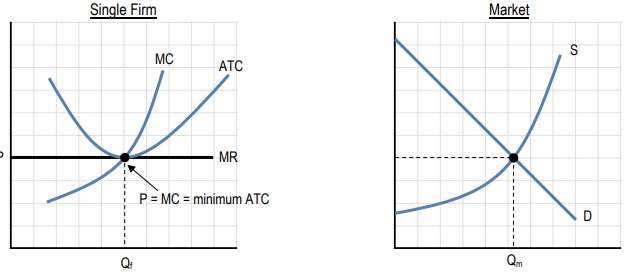

In perfectly competitive markets, both productive efficiency and allocative efficiency are achieved, leading to optimal resource allocation and cost management. Productive efficiency occurs when firms produce goods at the lowest possible cost, which is represented by the minimum point of the Average Total Cost (ATC) curve. In this scenario, the price of the good equals the minimum ATC, ensuring that firms operate efficiently and maximize profits by minimizing costs.

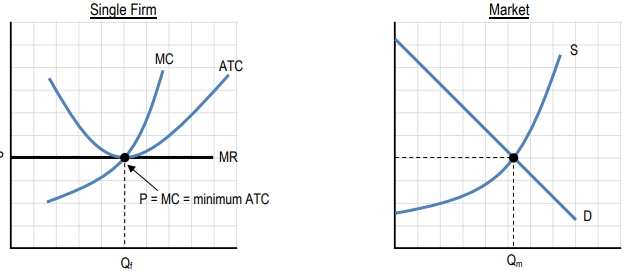

On the other hand, allocative efficiency is concerned with how resources are distributed according to consumer preferences. This efficiency is reached when the marginal benefit to consumers equals the marginal cost of production. In economic terms, the price of the good reflects the marginal benefit of the last unit sold, while firms produce where marginal revenue equals marginal cost. In a perfectly competitive market, the equilibrium price aligns with both the marginal benefit to consumers and the marginal cost to producers, confirming that resources are allocated efficiently.

To summarize, in perfect competition, the conditions for both productive efficiency (where price equals minimum ATC) and allocative efficiency (where marginal benefit equals marginal cost) are met. This unique characteristic of perfect competition contrasts with other market structures, such as monopolies, which typically do not achieve these efficiencies. Thus, perfect competition stands out as a model for optimal economic efficiency.