Back

BackMacroeconomics Key Concepts and Principles

06:23

06:23

Terms in this set (29)

A market system uses prices to signal resource allocation to individuals.

Choices are affected by incentives.

Because society has only a limited amount of productive resources.

Scarcity is always present due to limited resources; shortages are usually temporary.

Money is not an economic resource; it is a medium of exchange.

The accumulation of skills, training, and education of workers.

Physical capital.

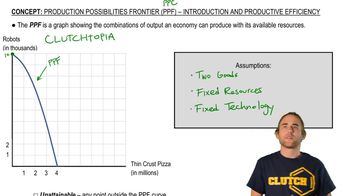

All possible combinations of two goods that can be efficiently produced with given resources.

The law of increasing opportunity cost.

When a person can produce a good at a lower opportunity cost than another.

Specialization usually increases productivity.

Resources are being inefficiently utilized.

As price decreases, quantity demanded increases, ceteris paribus.

The total quantities demanded by all consumers at given prices.

Fish is an inferior good and beef stew is a normal good for Sarah.

An increase in expected future price of the good, among other factors.

Demand for good A increases.

The sum of the employed and unemployed individuals.

Seasonal unemployment.

The unemployment level when normal frictional unemployment is accounted for.

A sustained decrease in the average price level of goods and services.

They are inversely related.

The total monetary value of all final goods and services produced.

By comparing the cost of a market basket of goods in the current year to the base year.

Real interest rate = nominal rate - inflation rate = \(7\% - 3\%\) = 4%.

Incomes fall and unemployment increases.

A period when overall business activity is rising.

The total market value of all final goods and services produced within a country in a year.

GDP = Consumption + Investment + Government Spending + Net Exports (Exports - Imports).