Skip to main content

Microeconomics

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

My Course

Learn

Exam Prep

AI Tutor

Study Guides

Flashcards

Explore

Try the app

Back

Perfect Competition and Efficiency definitions

You can tap to flip the card.

Perfect Competition

You can tap to flip the card.

👆

Perfect Competition

A market structure where many firms sell identical products, ensuring prices reflect both consumer and producer costs.

Track progress

Control buttons has been changed to "navigation" mode.

1/14

Related flashcards

Related practice

Recommended videos

Perfect Competition and Efficiency quiz #1

Perfect Competition and Efficiency

10 Terms

Perfect Competition and Efficiency

11. Perfect Competition

10 problems

Topic

Four Market Model Summary: Perfect Competition

11. Perfect Competition

10 problems

Topic

11. Perfect Competition

11 topics

15 problems

Chapter

Guided course

06:46

Efficiency in Perfect Competition

2284

views

19

rank

Terms in this set (14)

Hide definitions

Perfect Competition

A market structure where many firms sell identical products, ensuring prices reflect both consumer and producer costs.

Productive Efficiency

Occurs when production happens at the lowest possible cost, specifically at the minimum point of average total cost.

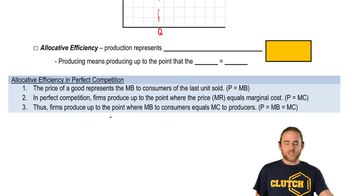

Allocative Efficiency

Achieved when the quantity produced matches consumer preferences, with marginal benefit equaling marginal cost.

Average Total Cost

Represents the per-unit cost of production, minimized when firms operate efficiently in perfect competition.

Marginal Benefit

The value consumers place on the last unit purchased, reflected by the market price at equilibrium.

Marginal Cost

The expense incurred by producers for making one additional unit, matched by price in efficient markets.

Equilibrium Price

The market price where supply meets demand, ensuring both productive and allocative efficiency.

Demand Curve

A graphical representation showing how consumer willingness to pay decreases as quantity increases.

Supply Curve

A graph illustrating how producers offer more goods as price rises, intersecting demand at equilibrium.

Marginal Revenue

The additional income a firm receives from selling one more unit, equal to price in perfect competition.

Consumer Preferences

The desires and priorities of buyers, guiding the allocation of resources in efficient markets.

Profit Maximizing Point

The output level where marginal revenue equals marginal cost, ensuring optimal firm performance.

Long Run

A period in which firms can adjust all inputs, leading to production at minimum average total cost.

Monopoly

A market structure with a single seller, typically failing to achieve both productive and allocative efficiency.

BackBack

BackBack

06:46

06:46