Risk is the uncertainty about future financial gains or losses due to unpredictable events.

Why are most people considered risk averse?

Most people are risk averse because they dislike losses more than they enjoy equivalent gains.

How do economists quantify satisfaction or happiness?

Economists use the concept of utility to quantify satisfaction or happiness.

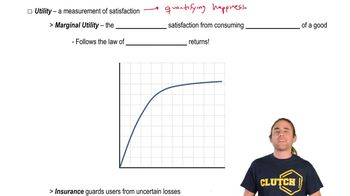

What does marginal utility refer to?

Marginal utility is the additional satisfaction gained from consuming one more unit of a good.

What is the law of diminishing marginal utility?

The law of diminishing marginal utility states that each additional unit consumed provides less additional satisfaction than the previous one.

How does the utility of money change as you acquire more of it?

The utility of money increases at a decreasing rate, meaning each extra dollar brings less satisfaction than the previous one.

Why does losing money hurt more than gaining the same amount helps?

Losing money causes a larger drop in utility than the increase in utility from gaining the same amount, due to diminishing marginal utility.

What type of losses do people typically insure against?

People typically insure against unlikely but catastrophic losses, such as those from a fire.

How does insurance help manage risk?

Insurance allows individuals to pay a small, certain cost to avoid the risk of a large, uncertain loss.

What is the main reason the insurance market exists?

The insurance market exists to help people manage and reduce the impact of financial risk.

How does insurance relate to utility and risk aversion?

Insurance helps risk-averse individuals maintain higher utility by protecting them from large losses that would significantly decrease their satisfaction.

What is meant by 'internalizing external costs' in insurance markets?

Internalizing external costs means that insurance markets help individuals bear the costs of unpredictable events, reducing the negative impact on society.

How does insurance reduce deadweight loss from financial shocks?

Insurance reduces deadweight loss by spreading risk and preventing large, unpredictable losses from causing significant economic inefficiency.

Why might someone be willing to pay for insurance even if the event is unlikely?

Someone may pay for insurance to avoid the large loss in utility that would result from a rare but catastrophic event.

What is the relationship between risk, utility, and insurance?

Risk creates uncertainty in utility, and insurance allows individuals to trade a small certain loss for protection against a large uncertain loss, aligning with risk aversion and diminishing marginal utility.

Back

Back

07:25

07:25