilities, stockholders' equity, revenues, and expenses.

Machine Learning in Accounting and Business

Overview and Applications

Artificial Intelligence (AI): Machines that solve problems in a human-like manner.

Machine Learning: Machines learn from data without explicit programming.

Applications in accounting include automating transaction classification and fraud detection.

Programming languages: Python (most popular), R, Julia, Java.

Summary Table: Rules of Debit and Credit

Account Type | Increase | Decrease |

|---|---|---|

Asset | Debit | Credit |

Liability | Credit | Debit |

Stockholders' Equity | Credit | Debit |

Revenue | Credit | Debit |

Expense | Debit | Credit |

Dividend | Debit | Credit |

Key Formulas

Basic Accounting Equation:

Expanded Accounting Equation:

Conclusion

Transaction analysis is essential for understanding how business activities affect financial statements. Mastery of the accounting equation, types of accounts, rules of debit and credit, and the mechanics of journalizing and posting is foundational for all financial accounting students.